Contractor Liability Coverage: Building a Solid Liability Shield

Contractor liability coverage is one of the most misunderstood aspects of running a construction business. Most contractors think they’re protected until they face a claim that falls outside their policy limits or hits an unexpected exclusion.

At Saberlines Insurance Services, we’ve seen too many contractors scramble to find coverage after damage occurs. The right liability shield isn’t about buying the cheapest policy-it’s about understanding exactly what you’re covered for and where the gaps are.

What Your Liability Coverage Actually Protects

Contractor liability insurance protects you from third-party claims-claims filed by someone other than you or your employees. When a property owner sues because your crew damaged their building during a renovation, or a passerby files a claim after an injury on your job site, your general liability policy steps in to cover legal defense costs and any settlements or judgments up to your policy limits. This protection extends to bodily injury claims, such as when someone breaks a leg from a fall at your site, and property damage claims, like when your equipment punctures a water line. The policy covers medical payments for injured third parties, defense attorney fees, court costs, and settlements, which means you avoid paying these expenses out of pocket while litigation unfolds.

Most contractors buy limits of $1 million to $2 million in general liability coverage, though smaller subcontractors often purchase only the minimum. The problem is that as construction costs rise due to inflation, medical expenses, and legal fees climbing faster than ever, those minimum limits leave you exposed to catastrophic losses on a single major claim.

Defense Costs Require Separate Coverage Verification

Your policy covers legal defense costs separately from the settlement amount in most cases. If you face a $500,000 lawsuit and your attorney charges $50,000 in fees, that defense cost typically doesn’t reduce your policy limit. However, some policies structure defense costs differently, so you must verify this in your actual policy language. Without liability coverage, you write checks to lawyers before you know whether you’ll win or lose the case.

A roofing contractor faced a bodily injury claim when a worker from another trade was struck by falling materials on a mixed-crew project. The defense alone cost $35,000, and without coverage, that contractor would have paid the entire amount upfront. The settlement eventually reached $180,000, well within the policy limit but devastating if uninsured.

Subcontractor Negligence Exposes You to Claims You Don’t Control

Your liability extends to work performed by your subcontractors under most general liability policies. If a subcontractor’s negligence causes property damage or injures someone, you face the claim even though you didn’t perform the faulty work. Many contractors believe their subs’ insurance protects them, but that’s incomplete. You remain responsible as the general contractor or project lead, and your policy is often the first one defending the claim.

This is why you must require and verify certificates of insurance from every subcontractor before they start work. A painter’s crew damaged drywall in an occupied office building during a renovation, creating water damage that spread to adjacent spaces. The painting sub’s insurance had lapsed, so the general contractor’s liability policy covered the entire $120,000 claim, exhausting part of the annual limit. That’s exposure you can’t afford to ignore when you bid future projects.

Where Coverage Gaps Hide in Your Policy

Most contractors assume their general liability policy covers all property damage and bodily injury claims, but standard policies exclude damage to your own work, property you own or rent, and certain types of professional services. These exclusions (particularly exclusions j, k, and l in ISO standard forms) create blind spots that catch contractors off guard. Exclusion j(5) bars coverage for damage to the specific part of real property on which you perform operations, while exclusion j(6) excludes damage from faulty workmanship by you or your subcontractors. Exclusion k eliminates coverage for damage to your own product, and exclusion l bars coverage for damage to your completed work.

Understanding these gaps matters because they determine whether your policy pays or you do. If your crew installs a window incorrectly and water leaks into the building’s interior, that faulty workmanship exclusion may block coverage. You need to know this before a claim arrives, not after. The right coverage strategy involves either accepting these exclusions and budgeting for them or purchasing endorsements that modify or remove them for specific projects. Your next step is to assess which gaps matter most for your business type and project mix, then align your coverage limits and endorsements accordingly.

Where Your Coverage Actually Fails

Most contractors discover their coverage gaps only after a claim lands on their desk. The standard general liability policy you bought covers third-party bodily injury and property damage, but it explicitly excludes damage to your own work, property in your care or custody, and defects caused by faulty workmanship. This matters because these exclusions directly affect how you pay when things go wrong. If your crew installs flooring incorrectly and it buckles within six months, that faulty workmanship exclusion (j(6) in ISO standard forms) blocks coverage. You absorb the cost to replace it. Similarly, exclusion j(5) eliminates coverage for damage to the specific part of real property where you perform work, meaning if your crew damages the foundation they reinforce, your policy won’t pay to fix it. These aren’t edge cases-they’re standard exclusions that apply to everyday construction work.

High-Risk Projects Demand Higher Limits Than You Expect

High-risk projects amplify these gaps significantly. Office-to-residential conversions, which have surged due to remote work trends, carry elevated defect risk when multiple owners occupy the same building. Insurers price these projects with higher premiums precisely because the risk profile is more complex than single-owner rental properties. Data center and semiconductor construction, which is expanding rapidly due to AI infrastructure investment, requires much higher liability limits than typical building work because cooling systems can leak onto high-value electronics, creating catastrophic completed operations exposure. Many contractors bid these projects with standard $1 million to $2 million limits, only to realize mid-project that clients contractually require $5 million or higher. Adjusting limits late in the process costs significantly more or may become impossible to obtain.

Subcontractor Coverage Creates Exposure You Can’t Control

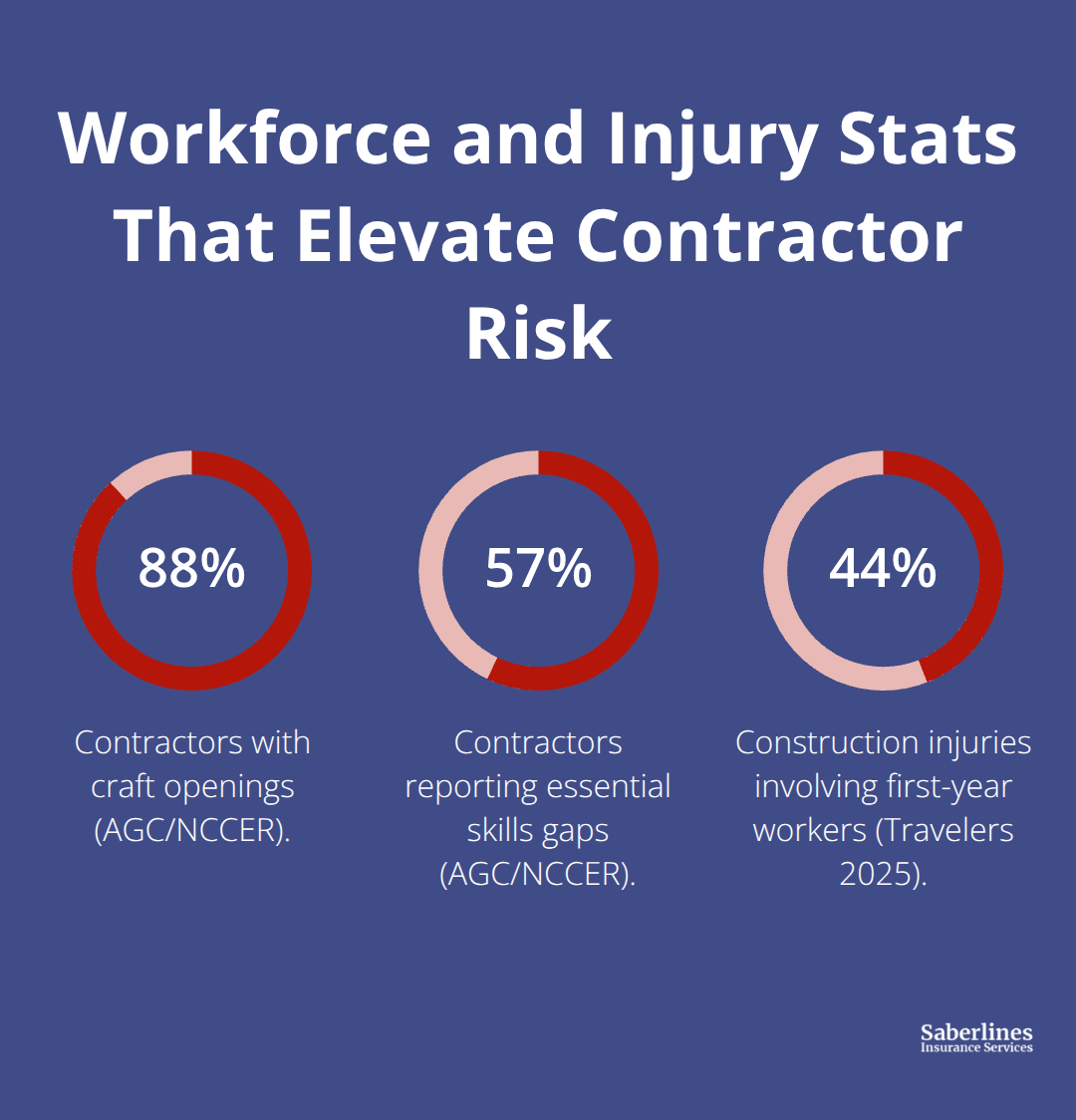

Subcontractor coverage exposes another critical gap. Your policy covers negligence by your subs, but it doesn’t cover their work if their insurance lapses or is inadequate. You must require certificates of insurance from every subcontractor and verify they maintain coverage throughout the project. A single sub with expired coverage can leave you defending claims that should be their responsibility. According to data from the Associated General Contractors of America and NCCER, 88% of contractors have craft openings and 57% report essential skills gaps, meaning new hires and less experienced subcontractors are common. Travelers’ 2025 study found that 44% of construction injuries involve first-year workers and these injuries drive 47% of workers’ compensation costs.

This workforce reality increases your exposure to subcontractor-related claims because less experienced crews create more incidents. Your liability policy doesn’t protect you from their inexperience-it just makes you defend their mistakes.

What You Must Do Before the Next Project Starts

Assess project risk upfront and verify subcontractor insurance in writing before work begins. Purchase endorsements that modify exclusions j(5), j(6), or l when your project risk profile demands it. Don’t assume your current limits are adequate for new project types or that your subs’ insurance covers you. The gaps in your standard policy will shape how much you pay out of pocket on your next major claim, so identifying them now determines whether you protect your business or expose it to catastrophic loss.

What Liability Limits Actually Protect Your Business

Most contractors pick liability limits based on what their competitors carry or what sounds reasonable, not on what their actual exposure demands. Contractors repeatedly choose $1 million to $2 million limits because those numbers feel standard, only to discover during a claim that their project risk profile required significantly more. The truth is that your liability limit must match three concrete factors: the contractual requirements your clients impose, the specific risks your project type creates, and the financial exposure you’re willing to absorb personally. Standard limits no longer reflect current construction costs. Medical expenses, legal fees, and settlements have climbed faster than inflation over the past five years, meaning a $1 million limit that felt adequate in 2020 now covers far less ground.

Match Your Limits to Project Type and Client Demands

Data center and semiconductor projects, which are expanding rapidly due to AI infrastructure investment, routinely require $5 million to $10 million limits because a single cooling system failure can damage millions in electronics. Office-to-residential conversions, driven by remote work trends, demand higher limits when multiple unit owners occupy the building because defect claims involve more complex liability chains. If you bid these projects with minimum limits, you’ll either lose the contract or accept contractual liability that exceeds your policy protection, leaving you personally responsible for the gap.

Your first step is to pull your last five project contracts and note the liability limits each client required. Most commercial clients demand $1 million to $2 million, but larger property owners and institutional clients frequently require $2 million to $5 million or more. If you’ve been bidding projects below these thresholds, your actual exposure is already higher than your current limits provide.

Calculate Limits Based on Revenue and Assets

Your revenue and asset base determine how much out-of-pocket exposure you can afford. A contractor with $2 million in annual revenue and $500,000 in equipment and tools cannot absorb a $500,000 uninsured loss without threatening business continuity. According to the American Institute of Architects, nonresidential construction spending growth has moderated, meaning tighter margins make uninsured losses more damaging. If you carry $1 million limits and face a $1.5 million claim, you personally pay the $500,000 difference plus any costs your insurance doesn’t cover due to exclusions.

This is why subcontractor verification matters so directly to your limit strategy: a single sub with lapsed insurance can push a claim above your limit, forcing you to pay their negligence out of pocket. Require and verify certificates of insurance from every subcontractor at least 30 days before work starts, and make their insurance requirements a contract line item. Higher limits cost more in premium, but the cost is predictable and manageable. An uninsured loss is catastrophic and unpredictable.

Set Limits That Protect Your Business Continuity

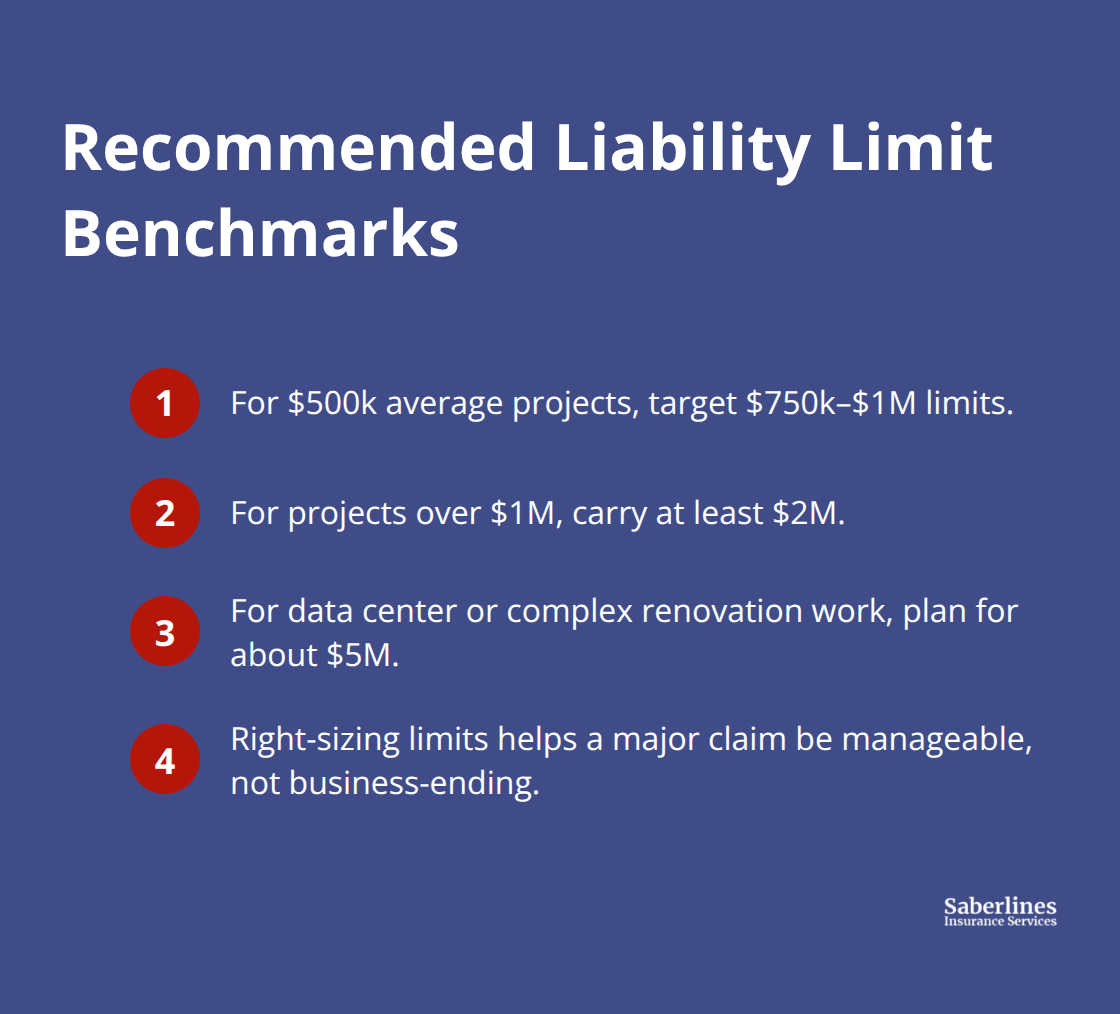

For most contractors, limits should align with your largest single project value plus 25 to 50 percent additional cushion. If your average project is $500,000, your limit should be at least $750,000 to $1 million. If you routinely bid projects over $1 million, your limit should be $2 million minimum, and if you pursue data center or complex renovation work, $5 million is increasingly standard.

The gap between what you carry and what you actually need determines whether a single major claim ends your business or simply costs you a deductible.

Final Thoughts

Contractor liability coverage protects your business only when it matches three concrete realities: what your clients contractually require, what your project type actually demands, and what you can afford to absorb personally if a claim exceeds your limits. The contractors who avoid catastrophic losses pull their contracts, verify subcontractor insurance in writing, and adjust their limits before bidding high-risk projects like data center work or office-to-residential conversions. They don’t assume their coverage is adequate or buy the cheapest policy available.

Your next step is straightforward: review your last five project contracts and list every liability limit your clients required, then compare those numbers to your current policy limits. Pull your actual policy language and identify which exclusions matter most for your business type, particularly exclusions j(5), j(6), and l that block coverage for faulty workmanship and damage to your own work. Assess whether you need endorsements to modify those exclusions or whether accepting them and budgeting for self-insured repairs makes financial sense.

Work with specialists who understand construction risk and can help you build adequate protection before your next major claim arrives. General insurance agents often miss the nuances of contractor liability because they don’t focus on your industry, but Saberlines Insurance Services specializes in helping contractors secure the right coverage for their specific risk profile. Contact us to discuss your liability strategy with someone who understands construction exposure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.