Transportation General Liability Insurance: Coverage That Keeps You Moving

One accident, one lawsuit, one claim-and your transportation business could face financial devastation without proper protection. Transportation general liability insurance is the safety net that protects your operation from bodily injuries, property damage, and legal costs that can drain your resources.

At Saberlines Insurance Services, we’ve seen too many transporters operate with gaps in their coverage, only to discover those gaps when it’s too late. This guide walks you through what you actually need to protect your business.

What General Liability Actually Covers in Transportation

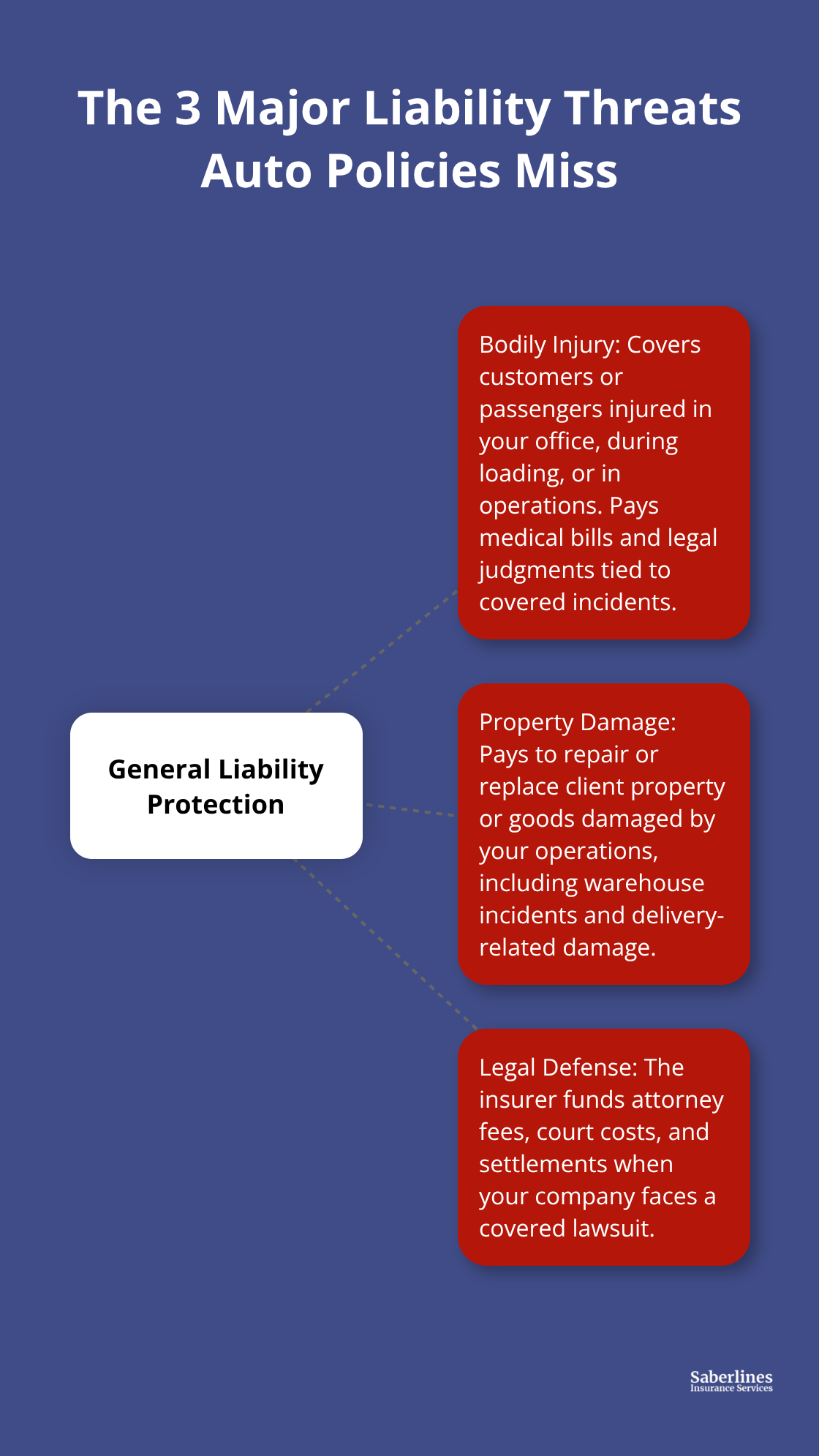

The Three Major Financial Threats Your Auto Policy Won’t Touch

General liability insurance protects your transportation business from three major financial threats that auto policies won’t cover. First, bodily injury claims happen constantly in transportation operations-a customer slips in your dispatch office, a delivery goes wrong and someone gets hurt, or a passenger sustains an injury during loading. Medical expenses for these incidents add up fast; a single slip-and-fall claim can easily exceed $50,000 when you factor in hospital visits, ongoing treatment, and lost wages. General liability covers these medical costs plus legal judgments if someone sues. Second, property damage liability protects you when your operations damage someone else’s belongings. A forklift operator damages client goods in your warehouse, a delivery causes damage to a customer’s property, or shelving collapses and destroys inventory-general liability covers repair or replacement costs. Without this coverage, you’re writing checks directly from your business account.

Third, legal defense costs get paid by your insurer, not your pocket. When someone files a lawsuit against your company, the insurance company covers attorney fees, court costs, and settlement negotiations.

Affordability Meets Essential Protection

According to Insureon data, general liability for trucking averages just $51 per month with typical limits of $1 million per occurrence and $2 million aggregate, making this one of the most affordable layers of protection you can buy. This low cost relative to the exposure makes general liability a non-negotiable foundation for any transportation operation.

Why Your Auto Policy Leaves You Exposed

The critical distinction is that general liability covers non-vehicular incidents while commercial auto covers vehicle-related accidents. If a driver backs a truck into a loading dock, that’s auto liability. If someone sustains an injury during the loading process itself or damaged goods surface after delivery, that’s general liability. Many transporters mistakenly assume their auto policy handles everything, then face massive out-of-pocket costs when a warehouse incident or completed operations claim emerges.

Your general liability policy should explicitly include coverage for products and completed operations-protection that activates after goods leave your facility. This matters because delivery errors, damaged shipments discovered later, and customer injuries during unloading on their property all fall under completed operations, not auto coverage. Transporters often scramble to add this coverage retroactively, paying higher premiums because the exposure wasn’t covered from day one. The solution is straightforward: review your policy now to confirm it includes bodily injury, property damage, personal and advertising injury, and medical expense coverage with adequate limits that match your actual operation size.

Understanding what general liability covers sets the foundation, but identifying the specific gaps in your current protection is where most transporters stumble-and that’s exactly where the next section takes you.

Where General Liability Falls Short

Most transporters discover coverage gaps only after an incident exposes them. The problem isn’t what general liability covers-it’s what transporters assume it covers without verifying their actual policy language. A delivery driver injures a passenger during loading, and the business owner files a claim only to learn that passenger injury during the loading process wasn’t included in their policy limits or was excluded entirely. A warehouse worker damages client goods worth $150,000, but the policy limit sits at $100,000 per occurrence, leaving a $50,000 gap the business must absorb. These scenarios happen regularly, and they’re entirely preventable with the right policy structure and limits matched to your operation size.

Passenger and Customer Injury Exposures Often Get Missed

Transportation operations involving passengers create exposure that standard general liability policies sometimes exclude or severely limit. Non-emergency medical transport providers face particular risk-a patient falls during boarding, or a passenger sustains injury from improper securing or vehicle movement. Charter bus operators, limousine services, and school bus contractors all operate in this high-injury zone. The gap emerges because some carriers treat passenger injury differently from third-party bodily injury, imposing lower limits or requiring separate endorsements. You need to confirm your policy explicitly covers passenger injuries during boarding, transport, and disembarking with limits that reflect the severity of potential claims. A single serious injury can generate $200,000 to $500,000 in medical costs and liability exposure-far exceeding the $1 million standard limit if multiple passengers are injured in a single incident. Ask your agent whether your policy includes medical payments coverage for passengers separate from your general liability bodily injury limit, and whether passenger injury during loading and unloading is covered without exclusion.

Completed Operations and Third-Party Property Damage Create Real Exposure

Damage to customer property or goods in your care represents a significant liability gap for many transporters. A forklift operator in your warehouse damages expensive client inventory, a delivery causes structural damage to a customer’s property, or goods arrive damaged and the customer sues for the full replacement value. General liability covers these scenarios, but only if your policy explicitly includes products and completed operations coverage with adequate property damage limits. Transporters frequently operate with $100,000 property damage limits when their actual exposure-based on cargo value, number of daily deliveries, or warehouse inventory-demands $500,000 or higher. The Motor Transport Association of Connecticut research on general versus auto liability emphasizes that non-vehicular incidents including delivery errors and damaged goods represent major cost drivers. Review your contracts with major clients; many require minimum property damage limits of $500,000 or $1,000,000 as a condition of doing business. Without those limits documented in your policy, you cannot provide accurate certificates of insurance, and clients may terminate relationships or hold you liable for shortfalls.

Calculate Your Actual Exposure Before Selecting Limits

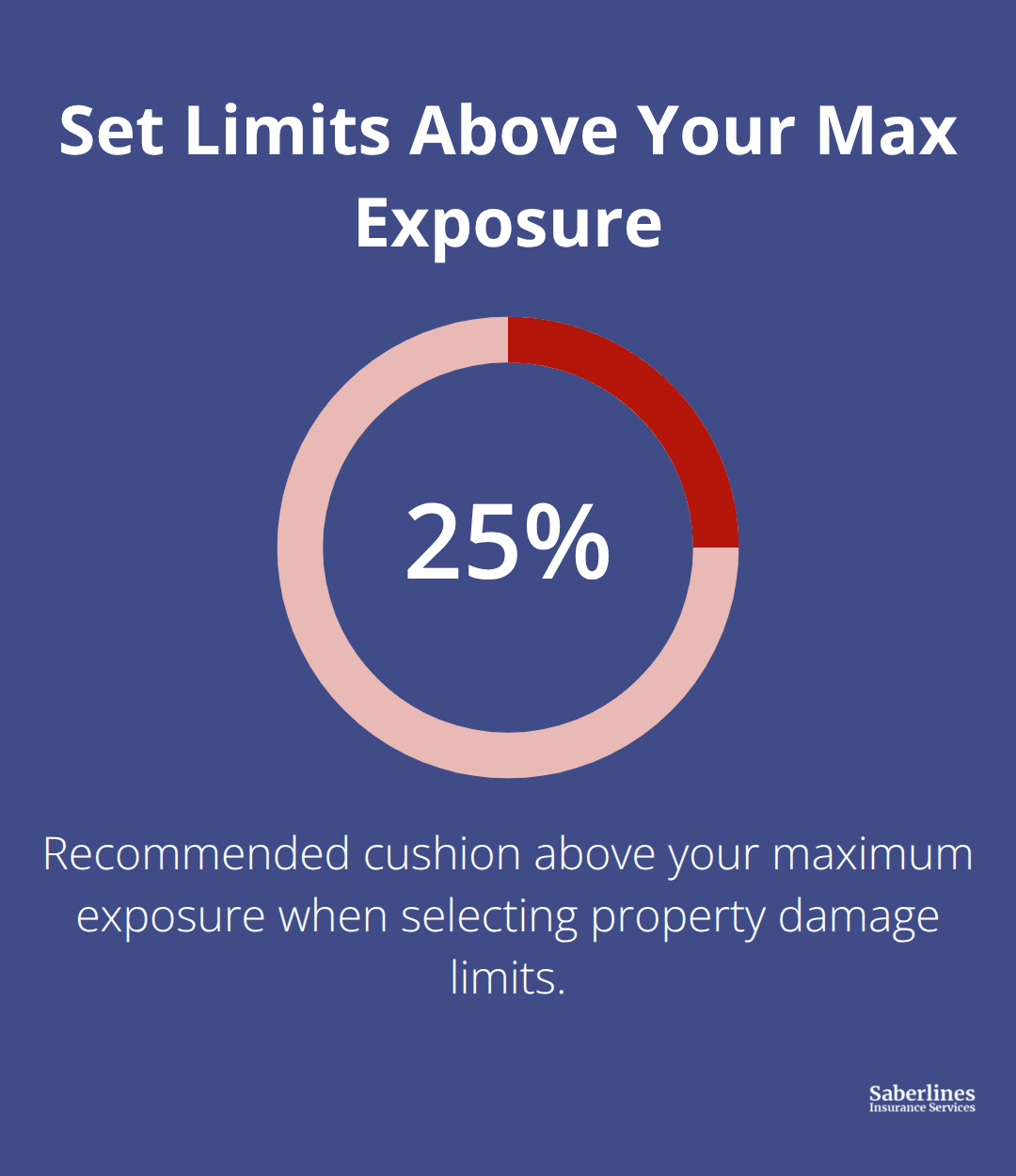

You need to calculate your actual third-party property damage exposure to set appropriate limits. Review your largest single shipment value, your total warehouse inventory at any given time, and your most valuable client contracts, then set your policy limits to exceed that number by at least 25 percent. This calculation prevents the common mistake of selecting limits based on industry averages rather than your specific operation.

A transportation company hauling high-value electronics faces vastly different exposure than one transporting household goods, yet both might carry identical $100,000 property damage limits. Your contracts with major clients often dictate minimum coverage requirements-many demand $500,000 or $1,000,000 in property damage limits as a condition of partnership. Failing to meet these contractual requirements leaves you unable to provide accurate certificates of insurance and exposes you to client disputes or contract termination. The next section shows you how to assess your specific risk exposures and select the right policy structure for your transportation business.

Selecting the Right Coverage Limits for Your Operation

Start with Your Client Contracts, Not Industry Averages

Pull every client agreement you have and identify the minimum general liability requirements they demand. Most major clients require $500,000 or $1,000,000 in property damage limits as a condition of partnership, yet many transporters carry $100,000 limits based on what they assume is standard. That mismatch disqualifies you from bidding on larger accounts and creates certificate of insurance problems when clients verify your actual coverage.

Calculate Your Real Exposure

List your largest single shipment value, total warehouse inventory at any given time, and the highest-value goods you handle monthly. If you transport electronics worth $750,000 in a single load, your property damage limit should exceed that number. Set your limits 25 percent above your maximum exposure, not at your maximum exposure, because a single incident can generate unexpected secondary costs.

According to Insureon data, general liability averages $51 per month for trucking operations with $1 million per occurrence and $2 million aggregate limits. Jumping from $1 million to $2 million in property damage limits typically adds minimal cost-often just $10 to $20 monthly-making the upgrade financially sensible when your actual exposure justifies it.

Choose Your Deductible Strategically

Your deductible choice matters equally to your coverage limits. A $500 deductible costs less than a $1,000 deductible, but only select the lower deductible if you can absorb it without straining cash flow. Transportation businesses with tight margins should select a $1,000 deductible they can comfortably pay, because a $50 monthly premium savings disappears fast when you face a claim and lack the reserves to cover the deductible.

Verify Products and Completed Operations Coverage

Ask your agent directly: does this policy cover passenger injuries during boarding and disembarking, damage to customer property while goods sit in your warehouse, and liability for delivery errors discovered after goods leave your facility? Get written confirmation of these coverage points before purchasing.

Transportation operations like charter buses, limousine services, and non-emergency medical transport face passenger injury exposure that some carriers exclude or severely limit, so passenger-related coverage must be explicit in your policy. Your policy should include products and completed operations coverage without exclusion-this protection activates after goods leave your facility and covers delivery errors, damaged shipments discovered later, and customer injuries during unloading on their property.

Work with a Transportation-Focused Agency

A specialized agency accesses carriers experienced with transportation risks, including carriers willing to underwrite hard-to-place operations, and they audit your coverage against your actual contracts and operations rather than accepting industry defaults. Request quotes from multiple carriers through a transportation-focused agency, then compare not just price but coverage structure, ensuring bodily injury, property damage, completed operations, and passenger injury coverage align with your specific business model.

Final Thoughts

Transportation general liability insurance stands between your business and financial ruin when incidents strike. Without it, you pay medical bills, property damage costs, and legal fees directly from your account. With it, your insurer absorbs those expenses while your operation continues moving forward.

The gap between what you assume your coverage includes and what your policy actually covers destroys most transporters. You might believe your auto policy handles everything, then discover that a warehouse incident, passenger injury during loading, or damaged goods claim falls outside your protection. Transportation general liability insurance fills those gaps, but only if you select limits matching your actual exposure and verify that your policy covers bodily injury, property damage, passenger injuries during boarding and disembarking, and completed operations without exclusion.

Pull your client contracts today and identify the minimum coverage limits they require-most demand $500,000 or $1,000,000 in property damage limits. Calculate your largest single shipment value and total warehouse inventory, then set your policy limits to exceed that number by at least 25 percent. Contact Saberlines Insurance Services to review your current coverage, identify gaps, and receive quotes from carriers experienced with transportation operations.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.