Truck Insurance Quotes: Fast Quotes for Commercial Vehicles

Getting truck insurance quotes is fundamentally different from shopping for personal auto coverage. Commercial vehicles face unique risks, higher coverage requirements, and stricter underwriting standards that most truck owners don’t anticipate.

At Saberlines Insurance Services, we’ve seen countless fleet operators and owner-operators leave money on the table by not understanding what goes into a proper quote. This guide walks you through the process so you can get accurate quotes fast and avoid costly mistakes.

Why Truck Insurance Costs More Than Personal Auto

Truck insurance quotes reflect a fundamentally different risk calculation than personal auto insurance. The Federal Motor Carrier Safety Administration legally requires trucking coverage because commercial vehicles operate under stricter liability standards. Most trucks need at least a $750,000 primary liability limit, compared to state minimums for personal vehicles that often sit at $15,000 to $25,000. This gap exists because a loaded semi-truck represents catastrophic damage potential. When a personal vehicle causes an accident, the financial exposure stays limited. When a commercial truck is involved, medical bills, property damage, and legal settlements multiply exponentially.

Insurance underwriters factor in cargo value, operating radius, and vehicle type when they price truck coverage. A refrigerated trailer hauling perishable goods costs more to insure than a dry van because spoilage creates additional financial exposure. Dump trucks command higher premiums than box trucks due to rollover risk. These aren’t arbitrary charges; they reflect actual claims data and loss patterns specific to each operation.

What Underwriters Actually Need From You

An accurate truck insurance quote requires you to provide details that personal auto quotes never ask about. Underwriters need your inspection history, USDOT compliance record, CSA-e percentile scores, and specific cargo types you haul. They want to know your operating radius, whether you run intrastate or interstate, and how many years you’ve been in business.

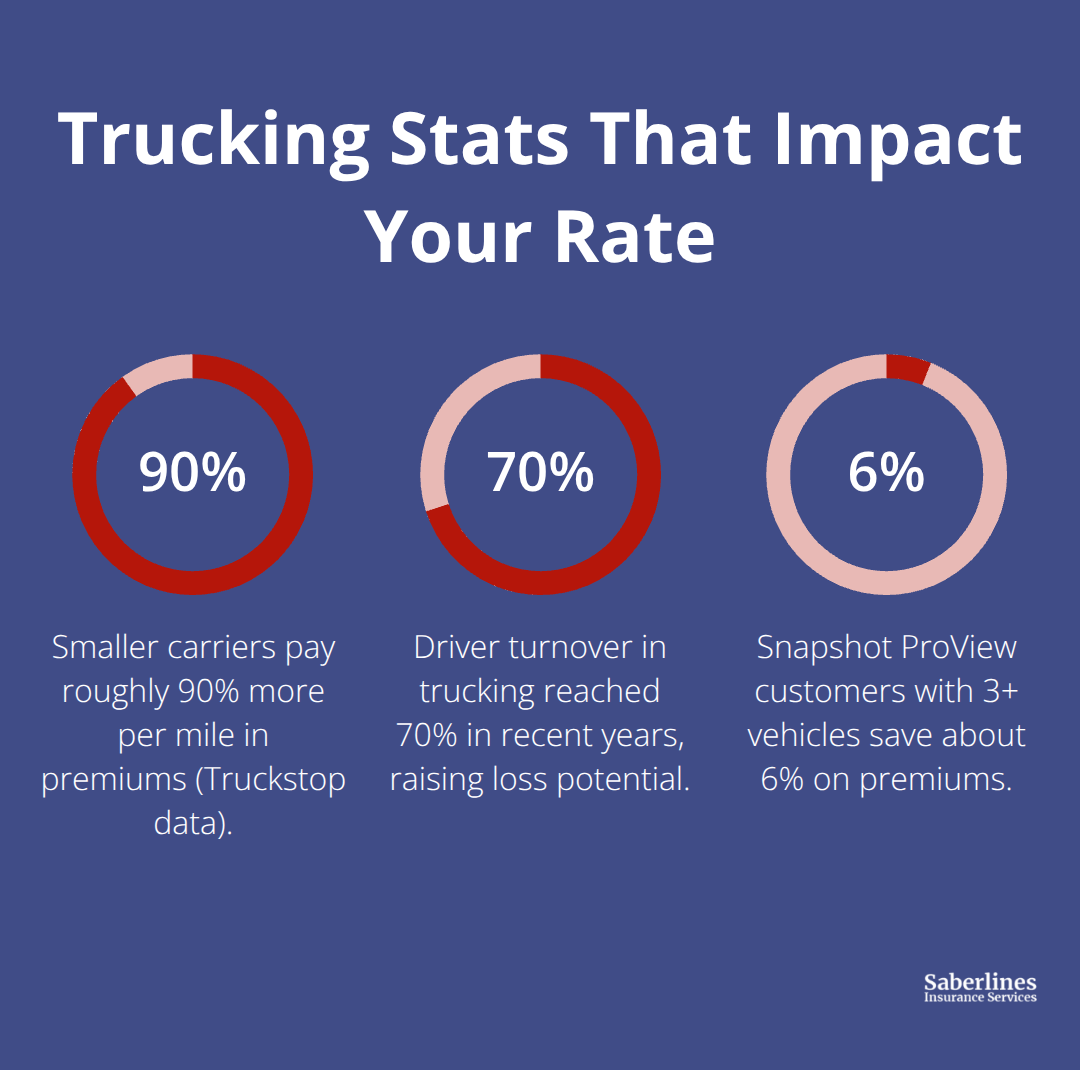

Driver turnover rates in trucking reached 70% to 90% in recent years, which directly impacts premium calculations because inexperienced drivers generate more claims. Your fleet’s age matters significantly; trucks ten years old or newer lower risk and insurance rates due to better safety and reliability. Some insurers require broker-assisted underwriting rather than online quotes because the complexity demands human review. This isn’t bureaucracy; it’s risk assessment. An insurer quoting based on incomplete information will either underprice and face losses or overprice and lose your business.

Specialized Coverages That Personal Auto Doesn’t Include

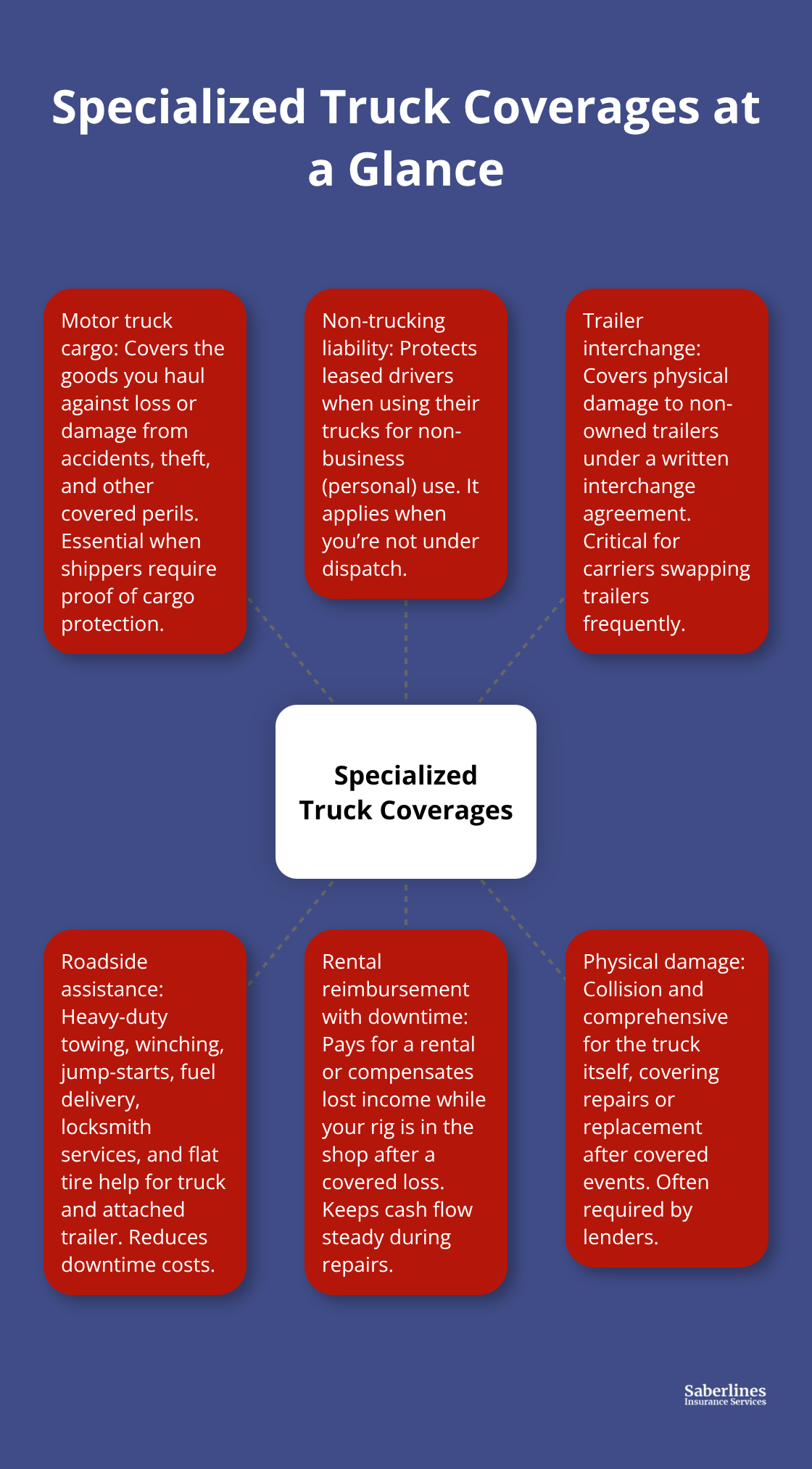

Motor truck cargo coverage protects goods you haul from loss or damage due to accidents, theft, and other risks. Non-trucking liability covers leased drivers who use their trucks for personal use when they’re not on the clock. Trailer interchange insurance protects against damages or losses to trailers you haul or interchange with others. These coverages don’t exist in personal auto policies because personal vehicles don’t create these exposures.

Heavy truck roadside assistance covers towing, winching, battery jump-start, fuel delivery, locksmith services, and flat tire replacement for the truck and attached trailer. Rental reimbursement with downtime covers vehicle rental or lost income while your rig sits in the shop, keeping cash flowing during repairs. Physical damage coverage for commercial trucks includes collision and comprehensive protection for the truck itself, covering repairs or replacement. Each coverage type addresses real operational realities that personal auto insurance ignores.

The specialized nature of truck insurance means you pay for protection tailored to how you actually work, not generic coverage that doesn’t fit commercial operations. Understanding these differences prepares you to request accurate quotes and evaluate what insurers offer. The next section walks you through the specific information you need to gather before you contact insurers for quotes.

How to Get Fast and Accurate Truck Insurance Quotes

Prepare Your Information Before You Request Quotes

Insurers need your USDOT number, current inspection history, and CSA-e percentile scores because these directly predict claims frequency. Your driving record matters, but so does your fleet’s age; trucks ten years old or newer qualify for better rates due to superior safety systems. Have your specific cargo types ready.

Hauling hazardous materials requires different underwriting than dry goods. Your operating radius determines exposure; interstate operations face federal FMCSA requirements while intrastate trucking follows state rules. Provide accurate annual mileage, number of drivers, and driver experience levels.

Insurance companies like Progressive and GEICO can issue federal and state filings within 24 to 48 hours after you apply, but only if your initial submission contains complete information. Incomplete applications get delayed, and delays cost you money during the quote-to-binding window. If you operate leased vehicles, clarify whether you or the motor carrier holds primary coverage. Most online quote tools ask for basic information and deliver preliminary pricing in eight minutes, but detailed underwriting often requires broker assistance because the complexity demands human judgment.

Compare Coverage Limits, Not Just Monthly Premiums

Two $900 monthly quotes can be wildly different if one carries $750,000 liability and the other $1 million. Request identical coverage across all quotes so you compare apples to apples. Physical damage deductibles matter tremendously; a $1,000 deductible versus $2,500 saves money monthly but costs thousands out-of-pocket when a claim occurs. Ask about discount eligibility explicitly. Progressive reported that new truck customers enrolled in their Smart Haul program save an average of $1,261 annually, while Snapshot ProView customers with three or more vehicles save approximately six percent without an ELD. These discounts don’t appear automatically; you must qualify and apply.

Verify that specialized coverages you actually need appear in each quote. Non-trucking liability, trailer interchange, and cargo protection are often add-ons, not defaults. Smaller carriers pay roughly ninety percent more per mile in premiums according to Truckstop data, which means your fleet size affects pricing significantly. Don’t assume online aggregators like CoverWallet deliver complete quotes; verify that their matches include all endorsements your operation requires.

Spot Red Flags in Quotes That Signal Trouble

Red flags include quotes that seem suspiciously cheap without explanation, insurers unwilling to clarify what’s included, or carriers that quote without requesting your inspection history. A quote missing your USDOT compliance details signals underwriting corners are being cut. If an insurer quotes without understanding your actual operations, they’ll either deny claims later or cancel your policy when claims arrive.

Operators who prepare comprehensive details before requesting quotes cut their approval timeline in half. This preparation also reveals which insurers take your operation seriously and which ones treat truck insurance as a commodity product. The next section addresses the mistakes that most truck owners make when they request quotes, mistakes that cost thousands in unnecessary premiums or inadequate coverage.

Common Mistakes Truck Owners Make When Getting Quotes

Shopping by Price Instead of Coverage

Most truck owners treat truck insurance like personal auto insurance and shop based on monthly cost alone. This approach costs thousands because a $200 monthly savings on premium often means $5,000 less in coverage limits or missing cargo protection entirely. Owner-operators frequently request quotes without mentioning their actual cargo types, operating radius, or whether they haul hazardous materials. Underwriters then quote based on assumptions, not reality.

When your operation differs from what the quote assumed, you face either surprise premium increases at renewal or denied claims because your actual exposure wasn’t covered. Smaller carriers pay roughly ninety percent more per mile in premiums according to Truckstop data, which means inadequate coverage hits your bottom line twice: first through higher claims costs, then through premium increases after claims occur. The solution is straightforward: request quotes that match your exact operation, not generic coverage. Ask each insurer to quote the same liability limits, deductibles, and specialized coverages so you compare actual protection, not just numbers on an invoice.

Requesting Quotes from Too Few Carriers

The second mistake is requesting quotes from only one or two insurers. Progressive’s position as the number one truck insurer in America according to S&P Global Market Intelligence 2024 data doesn’t mean they offer the best quote for your specific operation. GEICO, OOIDA, and The Hartford each underwrite differently and price different risk profiles competitively. A refrigerated hauler might find The Hartford’s fleet programs more suitable, while an owner-operator with a single truck may qualify for better rates through OOIDA’s in-house underwriting. You won’t know without requesting detailed quotes from at least three carriers.

Many operators assume online quote tools deliver complete pricing, but aggregators like CoverWallet match you with carriers without verifying that specialized endorsements appear in quotes. This creates a false sense of comparison. Instead, contact carriers directly and work with brokers who understand your specific operation. We specialize in trucking and passenger transportation, helping owner-operators and fleets secure coverage for commercial auto, cargo, physical damage, bobtail, workers’ compensation, general liability and BOPs. We market for preferred and hard-to-place risks because we understand that one-size-fits-all quotes leave money on the table.

Incomplete Information Leads to Inaccurate Quotes

Operators who prepare comprehensive details before requesting quotes cut their approval timeline in half. This preparation also reveals which insurers take your operation seriously and which ones treat truck insurance as a commodity product. Spending an extra hour gathering complete information about your operation (USDOT number, inspection history, CSA-e percentile scores, cargo types, and operating radius) and requesting quotes from multiple specialized carriers reduces your annual premium by five to fifteen percent on average while securing coverage that actually protects your business.

Final Thoughts

Accurate truck insurance quotes require preparation, comparison, and working with carriers who understand your specific operation. The three mistakes outlined above-shopping by price alone, requesting quotes from too few insurers, and providing incomplete information-cost operators thousands annually in wasted premiums or inadequate coverage. Avoiding these pitfalls starts with gathering your USDOT number, inspection history, CSA-e percentile scores, and cargo details before you contact any insurer.

Specialized insurers matter because they underwrite based on trucking realities, not generic assumptions. Progressive, GEICO, and The Hartford each price risk differently depending on your fleet size, cargo type, and operating radius. A carrier experienced in refrigerated hauling understands spoilage exposure, while a carrier focused on owner-operators knows how to price single-truck operations competitively.

We at Saberlines Insurance Services help owner-operators and fleets secure truck insurance quotes tailored to their specific operation. We specialize in trucking and passenger transportation, handling commercial auto, cargo, physical damage, bobtail, workers’ compensation, general liability, and BOPs for small and mid-sized transportation businesses. Contact Saberlines Insurance Services to request quotes that match your actual exposure, not generic assumptions.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.