General Liability Requirements 2026: What Has Changed and Why It Matters

General liability requirements 2026 have shifted significantly, and businesses that haven’t updated their policies are already falling behind. These changes affect your operating costs, legal exposure, and competitive standing in ways you can’t ignore.

At Saberlines Insurance Services, we’ve seen firsthand how quickly outdated coverage becomes a liability. This guide walks you through what’s changed and how to protect your business.

What’s Actually Changing in General Liability for 2026

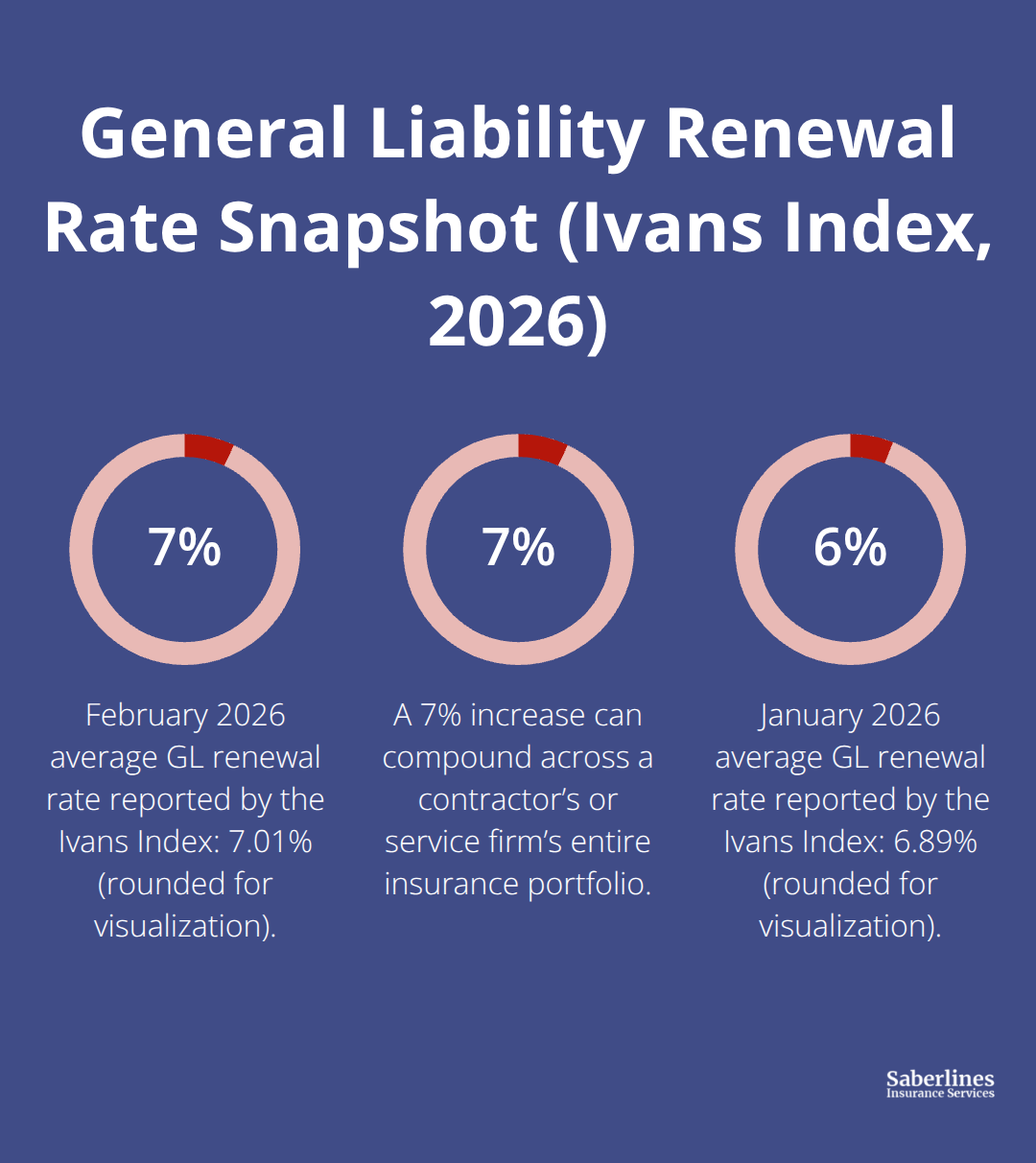

General liability pricing has stabilized compared to the hard market peaks of recent years, but don’t mistake stability for stagnation. The Ivans Index data from February 2026 shows general liability renewal rates at 7.01%, up from 6.89% in January, with year-over-year rates continuing to climb. Your renewal quote will likely be higher than last year, regardless of your claims history. The market is also tightening around emerging exposures.

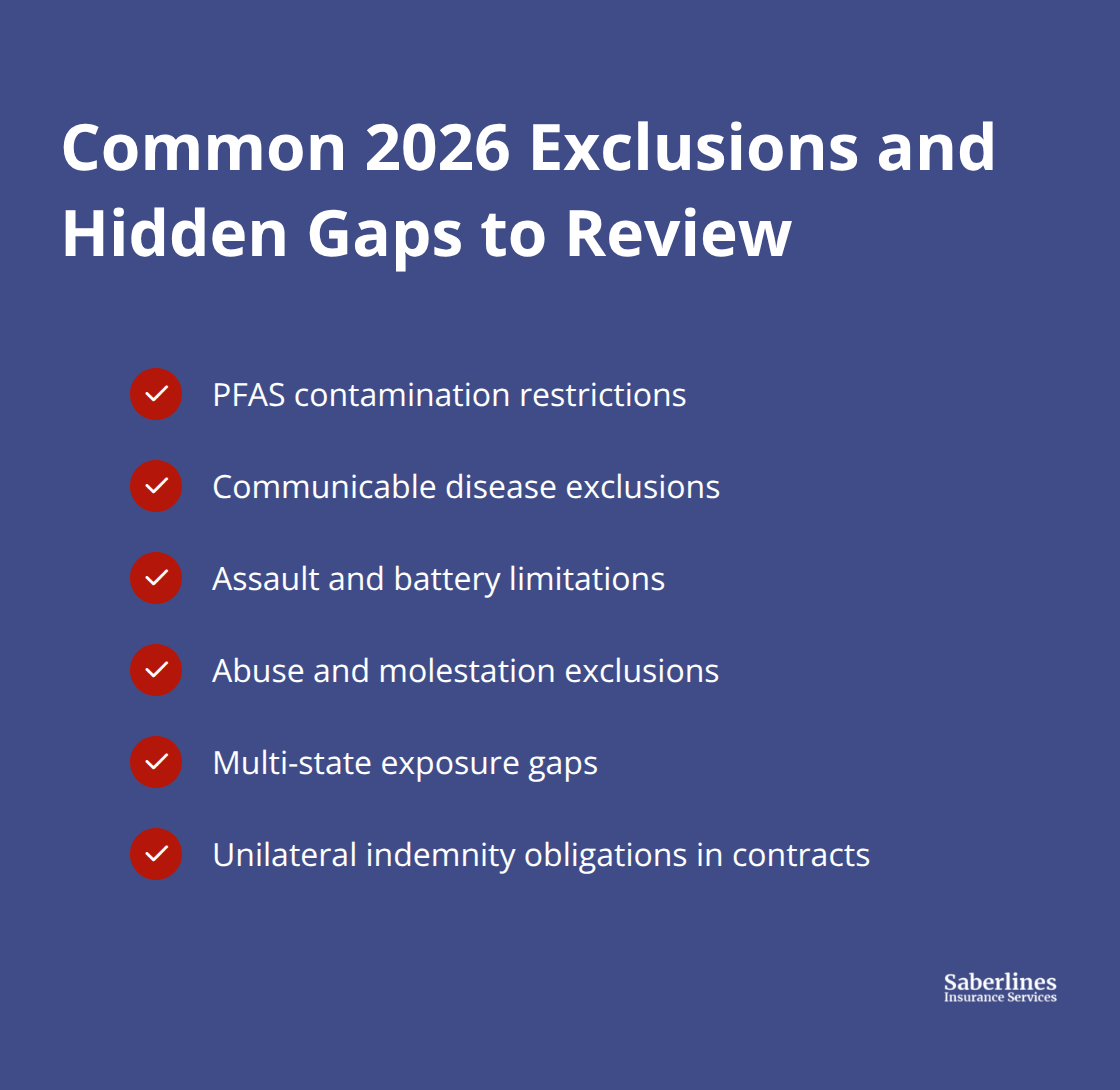

Carriers now actively exclude or heavily restrict coverage for communicable disease, PFAS contamination, assault and battery, and abuse and molestation claims. If your business hasn’t reviewed its policy exclusions since 2024, you’re almost certainly missing what your coverage actually protects. Coverage terms shift faster than most business owners realize, and a Certificate of Insurance alone won’t catch these gaps. Your existing policy may have looked adequate last year but now leaves you exposed to specific liability scenarios your industry faces today.

Limits Are Rising Because Risk Is Rising

The old $1 million general liability limit isn’t cutting it anymore. Project values have inflated, and juries award larger settlements than they did even two years ago. The NSPE, AIA, and ACEC Consolidated Risk Management Survey from 2025 found that high-severity losses occur increasingly often, especially in multi-party disputes and large infrastructure projects. Many businesses now carry $2 million to $5 million in limits, and some industries push higher. If you renew at your current limit without reassessing what a single claim could cost in your industry, you bet your business on outdated assumptions. Excess liability capacity remains constrained, with many carriers limiting participation above $5 million in excess limits, so you’ll find higher umbrella coverage tougher and more expensive than it was twelve months ago.

Compliance and Documentation Now Matter More

Underwriters no longer accept a handshake and a policy number. They want evidence that you actually manage risk. Written safety policies, training logs, inspection records, and incident reports now directly influence your renewal rates and terms. Well-documented loss control measures lead to better pricing, while poor documentation signals negligence to underwriters. If your business operates across multiple states, you need confirmation that remote work and multi-state exposure are explicitly covered. Contract review has also become critical. Many carriers tighten language around indemnity obligations and scope creep, and some now offer contract review services to help you avoid unilateral indemnities that could expose you beyond your policy limits. The shift is clear: carriers price based on your actual risk management practices, not just your industry classification.

What Happens Next in Your Renewal Process

The tightening of coverage terms and rising limits mean your next renewal conversation will look different from previous years. Underwriters will ask more questions about your operations, your loss history, and your risk controls. They’ll scrutinize your contracts and your documentation practices. This shift creates an opportunity for businesses that prepare early and demonstrate strong risk management. Those that don’t will face higher premiums, tighter restrictions, and potential coverage gaps that could prove costly.

Why These Changes Matter Right Now

Higher renewal rates directly shrink your operating budget. The Ivans Index tracked general liability renewals at 7.01% in February 2026, meaning businesses renewing that month saw premium increases compared to January. Year-over-year, the trend worsens. If you manage multiple projects as a contractor or operate a service business with client-facing work, a 7% increase compounds across your entire insurance portfolio. That money disappears from cash flow before you make a single operational decision. But the cost impact extends beyond the premium itself. Underwriters now demand documented safety programs and loss control measures, which means you spend time and resources building compliance infrastructure. Businesses that skip this step face either rejection at renewal or acceptance at punitive rates. The hidden cost isn’t just the higher premium-it’s the operational expense of proving you actually manage risk. Additionally, if your current limits sit at $1 million and you operate in an industry where claims routinely exceed that threshold, a single lawsuit could bankrupt you. The NSPE, AIA, and ACEC Consolidated Risk Management Survey from 2025 documented high-severity losses in infrastructure, transportation, and multi-use residential projects, with settlements regularly exceeding what most small businesses carry. You pay not just for more coverage but for inadequate protection if you haven’t increased your limits since 2024.

Exclusions Create Hidden Exposure

Exclusions matter more in 2026 than they did two years ago because carriers aggressively carve out specific exposures. PFAS contamination, communicable disease, assault and battery, and abuse and molestation claims now face heavy restrictions or outright exclusions on standard policies. If your business hasn’t reviewed its policy language since 2024, you likely believe you’re covered for scenarios that your actual policy explicitly excludes. This false sense of security evaporates the moment you file a claim.

For businesses operating across state lines or managing remote workers, multi-state exposure gaps create another hidden liability. Your policy may cover operations in California but leave you exposed in Nevada or Arizona if you haven’t explicitly requested multi-state endorsements. Contract-heavy businesses face even greater risk. If your client contracts include indemnity language that obligates you to cover their negligence, your general liability policy may not respond, leaving you personally liable for amounts far exceeding your policy limits. Many carriers now offer contract review services specifically to catch these misalignments before they become claims. Skipping this step isn’t just risky-it proves expensive when you discover mid-claim that your coverage doesn’t apply.

Documentation Drives Better Renewal Terms

Carriers now price based on what you can prove, not assumptions about your industry. Written safety policies, training logs, inspection records, and incident reports directly influence your renewal rates. A business that maintains detailed documentation of its risk management practices signals to underwriters that it takes loss prevention seriously, which translates to better renewal terms and potentially lower premiums. Poor documentation signals negligence, and underwriters price accordingly. This shift creates a competitive advantage for businesses willing to invest in compliance infrastructure. If you bid against competitors for contracts, many clients now require proof of strong general liability coverage with specific limits and endorsements. Landlords and corporate partners increasingly request Certificates of Insurance that demonstrate not just the existence of coverage but its adequacy relative to the work performed. A business with documented risk management practices and appropriate limits wins contracts that competitors without those practices cannot secure. The 2026 market actively rewards well-managed risks with better pricing and capacity, while poorly documented risks face restrictions and higher costs. This isn’t theoretical-actual renewal outcomes across thousands of agencies and carriers tracked by the Ivans Index reflect this reality.

What Your Next Renewal Conversation Will Look Like

Underwriters will ask more questions about your operations, your loss history, and your risk controls than they did in previous years. They’ll scrutinize your contracts and your documentation practices. This tightening of coverage terms and rising limits means your renewal process will look fundamentally different. Underwriters will want to see evidence that you’ve addressed emerging exposures specific to your industry and that your limits align with current project values and settlement trends. They’ll also verify that your multi-state operations (if applicable) are explicitly covered and that your contracts don’t obligate you to indemnify clients for their own negligence. Businesses that prepare early and demonstrate strong risk management practices will find themselves in a stronger negotiating position. Those that arrive at renewal unprepared will face higher premiums, tighter restrictions, and potential coverage gaps that could prove costly when a claim occurs.

Audit Your Current Coverage and Identify Gaps

Read Your Policy Word-for-Word

Pull your declarations page and your policy document itself, not just the summary. Read the exclusions section word-for-word, because that’s where carriers hide their refusals to pay. If your business operates in multiple states, verify that each state appears explicitly on your endorsements. If you work with contracts, print three recent ones and cross-reference the indemnity language against your policy’s scope. Many business owners discover mid-claim that they promised clients coverage their policy doesn’t provide.

The NSPE, AIA, and ACEC Consolidated Risk Management Survey from 2025 found that high-severity losses now take 18 months to 3–5 years to resolve, which means a coverage gap discovered during a claim investigation can paralyze your business for years. Schedule two hours this week to complete this audit yourself, then schedule a follow-up call with an insurance professional who can identify gaps you missed.

Document Your Findings

Carriers now offer contract review services as part of renewal discussions, so ask your agent whether this service is included in your renewal quote. Document everything you find during this audit in a simple spreadsheet: policy limits by line, exclusions that concern you, any multi-state gaps, and questions about contract language. This documentation becomes your roadmap for the renewal conversation and proves to underwriters that you take risk management seriously.

Work with an Independent Agent to Update Your Policies

Contact an independent insurance agent to update your policies based on what the audit revealed. Independent agents shop across multiple carriers rather than locking you into one company’s appetite and pricing, which matters because excess liability capacity remains constrained with many carriers limiting participation above $5 million in excess limits. An agent can identify which carriers actively compete for your industry class and which ones have tightened their underwriting criteria.

Discuss your audit findings directly with the agent. Tell them about your multi-state operations, your contract obligations, and any emerging exposures specific to your business. If you’ve added new products or services since your last renewal, mention them now because carriers price based on your actual exposures. Request quotes from at least two carriers so you can compare not just premium but also policy language, limits, and available endorsements.

Leverage Documentation to Negotiate Better Terms

The Ivans Index showed general liability renewal rates at 7.01% in February 2026, but your individual renewal depends on your loss history, documentation practices, and risk management infrastructure. A business with detailed safety policies and training records often renews at lower rates than an identical business without documentation, even in the same industry.

Ask your agent specifically about what documentation carriers want to see and what endorsements address the emerging exposures your audit flagged. Then build that documentation infrastructure before your renewal date arrives. Written safety policies, training logs, inspection records, and incident reports aren’t just compliance theater-they directly influence your renewal rates and your ability to negotiate better terms with carriers. Carriers now price based on what you can prove, not assumptions about your industry, so the documentation you create today becomes your competitive advantage at renewal.

Final Thoughts

General liability requirements 2026 have shifted the entire renewal landscape, and waiting until your policy expires leaves you scrambling to catch up. Carriers now price based on documented risk management practices, higher claim severity, and emerging exposures that standard policies increasingly exclude. The businesses that audit their coverage now and build documentation infrastructure before renewal arrives will negotiate better terms and secure capacity more readily. Those that delay will face higher premiums, tighter restrictions, and discover mid-claim that their coverage doesn’t apply to scenarios they thought were protected.

Your immediate action is to pull your policy documents and read the exclusions section word-for-word, then document any multi-state gaps, contract language concerns, and emerging exposures specific to your industry. Contact an independent insurance agent who can shop across multiple carriers and identify which ones actively compete for your business class. Request contract review services if available, and ask specifically what documentation carriers want to see before renewal so you can build that infrastructure now rather than scramble later.

We at Saberlines Insurance Services help transportation businesses navigate these exact challenges and secure coverage that protects your operations while keeping costs manageable. Contact us to discuss how your current coverage aligns with 2026 requirements and what changes will strengthen your protection.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.