Commercial Auto Insurance Fleets: Fleet-Scale Protection for Operators

Running a fleet means managing dozens of moving parts, and your insurance is one of the most critical decisions you’ll make. Commercial auto insurance for fleets protects your business from liability claims, vehicle damage, and gaps that could cost you thousands.

At Saberlines Insurance Services, we’ve seen operators lose money because they didn’t understand their coverage options or missed essential protections. This guide walks you through what you actually need, how to cut costs without cutting corners, and the coverage gaps that catch most fleet operators off guard.

What Your Fleet Insurance Actually Covers

Liability Coverage Protects You From Third-Party Claims

Liability coverage sits at the foundation of any fleet policy, and you cannot skimp on it. This covers bodily injury and property damage when one of your drivers causes an accident. The problem we see constantly is that operators stick with state minimums, which in most states range from $25,000 to $50,000 per person. That sounds adequate until a serious injury case lands on your desk and medical bills exceed $200,000. Texas minimums, for instance, are often insufficient for many businesses operating beyond basic delivery. You should carry limits of at least $250,000 per person and $500,000 per accident, though high-value cargo operations or passenger transport should push toward $1 million. The industry standard benchmark sits around $1,000 per vehicle annually, but inadequate liability limits leave you personally liable for anything above your policy ceiling.

Physical Damage Coverage Protects Your Vehicles

Physical damage coverage protects your actual vehicles through two components: collision handles accidents with other vehicles or objects, while comprehensive covers theft, vandalism, hail, and weather damage. Your deductible choice directly impacts your premium, and this is where fleet operators make their biggest mistake. Increasing your deductible from $500 to $2,500 can reduce premiums significantly, but only if your cash flow can absorb that out-of-pocket hit when damage occurs. A fleet of 10 vehicles might save $1,500 to $3,000 annually with higher deductibles, but one major incident could wipe out those savings. You should match your deductible to what you can actually pay without disrupting operations, not just what sounds good on paper.

Uninsured and Underinsured Motorist Coverage Fills Critical Gaps

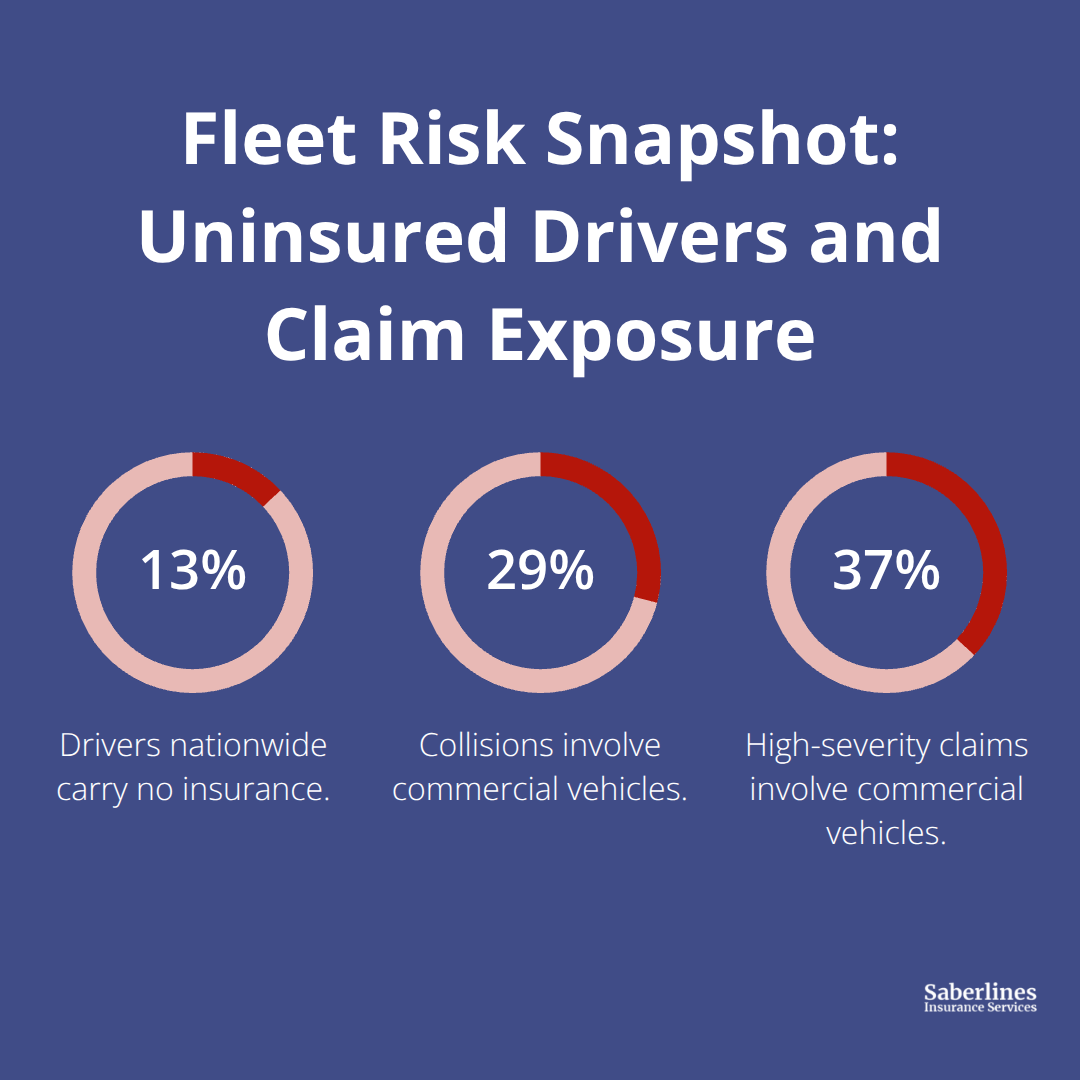

Uninsured and underinsured motorist coverage fills a gap that shocks most fleet operators when they finally need it. This protects your drivers and business when another driver causes an accident but lacks sufficient insurance to cover damages. Roughly 13% of drivers nationwide carry no insurance, so this isn’t theoretical protection. If one of your vehicles gets hit by an uninsured driver and suffers $15,000 in damage, this coverage kicks in. Many operators overlook this or carry minimal limits, thinking it’s redundant with their collision coverage. The difference is critical: collision covers accidents you cause, while uninsured motorist covers accidents caused by underinsured or hit-and-run drivers. You should set these limits equal to your liability limits for consistent protection.

For fleets operating in urban logistics environments, where accident exposure runs higher due to congestion and delivery density, this coverage becomes even more valuable. The data shows commercial vehicles account for roughly 29% of collisions and 37% of high-severity claims, so the probability of encountering an uninsured driver increases with fleet size and mileage. Understanding these three core protections sets the stage for the next critical decision: how to control your costs without sacrificing the protection your fleet actually needs.

How Driver Records and Maintenance Shape Your Fleet Costs

Driver Safety Records Drive Premium Changes

Your drivers determine your premiums more than anything else, and this is where most fleet operators leave money on the table. Driver safety records sit at the top of the cost hierarchy because insurers track moving violations, accidents, and claims history for every operator on your policy. A single driver with two at-fault accidents in the past three years can increase your fleet premium by 15% to 25%, even if the rest of your team maintains clean records.

The NAIC found that well-maintained vehicles and safe driving records directly negotiate lower premiums, which means investing in driver training programs returns measurable savings.

Formal safety training that covers defensive driving, hazard recognition, and load securing typically reduces accident frequency by 10% to 15%, and insurers reward this with tangible rate reductions. If you operate a fleet of 10 vehicles, a 15% premium reduction on a $10,000 annual policy saves you $1,500 yearly-enough to cover the cost of a professional training program with room to spare. The counterintuitive insight most operators miss is that removing a high-risk driver from your policy often costs less than keeping them insured, so don’t hesitate to make that change.

Vehicle Age and Maintenance History Lower Claim Costs

Vehicle age and maintenance history function as a secondary but equally important cost lever. Modern commercial vehicles contain over 120 electronic components, and repair costs run about 31% higher than they did in 2015, which means well-maintained fleets face dramatically lower claim costs. Insurers scrutinize maintenance records during underwriting, and documented service history for oil changes, brake inspections, tire rotations, and fluid checks can reduce your premium by 5% to 10%.

Older vehicles, particularly those over seven years old, typically cost 20% to 30% more to insure because repair expenses climb and safety systems become outdated. If your fleet mixes newer and older vehicles, consider replacing high-mileage units strategically rather than spreading maintenance costs across aging assets. Refrigerated trucks and specialized vehicles add complexity; refrigerated units can increase fleet premiums by up to 25% relative to standard delivery vans due to higher cargo risk, so factor this into your vehicle selection decisions.

Bundling and Strategic Coverage Decisions Compound Savings

Bundling your fleet policy with general liability or workers compensation coverage unlocks 5% to 10% discounts on total insurance costs, which compounds savings across your entire business insurance footprint. These layered discounts add up quickly when you consolidate multiple policies under one provider rather than spreading coverage across different insurers. The next section examines the specific coverage gaps that catch fleet operators off guard and cost them thousands when claims arise.

Coverage Gaps That Cost Fleet Operators Thousands

High-Value Cargo Requires Liability Limits That Match Your Exposure

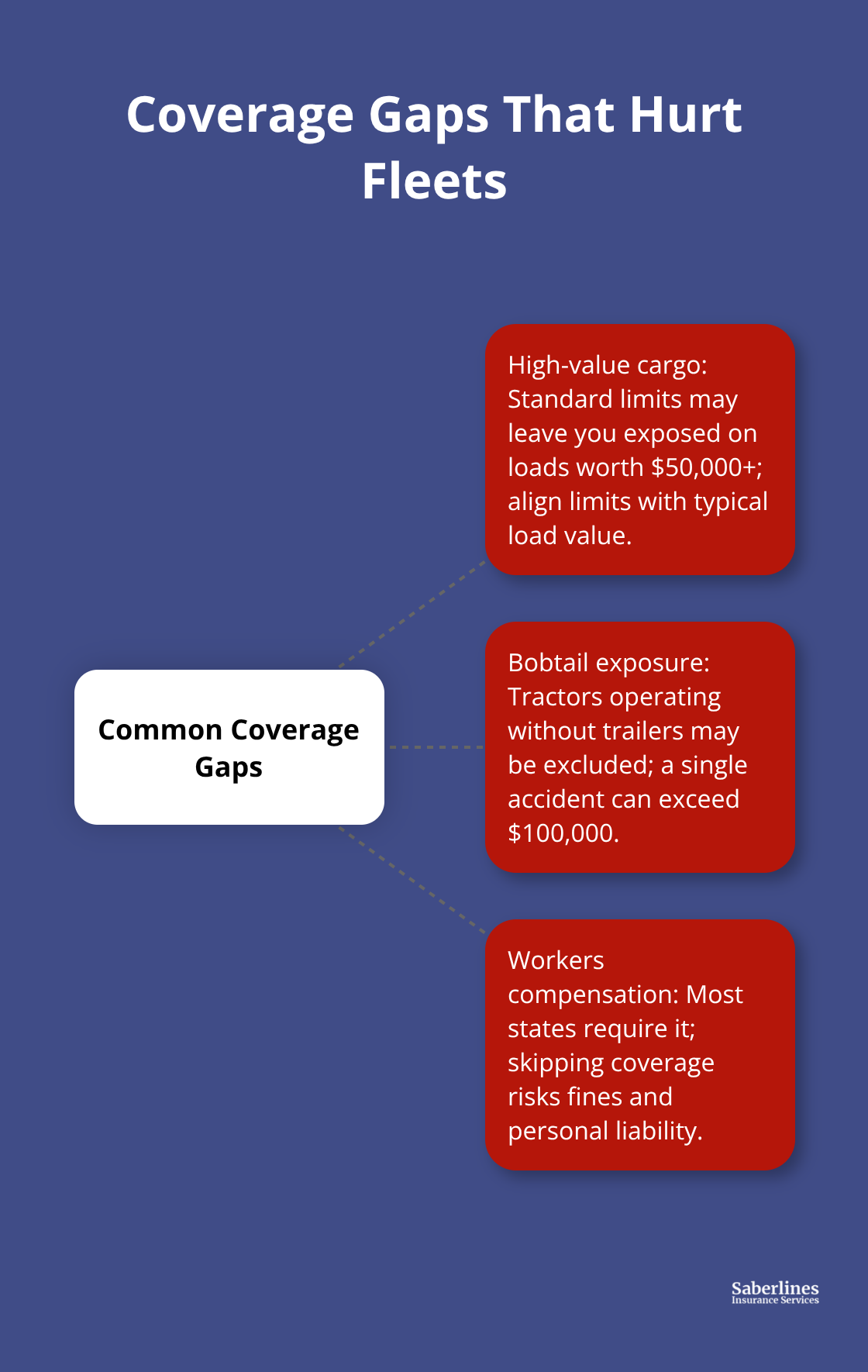

Most fleet operators discover their coverage gaps only after an accident happens, and by then the financial damage is done. High-value cargo operations represent the first major blind spot we encounter regularly. If you transport electronics, pharmaceuticals, or machinery worth $50,000 or more per load, standard liability limits expose you to catastrophic loss. A cargo worth $75,000 damaged in transit leaves you personally liable for the difference between what your policy covers and what the customer demands. Your liability ceiling should match or exceed your typical cargo value, not fall $30,000 short.

Operators moving valuable freight typically need liability limits between $500,000 and $2 million, depending on cargo type and route, yet many carry limits designed for basic delivery services. This mismatch costs operators money when claims exceed coverage, forcing out-of-pocket settlements that destroy cash flow. Cargo-specific endorsements add minimal cost, usually $200 to $500 annually, but protect against losses that could exceed your annual profit margin.

Bobtail Coverage Protects Tractors Operating Without Trailers

Owner-operators and small fleet owners face a second critical gap that bobtail coverage addresses directly. Bobtail insurance covers your tractor when it operates without a trailer attached, whether you travel to pick up a load, return from delivery, or reposition equipment. Many operators believe their standard commercial auto policy covers this movement, then face claim denials when an accident occurs during bobtail operation. The gap exists because standard fleet policies often exclude or limit coverage for tractors operating unloaded, treating bobtail as a separate exposure requiring dedicated protection.

A single bobtail accident involving injury can cost $100,000 or more in liability claims, and without proper coverage your business absorbs the full amount. Bobtail policies typically cost $600 to $1,200 annually for owner-operators, making it one of the most cost-effective protections available relative to the exposure it covers. If you operate any type of tractor or heavy equipment, bobtail coverage is non-negotiable regardless of your other policies.

Workers Compensation Protects Employees and Your Business

The final gap involves workers compensation, which many fleet operators overlook because they assume it falls under a separate policy. Workers compensation covers medical expenses and lost wages when an employee gets injured during work, and most states require it for any business with employees. Operating without it exposes you to personal liability for injuries, fines reaching $10,000 or more per violation, and potential license suspension.

Some operators think they can avoid workers compensation by classifying employees as independent contractors, but state labor boards increasingly challenge this classification and impose retroactive liability. If your fleet has even one employee beyond yourself, workers compensation is mandatory, not optional, and bundling it with your fleet policy typically reduces your overall insurance costs by 5% to 10% compared to separate policies. Saberlines Insurance Services specializes in helping owner-operators and fleets secure workers compensation coverage alongside commercial auto and other protections to keep your business compliant and protected.

Final Thoughts

Your commercial auto insurance for fleets protects your business only when coverage limits match your actual exposure and gaps don’t exist to surprise you later. Start this week by pulling your declarations pages and verifying liability limits against your typical cargo value and route risk. Check whether bobtail coverage appears on your policy if you operate tractors, confirm workers compensation is active, and document your vehicle maintenance records because these directly influence your next renewal quote.

Shopping your coverage with insurers who specialize in transportation makes a measurable difference because general commercial agents often miss industry-specific exposures that matter. Specialized carriers understand that refrigerated trucks operate differently than standard delivery vans, that owner-operators face unique bobtail exposure, and that driver safety programs generate measurable premium reductions. We at Saberlines Insurance Services work with owner-operators and fleets to secure commercial auto, cargo, bobtail, and workers compensation coverage that actually fits your operations-visit https://saberlinesins.com to explore how we can help you evaluate your current coverage and find better rates.

Your fleet’s profitability depends on treating insurance as a strategic asset rather than a line item to minimize, which means controlling costs while maintaining the protection that keeps your business running when accidents happen. The operators who thrive are those who take action this week to review their policies, identify gaps, and connect with an insurer who understands transportation risk.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.