Contractor Workers Compensation Insurance: Keeping Your Crew Protected

One injury on a job site can derail your entire operation. Medical bills pile up, work stops, and your crew loses income-fast.

That’s why contractor workers compensation insurance isn’t optional. At Saberlines Insurance Services, we’ve seen firsthand how the right coverage protects both your team and your bottom line when accidents happen.

What Workers Compensation Actually Pays For

Workers compensation covers three distinct areas that matter when your crew gets hurt on the job. In 2022, covered workers received 29.0 billion dollars in medical benefits and 32.7 billion dollars in cash benefits according to the National Academy of Social Insurance, showing just how substantial this protection is.

Medical care gets priority treatment

The medical side pays for immediate treatment-emergency room visits, surgeries, medications, ongoing therapy-everything your health insurance won’t touch because it’s work-related. Your health plan actively excludes injuries that happen on job sites, which is why workers compensation fills that gap. When someone gets injured, workers compensation prioritizes access to the right medical provider fast. This isn’t theoretical-the system pays for initial treatment, specialist referrals, imaging, prescriptions, and ongoing rehabilitation without requiring your worker to fight with insurance companies or worry about deductibles.

Many plans include occupational medicine networks that understand work-related injuries better than general practitioners, meaning faster diagnosis and more appropriate treatment paths. The coverage extends to prosthetics, mobility aids, and adaptive equipment if the injury requires it. This speed matters because delayed treatment costs more and keeps your worker sidelined longer.

Disability benefits replace lost income

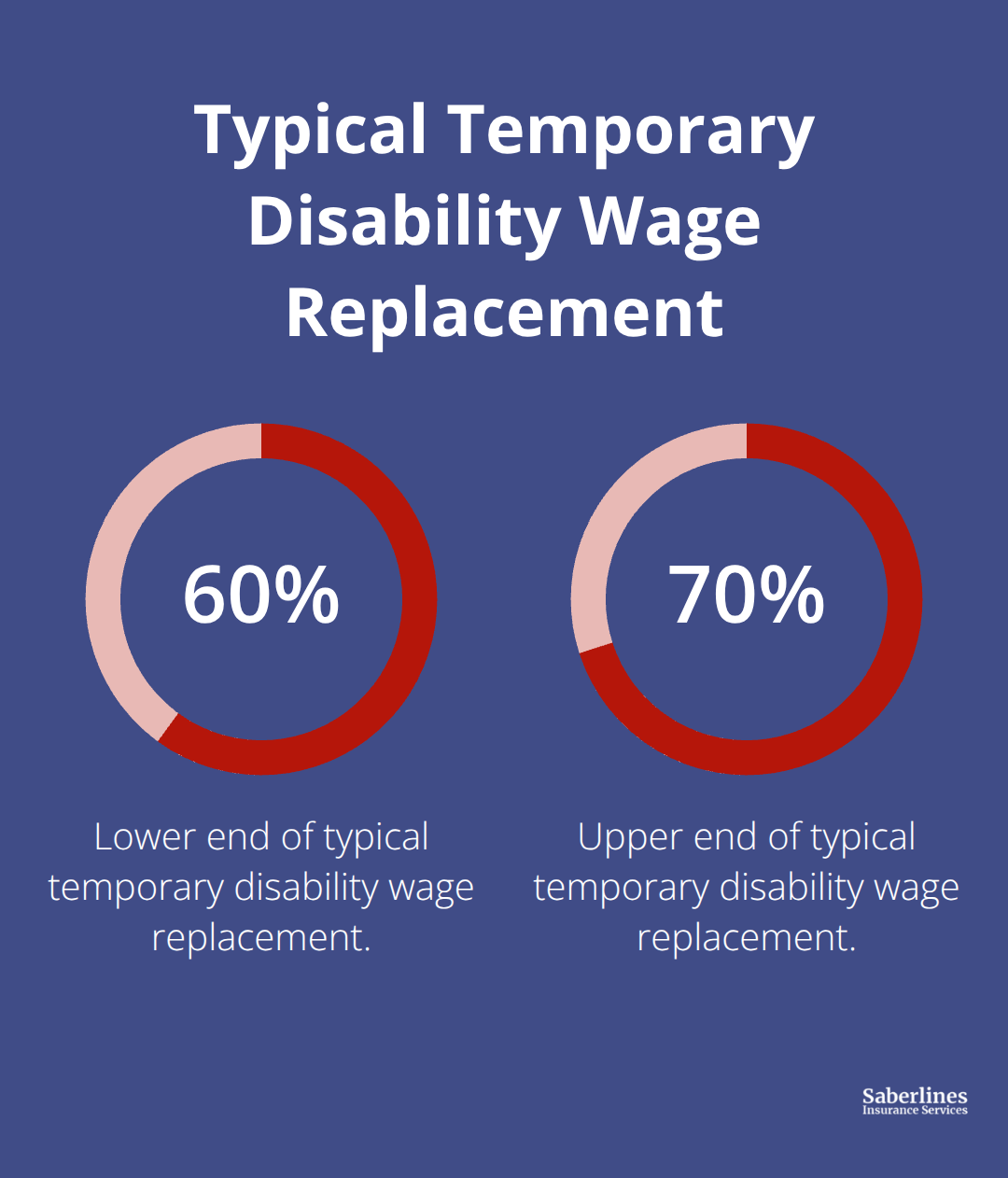

The cash side replaces lost wages while your worker recovers, typically covering a percentage of their regular earnings during temporary disability. Temporary disability benefits typically replace between 60 and 70 percent of the worker’s average weekly wage while they’re unable to work, providing income stability during recovery.

If the injury causes permanent damage, permanent disability benefits continue indefinitely, protecting your crew member from financial ruin.

Return-to-work programs reduce downtime and costs

If your worker can return to lighter duty work before full recovery, many plans support modified work arrangements that keep them earning something while healing. Return-to-work programs actively reduce the number of lost workdays, which directly lowers your overall workers compensation costs over time. A robust claims management process with timely reporting and thorough investigation mitigates costs significantly. The longer someone stays out of work, the more expensive the claim becomes, so getting injured workers back productively is built into how modern workers compensation systems function.

Understanding what your policy covers sets the foundation for protecting your crew. The next step is recognizing why contractors specifically need this coverage-and what happens when you don’t have it in place.

Why Your Crew Needs This Coverage

Contractors operate in one of the highest-risk environments in the workforce. The U.S. Bureau of Labor Statistics reported that service workers and transportation/materials moving occupations accounted for 46.4 percent of all workplace injuries in 2021-2022, and construction extraction roles added another 6.1 percent to that total.

These aren’t abstract statistics-they represent real crew members who face falls, equipment contact, vehicle accidents, and exposure to hazards every single day. Without workers compensation coverage, a single serious injury can bankrupt your business while leaving your worker financially devastated.

State requirements vary significantly

Each state sets its own workers compensation rules, and violations cost money fast. California requires licensed contractors to carry coverage in addition to general liability and surety bonds, while other states have different thresholds based on employee count or industry classification. Most states legally require you to carry this insurance if you have employees, with penalties ranging from $1,000 in Arizona to up to $10,000 in fines or 18 months imprisonment in New Jersey.

If you operate across multiple states, you need coverage aligned to each jurisdiction’s specific requirements-not a one-size-fits-all approach. Many contractors misclassify workers as independent contractors to avoid premiums, but this strategy backfires when audits reveal the misclassification and you face back premiums plus penalties. The safest approach involves consulting a business attorney about your specific workforce structure, then securing coverage that matches your actual classification decisions.

Liability protection keeps your business intact

When an injured worker files a claim, workers compensation acts as a shield that prevents them from suing you directly for negligence. This no-fault system means your worker receives benefits regardless of who caused the accident, and in exchange, they cannot pursue a personal injury lawsuit against you. Without this protection, a catastrophic injury claim could exceed your business assets.

A certificate of insurance proves to clients that you maintain coverage, which many contracts now require before work begins. Clients increasingly demand proof of coverage, making this documentation essential for securing jobs and protecting your reputation. Even in states where coverage isn’t mandated for certain contractor types, skipping it exposes you to direct liability claims that can exceed your annual revenue in minutes.

Your bottom line depends on controlled costs

Workers compensation premiums average around $54 per month, but actual costs depend on payroll, location, employee count, industry risk level, and your claims history. The 2025 workers compensation market shows rising premiums driven by wage growth and medical inflation, meaning costs will likely increase year-over-year. Your crew members know whether you have their backs when something goes wrong, and that knowledge directly impacts job satisfaction, productivity, and your ability to attract skilled workers.

Implement a strong safety program with regular training and hazard reporting to reduce your premium costs directly-fewer claims mean lower loss costs. Accurate payroll data and regular audits prevent mispricing and premium surprises at renewal time. A robust return-to-work program that moves injured workers back to productive activity reduces lost workdays and associated claim expenses significantly. These cost-control measures transform workers compensation from a fixed expense into a manageable investment that protects both your crew and your financial stability.

Understanding what your policy covers and why you need it sets the foundation for protecting your crew. The next step involves selecting the right policy that matches your specific operation and risk profile.

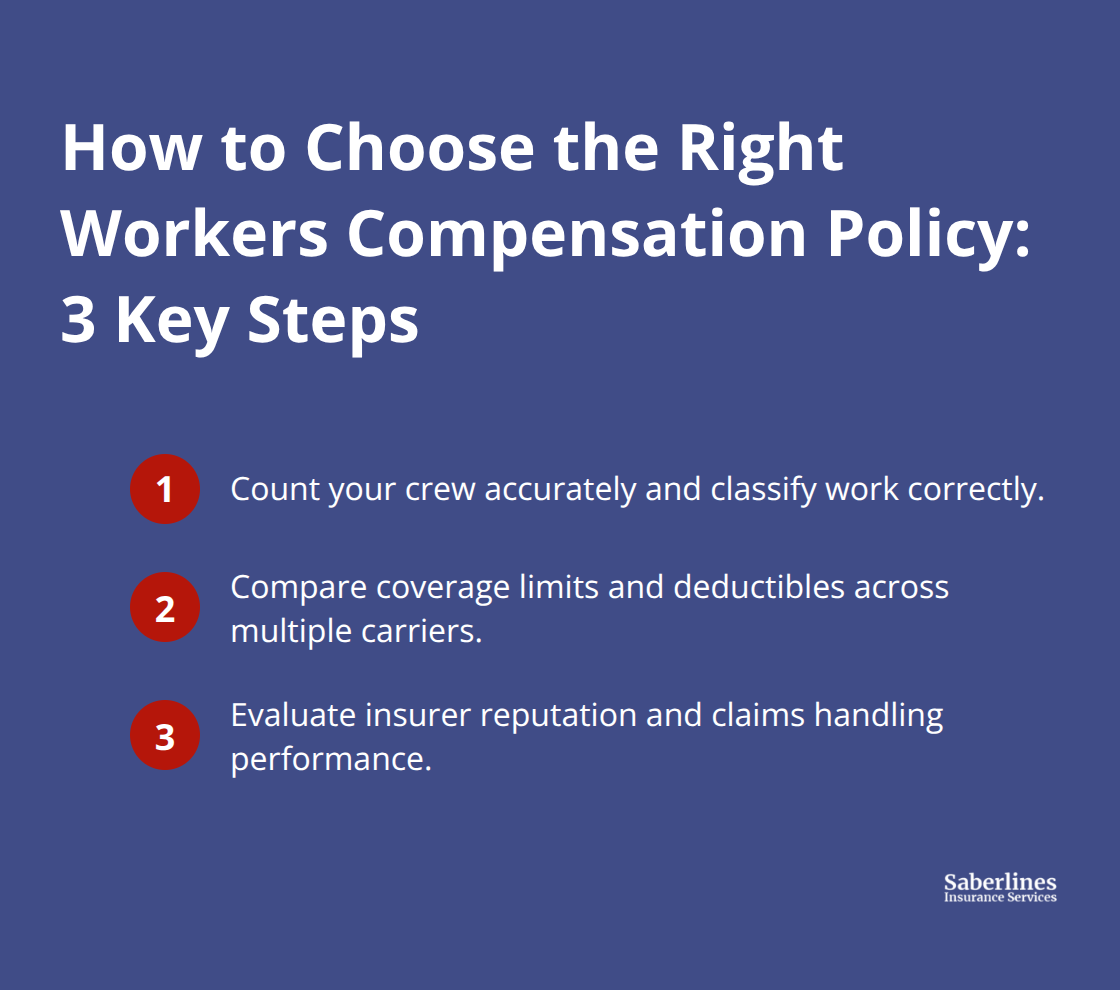

How to Choose the Right Workers Compensation Policy

Count your crew accurately and classify work correctly

Start with your actual crew size and the specific work your team performs, because these two factors drive everything else in your policy selection. A five-person drywall crew operates in a completely different risk environment than a ten-person excavation team, and your policy needs to reflect that reality. Most contractors underestimate their true crew size when shopping for coverage, forgetting to count seasonal workers, apprentices, or subcontractors they regularly hire. Count every person who works under your direction or uses your equipment, then verify with your insurance agent that your classification matches how your crew actually works.

The National Council on Compensation Insurance tracks injury rates by specific occupation, so a crew doing roofing work faces dramatically different hazard exposure than one doing general carpentry. When you shop for quotes, carriers will ask detailed questions about job classifications, and your honest answers directly impact both your premium and your actual coverage. Misrepresenting crew duties to get cheaper premiums creates a gap that leaves you unprotected when a claim happens.

Compare coverage limits and deductibles across multiple carriers

Coverage limits and deductibles require careful comparison across multiple carriers because the savings from a higher deductible often disappear when claims hit your business. Get quotes from at least three major carriers like Travelers, Hartford, or AmTrust, since the 2024 workers compensation market remains highly competitive with ample capacity, giving you real negotiating power.

Request identical coverage scenarios from each carrier so you can compare apples to apples, not just premium amounts.

Ask each insurer about their claims handling speed, their occupational medicine networks, and whether they offer return-to-work program support, since these factors determine how quickly your crew returns to work after an injury. Carriers increasingly use data-driven risk assessment and safety program reviews during underwriting, so document your safety training, incident prevention measures, and any certifications your crew holds. A strong safety program directly lowers your renewal costs, so asking about premium discounts for documented hazard training or equipment investments pays off.

Evaluate insurer reputation and claims handling performance

Before committing to any policy, read the exclusions carefully and discuss typical scenarios with your agent in plain language, confirming exactly what happens when someone gets injured on your most common job types. The insurer’s reputation for handling contractor claims matters more than saving fifty dollars monthly on premiums if they delay claim processing when your crew needs help. Your crew members know whether you have their backs when something goes wrong, and that knowledge directly impacts job satisfaction, productivity, and your ability to attract skilled workers.

Final Thoughts

Contractor workers compensation insurance protects your crew and your business when injuries happen on the job. The coverage pays for medical treatment your health plan won’t touch, replaces lost wages during recovery, and shields your business from direct liability claims that could exceed your annual revenue. State requirements vary significantly, and penalties for non-compliance range from thousands to tens of thousands of dollars depending on your location.

Securing the right coverage starts with counting your crew accurately and classifying their work correctly, since these factors drive both your premium and your actual protection. Get quotes from multiple carriers like Travelers, Hartford, and AmTrust to compare coverage limits, deductibles, and claims handling performance across identical scenarios. Ask about premium discounts for documented safety programs, occupational medicine networks, and return-to-work support, since these factors determine how quickly your crew recovers and returns to work.

Read policy exclusions carefully and discuss typical injury scenarios with your agent in plain language before committing to any policy. The insurer’s reputation for handling contractor claims matters more than saving money on monthly premiums if they delay processing when your crew needs help. Contact Saberlines Insurance Services today to get quotes and find the right workers compensation policy for your crew.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.