Non Emergency Medical Transport Insurance: Essential Protections

Non-emergency medical transport operators face unique liability challenges that standard business insurance simply doesn’t cover. From patient injuries to vehicle accidents, the risks are real and costly.

At Saberlines Insurance Services, we understand that proper non-emergency medical transport insurance protects your business, your staff, and your patients. This guide walks you through the coverage types, regulations, and protections you need.

What Coverage Do You Actually Need for NEMT Operations

Commercial Auto Liability: The Foundation

Commercial auto liability forms the foundation of NEMT insurance, and the minimums shift based on your operating model. Federal FMCSA standards under 49 CFR Part 387 require interstate carriers with 1–15 passengers to carry at least 1.5 million in liability coverage, while intrastate operators follow state rules that often demand 1 million combined single limit. Medicaid brokers like ModivCare and MTM impose higher thresholds: they require 1 million in auto liability plus 1 million per occurrence and 2 million aggregate in general liability before they contract with you. Your coverage stack directly determines which payers will accept your trips.

Protecting Against Employee-Owned Vehicles

Most NEMT operators lease vehicles or rely on employee-owned cars for overflow capacity, which is why hired and non-owned auto coverage matters. A single at-fault collision without this endorsement can bankrupt a small operation. Claims costs for NEMT passengers run 2–5 times higher than standard auto claims because patients are medically fragile and settlements reflect that vulnerability. This endorsement protects your business when you don’t own the vehicle but still bear liability for the transport.

The Loading and Unloading Exposure

Forty to sixty percent of NEMT claims occur during loading and unloading-the curb-gap exposure that standard auto policies explicitly exclude. General liability coverage fills this gap and protects against passenger injuries that happen outside the vehicle. Workers’ compensation is federally mandatory if you employ drivers or aides, and it covers on-the-job injuries from the physical demands of assisting passengers in and out of vehicles.

Wheelchair-Accessible Vehicle Premiums

Wheelchair-accessible vehicles carry 15–30% premium surcharges because lift mechanisms, ramp systems, and securement equipment increase repair costs and complexity. Typical annual costs for a single vehicle range from 3,500 to 8,500 for auto liability alone; wheelchair-accessible vehicles run 565–1,000 monthly, with full coverage bundles reaching 5,000–15,000 per vehicle annually depending on location and claims history.

Regional Cost Variations

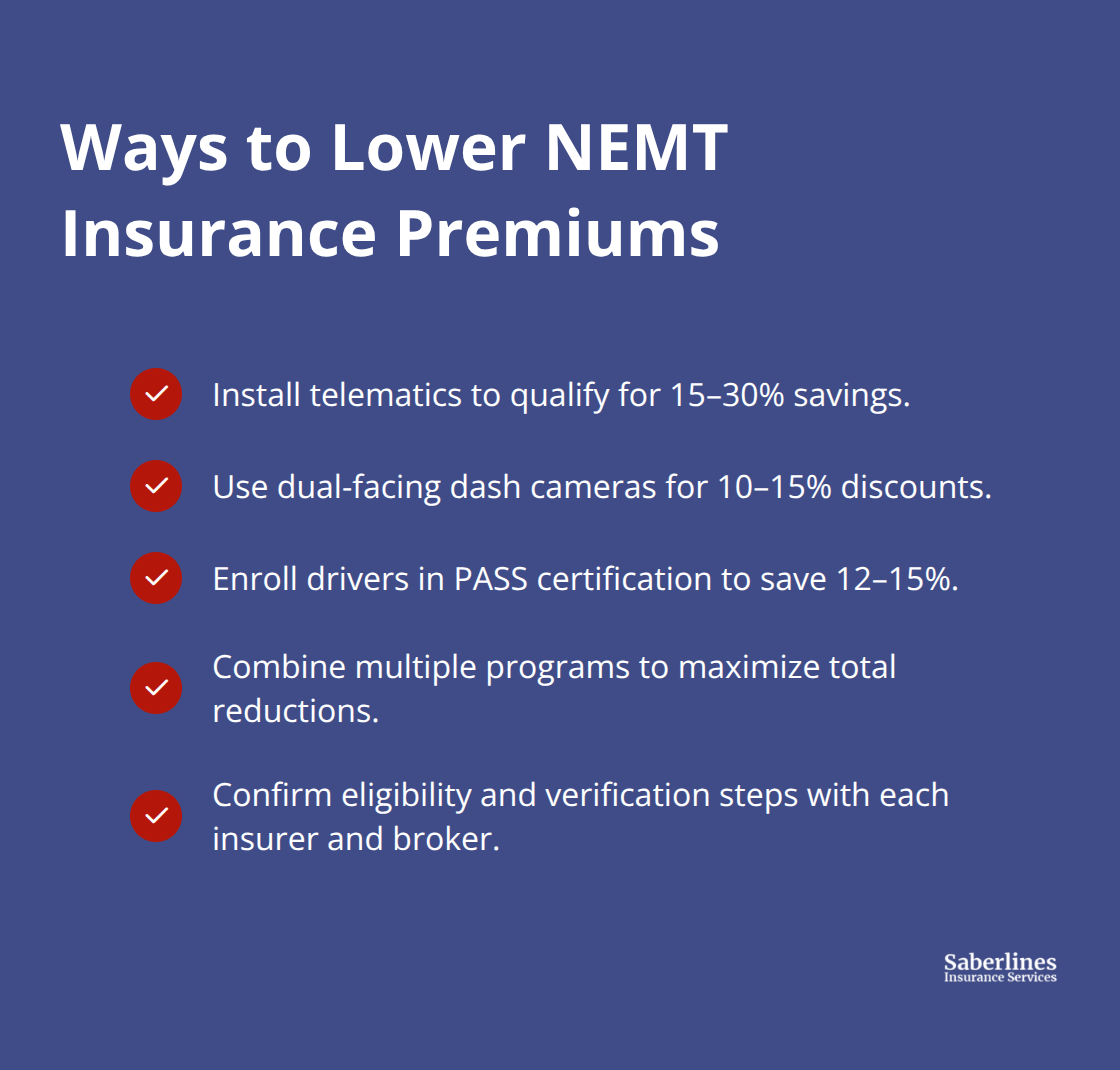

California and Florida operators pay significantly more-5,500–9,000 annually in California and 5,000–8,500 in Florida-because these states have higher litigation costs and no-fault insurance rules that inflate premiums. Telematics discounts (15–30% savings), dual-facing dash cameras (10–15%), and PASS driver certification programs (12–15%) help operators reduce these costs. Understanding your state’s specific requirements and available discounts shapes your total cost of coverage and determines which payers will work with you.

Common Risks in Non-Emergency Medical Transport

Patient Injuries During Loading and Unloading

Patient injuries during transport represent the costliest exposure in NEMT operations, and they rarely occur where operators expect them. Data shows 40–60% of claims happen during loading and unloading, not while the vehicle moves. A patient falls during the transfer from wheelchair to vehicle seat, or an aide’s back gives out lowering a stretcher-these moments create liability spikes that standard commercial auto policies explicitly exclude. The curb-gap exposure exists because the patient stands outside the vehicle but remains under your care. Claims involving medically fragile passengers run 2–5 times higher than standard auto claims because settlements reflect the patient’s vulnerability and existing health conditions. A simple fall that might cost 5,000 in a standard passenger transport case can balloon to 50,000 or more when the patient has diabetes, osteoporosis, or cardiovascular disease.

General liability coverage with passenger injury protection fills this gap and protects against injuries that auto liability misses.

Vehicle Collisions and Passenger Vulnerability

Vehicle accidents and collisions compound your exposure because NEMT passengers cannot brace themselves during impact the way healthy passengers can. Older adults with arthritis, patients on dialysis, or individuals with neurological conditions suffer disproportionate injury severity in even low-speed collisions. The fragility of your passenger population means that impact forces that cause minor injuries in standard auto claims trigger severe outcomes in NEMT cases. This vulnerability directly affects claim costs and your renewal premiums.

Regulatory Compliance and Audit Risk

Regulatory compliance violations carry separate financial penalties and contract termination risk. Medicaid audits focus heavily on trip documentation, driver qualifications, and vehicle maintenance records. A single audit finding-missing background check documentation, incomplete trip logs, or a vehicle inspection gap-can trigger payment denials on dozens of trips and disqualify you from future Medicaid contracts. State licensing boards impose fines ranging from 1,000 to 10,000 for violations, and repeat offenses result in license suspension. The U.S. Department of Transportation emphasizes data accuracy and mobility compliance as core oversight priorities. This means your documentation systems must be audit-ready from day one, not scrambled together when an auditor arrives.

Documentation as Operational Foundation

Operators who treat compliance as a back-office task rather than an operational foundation pay the price through denied claims, contract losses, and premium increases after violations surface. Your audit-ready driver qualification files, trip logs, and vehicle inspection records protect you from these cascading financial and contractual consequences. The cost of building compliant systems upfront is far lower than the cost of recovering from audit failures and contract termination. These risks shape not only your insurance needs but also your operational strategy moving forward.

Industry Requirements and Regulations

Federal and state regulations create a complex compliance landscape that directly affects your insurance requirements and operating costs. The U.S. Department of Transportation enforces FMCSA standards under 49 CFR Part 387, which mandate minimum liability coverage based on passenger capacity and interstate versus intrastate operations. Interstate carriers transporting 1–15 passengers must carry 1.5 million in liability; those with 16 or more passengers need 5 million. Intrastate operators follow state-specific rules, but many states align with federal minimums or impose higher thresholds depending on Medicaid participation. Your state’s licensing board requires proof of insurance before issuing your NEMT permit, and that proof must match the specific coverage limits your state demands. CMS, which oversees Medicaid, treats NEMT as a mandatory benefit in most states, meaning state Medicaid programs enforce their own insurance and operational standards. This creates a three-layer compliance requirement: federal DOT rules, state licensing rules, and state Medicaid rules. Missing any single layer exposes you to fines, contract termination, and premium increases when violations surface during audits.

State Insurance Mandates Vary Significantly

Your state’s Medicaid program sets insurance thresholds that often exceed federal minimums. ModivCare and MTM, the largest Medicaid brokers, require 1 million combined single limit for commercial auto liability plus 1 million per occurrence and 2 million aggregate for general liability before they contract with you. Some states impose additional endorsements: hired and non-owned auto coverage, umbrella liability of 1–3 million, and assault and battery liability protection. California requires proof of workers’ compensation insurance before your NEMT license receives approval; Florida imposes higher premium minimums based on vehicle age and seating capacity. If you operate across multiple states, you must verify each state’s specific mandates rather than assuming one policy covers all jurisdictions. Many operators discover coverage gaps during Medicaid enrollment when brokers reject their policies for missing state-required endorsements. The cost of correcting these gaps mid-year often means policy amendments with backdated coverage or expensive policy cancellations and rebinding.

Documentation Systems Determine Your Audit Outcome

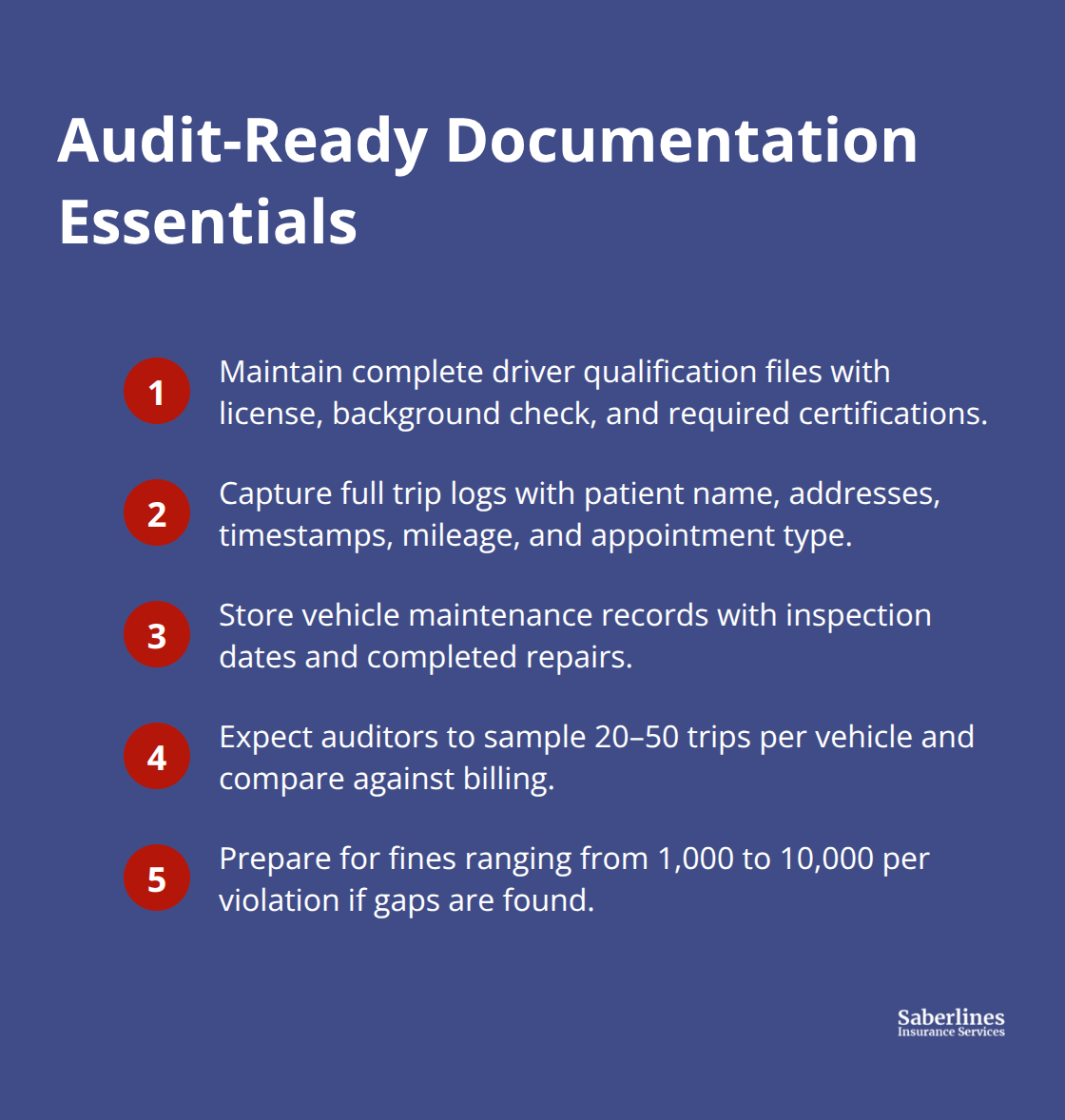

Medicaid audits focus on three compliance pillars: driver qualification files, trip documentation, and vehicle maintenance records. Your driver qualification file must include a valid driver’s license, background check results, and proof of any required training certifications within 30 days of hire. Trip logs must capture the patient’s name, pickup and dropoff addresses, time in and out, mileage, and the specific medical appointment type.

Vehicle maintenance records must show inspection dates and any repairs completed. Auditors examine 20–50 trips per vehicle and cross-reference them against your billing submissions. A single missing background check or incomplete trip log triggers a finding that can deny payment on entire trip batches. State licensing boards conduct compliance audits annually or when complaints arise, and violations carry fines from 1,000 to 10,000 per finding. Operators who treat documentation as a back-office task rather than a daily operational requirement face denied claims, contract suspension, and premium increases after audits conclude.

Build Audit-Ready Systems From Day One

Implement digital trip verification through your dispatch platform to capture all required data automatically. Maintain driver files in a centralized system with expiration alerts so certifications and background checks never lapse. Schedule monthly vehicle inspections with documented results and store records where auditors can access them quickly. This upfront investment costs far less than recovering from audit failures and contract losses. The operators who succeed in NEMT treat compliance as a core operational function, not a back-office burden, and their audit outcomes reflect that commitment.

Final Thoughts

Non-emergency medical transport insurance protects your vehicles, your staff, and your patients across three critical operational areas. The coverage stack-commercial auto liability, general liability, workers’ compensation, hired and non-owned auto coverage, and umbrella protection-addresses the specific risks that standard business policies ignore. Federal FMCSA standards set baseline minimums, but your state’s Medicaid program and payer contracts often demand higher limits, and wheelchair-accessible vehicles, regional cost variations, and claims history all shape your final premium.

Compliance systems matter as much as insurance itself. Audit-ready driver qualification files, trip logs, and vehicle maintenance records prevent denied claims and contract termination, while telematics, dash cameras, and PASS driver certification programs reduce your premiums and strengthen your operational foundation. The operators who succeed in NEMT treat non-emergency medical transport insurance and compliance as integrated business functions, not separate expenses.

We at Saberlines Insurance Services help NEMT operators and other transportation businesses secure the right coverage for their operations. Contact Saberlines Insurance Services today to get a quote tailored to your NEMT operation and state requirements.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.