NEMT Fleet Insurance: Coverage for Your NEMT Fleet

NEMT operators face unique insurance challenges that standard commercial policies often miss. Medical transport vehicles carry vulnerable passengers, require strict regulatory compliance, and operate in high-risk environments.

At Saberlines Insurance Services, we’ve seen how the right NEMT fleet insurance protects your business from accidents, liability claims, and compliance violations. This guide walks you through the coverage types you need, the risks you face, and how to select the best protection for your fleet.

What Coverage Do You Actually Need for Your NEMT Fleet?

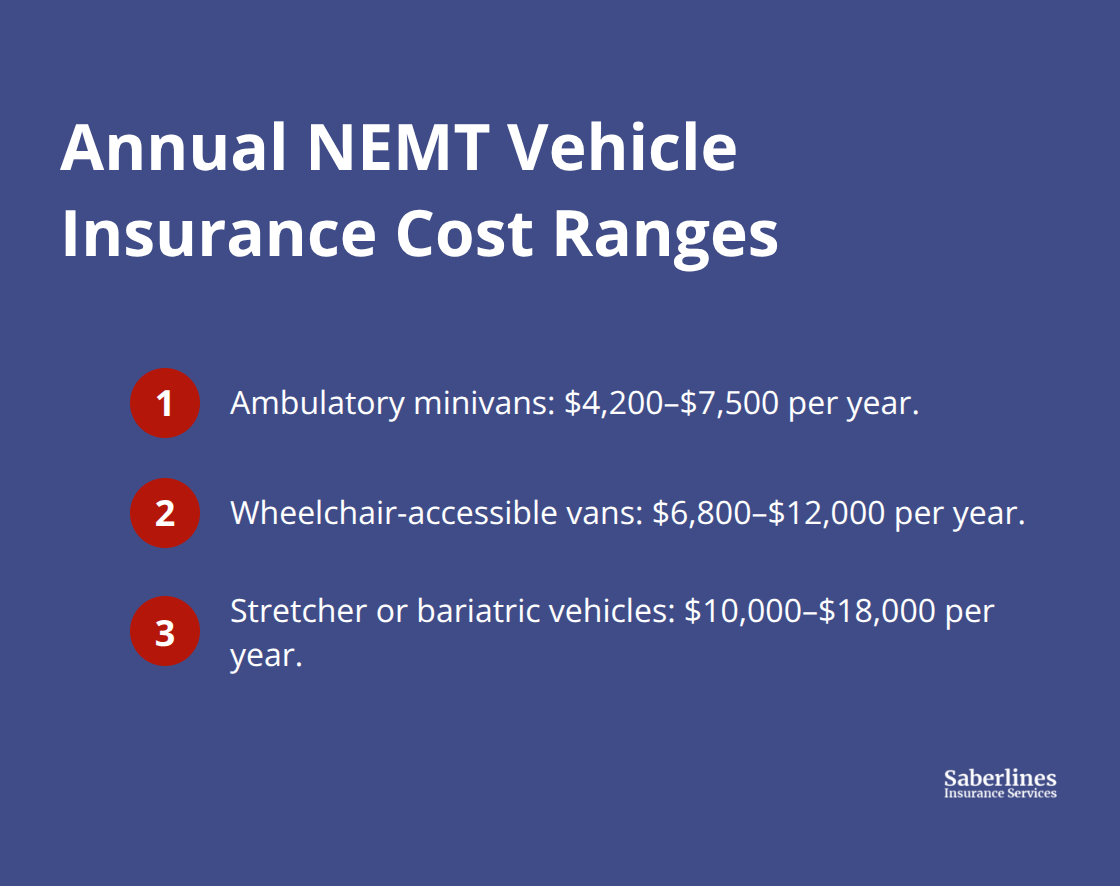

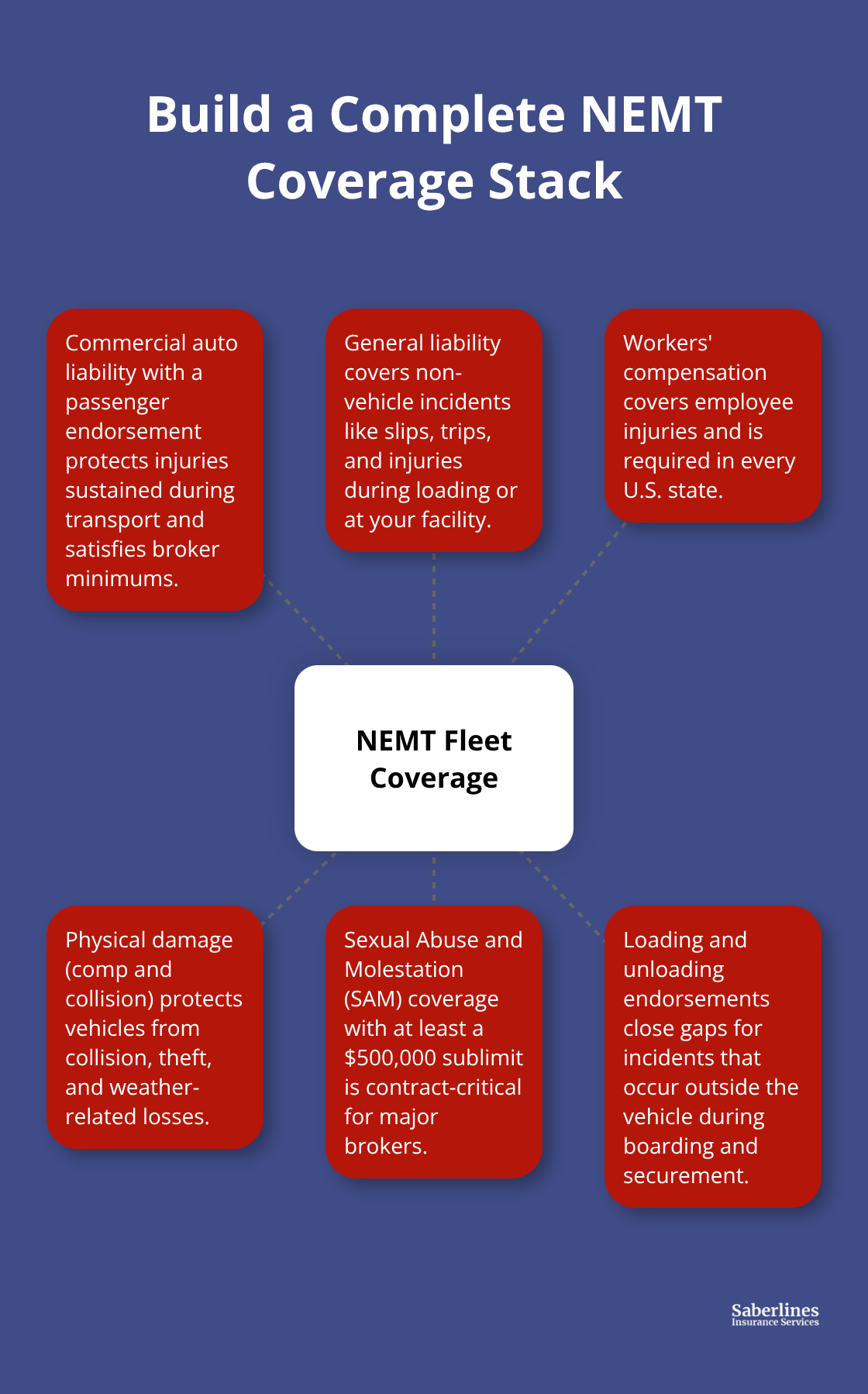

NEMT fleets require a multi-layered insurance stack because standard commercial auto policies exclude medical transport risks. Commercial auto liability with a passenger endorsement forms the foundation, protecting you when a patient sustains injury during transport. Federal minimums under FMCSA 49 CFR Part 387 require $1.5 million combined single limit for fleets carrying 1–15 passengers, though Medicaid brokers like ModivCare and MTM typically mandate $1 million CSL as a baseline. In 2026, commercial auto liability alone costs $4,200–$7,500 annually for ambulatory vans, $6,800–$12,000 for wheelchair-accessible vehicles, and $10,000–$18,000 for stretcher vans. Physical damage coverage protects your vehicles from collision, theft, and weather damage; new operators should select deductibles between $500 and $2,500, with higher deductibles lowering premiums by 10–15%. General liability coverage ($1 million/$2 million) covers non-vehicle incidents like a patient falling inside your facility or sustaining injuries during loading and unloading-this is separate from auto liability and costs $1,000–$1,500 annually per vehicle.

Loading and Unloading Endorsements Protect Against Hidden Gaps

Loading and unloading endorsements are non-negotiable for NEMT operators. Standard auto policies exclude injuries that occur outside the vehicle, which means a patient who falls while boarding your van or during wheelchair securement would face claim denial without this rider. Medicaid brokers require door-to-door service endorsements explicitly, and claims data shows loading and unloading incidents represent 25–40% of NEMT liability claims. You also need a Sexual Abuse and Molestation (SAM) rider with a minimum $500,000 sublimit; major brokers will not sign contracts without it. Hired and Non-Owned Auto coverage protects you when drivers use personal vehicles for medical transport, which is common for small operators adding capacity. Workers’ compensation is mandatory in every state and covers driver injuries; new operators budget $1,500–$2,000 annually per driver. The complete stack typically runs $8,000–$15,000 per vehicle per year when bundled with one carrier, compared to $18,000–$25,000 when policies scatter across multiple insurers with coverage gaps.

Location and Vehicle Type Drive Premium Differences

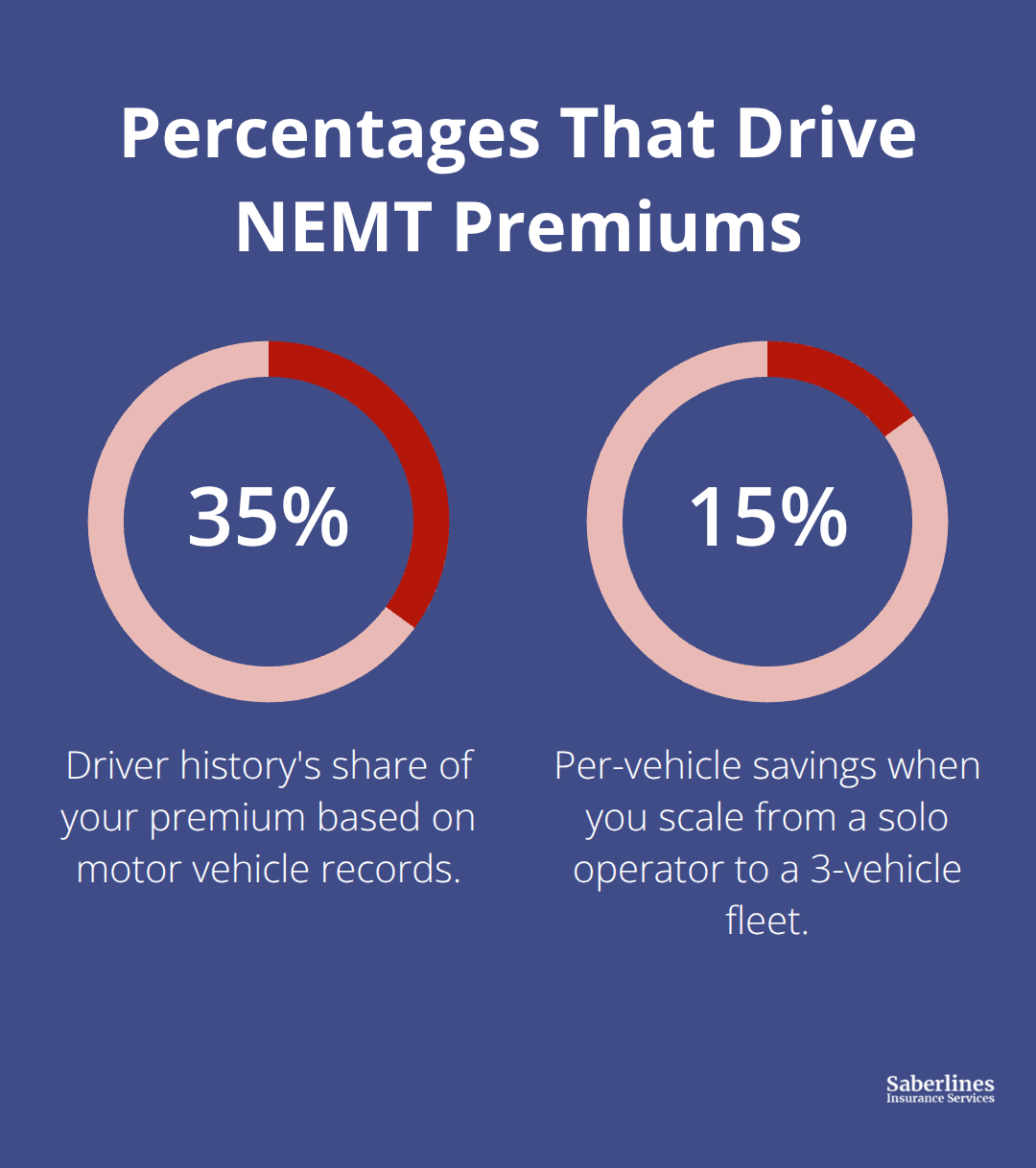

Your garaging address and vehicle type determine 40–50% of your premium. Urban operators in California or New York pay 30–170% more than rural operators in South Dakota or Montana; a 20-mile shift in garaging location can save $2,000 per vehicle annually. Wheelchair-accessible vans incur 15–30% surcharges over standard vans due to lift equipment complexity and securement liability. Fleet size also matters significantly: solo operators pay the highest per-vehicle rate, while fleets of 3 vehicles see 15% savings, 6–10 vehicles see 20–30% savings, and 10+ vehicles can reach 40%+ savings. New operators face a 30–50% surcharge until they establish two years of clean claims history.

Driver History and Safety Investments Lower Your Costs

Driver history carries the most weight in underwriting-about 35% of your premium depends on your drivers’ motor vehicle records. Installing GPS telematics and dual-facing dashcams can reduce premiums by 15–30%, while PASS certification for all drivers yields 5–10% savings and reduces loading and unloading claims by 25–40%.

Paying your annual premium in full rather than monthly installments saves 5–8%, and bundling all coverages with one NEMT-focused carrier typically yields 10–25% savings versus piecing together policies from generalist insurers. These cost-reduction strategies compound over time, especially when you maintain clean claims history and invest in driver training programs.

Understanding your coverage needs sets the stage for selecting the right insurance partner. The next section walks you through how to evaluate fleet size, compare coverage options, and work with specialized providers who understand NEMT operations.

Common Risks NEMT Fleets Face

NEMT fleets operate in an environment where injury claims routinely exceed standard commercial auto incidents by tenfold. Average NEMT injury claims run $150,000–$500,000 compared to standard auto claims around $12,000–$50,000, which is why insurers scrutinize NEMT operators so heavily. Accidents occur in medical transport, but the liability exposure extends far beyond typical vehicle collisions. A patient with a heart condition who experiences a medical event during transport, a wheelchair that fails during loading, or a driver error that causes a fall inside your van can all trigger catastrophic claims. What separates operators who survive these incidents from those who face financial ruin is having the right coverage in place before the claim happens.

Accidents and Collision Claims Create Compounding Liability

Most NEMT operators underestimate their actual risk exposure because they focus only on collision damage rather than the full spectrum of liability that medical transport creates. Insurance data shows that loading and unloading incidents alone account for 25–40% of NEMT liability claims, yet many operators carry minimal coverage for these exposures. A single uninsured loading incident can wipe out years of profit and expose your personal assets to judgment. Your passengers are medically fragile, your drivers operate under time pressure, and your vehicles carry equipment that creates additional liability. This combination demands comprehensive coverage that most standard commercial policies simply do not provide.

Premium Increases Follow Claims Quickly

Your premiums reflect this elevated risk profile. Only about 30 carriers write NEMT coverage nationwide, which means limited competition and higher pricing for everyone in the space. A single at-fault claim increases your premiums by 30–50%, while two claims in three years push you to the surplus lines market where premiums jump another 40–80%. New operators face 30–50% surcharges for the first two to three years because underwriters have no loss history to assess your actual risk. Once you establish clean claims history, premiums decline gradually: roughly 15–25% reduction after Year 1, 10–20% after Year 2, and 10–15% after Year 3.

Safety Investments Pay Dividends Through Lower Costs

Your insurance costs respond directly to how safely your fleet operates. Investing in driver training, telematics systems that provide real-time monitoring, and documented safety protocols pays dividends through lower premiums and fewer incidents. Installing GPS telematics and dual-facing dashcams can reduce premiums by 15–30%, while PASS certification for all drivers yields 5–10% savings and reduces loading and unloading claims by 25–40%.

Regulatory Compliance Violations Trigger Coverage Lapses

Regulatory compliance violations add another layer of risk. State Medicaid agencies and major brokers like ModivCare, MTM, and Veyo impose strict insurance requirements, and lapses in coverage trigger immediate suspension from trip assignments. A coverage gap lasting just 24 hours can cost you thousands in lost revenue and damage your relationships with payers. Your coverage stack must match both federal minimums and broker-specific mandates to avoid gaps that could devastate your operation. Understanding these overlapping risks positions you to make informed decisions about the coverage options and deductibles that actually protect your fleet.

Selecting the Right NEMT Insurance Partner

Match Your Fleet Size to the Right Insurance Program

Fleet size and vehicle composition determine which insurance programs work for your operation. A solo operator running one wheelchair-accessible van faces completely different underwriting than a five-vehicle fleet mixing ambulatory vans and stretcher vehicles. Solo operators pay the highest per-vehicle rates and should expect to budget $11,300–$15,000 annually for a single wheelchair van in Texas when you bundle auto liability, general liability, workers compensation, and physical damage. Fleets of three vehicles see roughly 15% per-vehicle savings, while fleets of 6–10 vehicles unlock 20–30% savings, and operators with 10+ vehicles can reach 40% or more in cumulative savings.

National Interstate Mobility℠, a group captive program established in 2022, offers collateral-friendly terms and no upfront capitalization for fleets committed to safety culture. Membership includes potential financial returns and networking opportunities at bi-annual meetings. If you operate 25 or more vehicles, large account customization programs exist that structure single-account rentals or member-owned captives with large deductibles tailored to your specific risk tolerance.

Account for Vehicle Type in Your Budget

The vehicle types within your fleet directly impact your annual costs. Ambulatory minivans and standard vans run $4,200–$7,500 annually, wheelchair-accessible vans $6,800–$12,000, and stretcher or bariatric vehicles $10,000–$18,000. Comparing quotes across three to five providers gives you real pricing data rather than assumptions.

Specialty NEMT brokers deliver 15–30% savings versus generalist insurers by accessing NEMT-only programs unavailable to the broader market, so verify that any broker you contact handles NEMT as a meaningful share of their business.

Structure Your Coverage and Deductibles Strategically

Coverage options and deductibles must align with both your risk tolerance and your Medicaid broker contracts. Higher deductibles lower premiums by 10–15%, but they also increase your out-of-pocket exposure when claims occur; most new operators select $500 to $2,500 deductibles to balance affordability with manageable risk. Paying your annual premium in full rather than monthly installments saves 5–8%, while bundling all coverages with one NEMT-focused carrier yields 10–25% savings compared to splitting policies across multiple insurers.

Your coverage stack should include commercial auto liability with passenger endorsement, general liability, workers compensation, physical damage, sexual abuse and molestation coverage with a $500,000 minimum sublimit, hired and non-owned auto coverage, and loading and unloading endorsements. Medicaid brokers like ModivCare typically require $1 million CSL auto liability, while MTM and Veyo may demand $1.5 million CSL, so review your contracts before finalizing quotes.

Navigate the Quote and Binding Process

Request sample certificates of insurance from each provider to confirm they include all required endorsements and primary language before you bind coverage. The quote process typically takes 24–72 hours once you submit your LLC documentation, garaging address, vehicle details, driver motor vehicle records, loss runs, and active Medicaid contracts; binding usually follows within 3–7 days if you approve the terms. Saberlines Insurance Services specializes in NEMT and passenger transportation coverage and can help you navigate these overlapping requirements.

Final Thoughts

NEMT fleet insurance protects your operation from the financial devastation that medical transport claims inflict. The coverage stack you build today determines whether a single incident becomes a manageable loss or a business-ending catastrophe. Your fleet carries medically fragile passengers, operates under regulatory pressure, and faces liability exposure that standard commercial policies explicitly exclude-a reality that demands specialized coverage accounting for loading and unloading incidents, passenger injury claims exceeding $150,000, and broker-specific mandates varying by state and payer.

Budget $8,000–$15,000 per vehicle annually for comprehensive NEMT fleet insurance when bundled with one carrier, and expect higher costs in California, New York, or Florida. New operators face 30–50% surcharges until they establish clean claims history, but those surcharges decline predictably as you build your track record. Installing telematics systems, certifying drivers in safety training, and maintaining detailed loss runs accelerates your path to lower premiums and demonstrates to underwriters that you take risk seriously.

Specialty NEMT brokers deliver 15–30% savings by accessing programs unavailable to the broader market and navigate the overlapping requirements imposed by Medicaid brokers, state agencies, and federal regulations. Request quotes from three to five providers, compare coverage completeness rather than price alone, and verify that all required endorsements appear on your certificates of insurance before you bind. Saberlines Insurance Services specializes in NEMT and passenger transportation coverage and can help you build a coverage stack that protects your assets while keeping your premiums manageable.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.