Owner Operator Trucking Insurance: What You Need to Know

Owner-operator trucking insurance isn’t optional-it’s the foundation of a sustainable business. Without the right coverage, a single accident or claim can wipe out your profits and threaten your livelihood.

At Saberlines Insurance Services, we’ve seen too many owner-operators operate with gaps in their coverage. The good news is that understanding your insurance needs doesn’t have to be complicated.

The Three Core Coverages Your Business Cannot Operate Without

Commercial Auto Liability: Your Legal Foundation

Commercial auto liability is non-negotiable. The FMCSA requires a minimum of $750,000 in primary liability coverage for owner-operators with authority, but this number is misleading.

Most shippers and brokers demand $1,000,000, and frankly, that’s the realistic floor for securing freight. Nuclear verdicts have exploded in recent years-according to Marathon Strategies, 2024 saw 135 nuclear verdicts exceeding $10 million, totaling $31.3 billion, with the median nuclear verdict around $51 million. A single catastrophic accident without adequate limits can destroy your business. Your liability coverage protects third parties for bodily injury and property damage related to your trucking operations. This coverage keeps you legal and operational.

Physical Damage Coverage: Protecting Your Asset

Physical damage coverage protects your truck itself from collision, fire, theft, and vandalism on an actual cash value basis. If your truck is financed, your lender will require this coverage. ATRI’s 2024 data shows insurance costs about $0.102 per mile, roughly 10% of total operating costs, making this a substantial expense that demands smart management. Physical damage typically includes glass breakage and chip repair with downtime coverage included at no extra premium for some programs. Downtime coverage reimburses up to $300 per day with a maximum of $18,000 and a 14-day waiting period, which matters significantly if your truck goes down during peak season.

Cargo Insurance: Protecting Your Load

Cargo insurance rounds out your essential trio by protecting loss of goods in your care during transit. This coverage protects against theft, damage, and spoilage and allows you to tailor limits to match your typical cargo value. Motor truck cargo insurance includes debris removal, earned freight protection, and refrigeration breakdown coverage. Most owner-operators pay $400–$1,800 annually for cargo coverage, making it affordable relative to the protection it provides.

These three coverages form your minimum viable insurance program, but significant gaps exist elsewhere that can cost you thousands when claims arise.

Common Coverage Gaps Owner-Operators Face

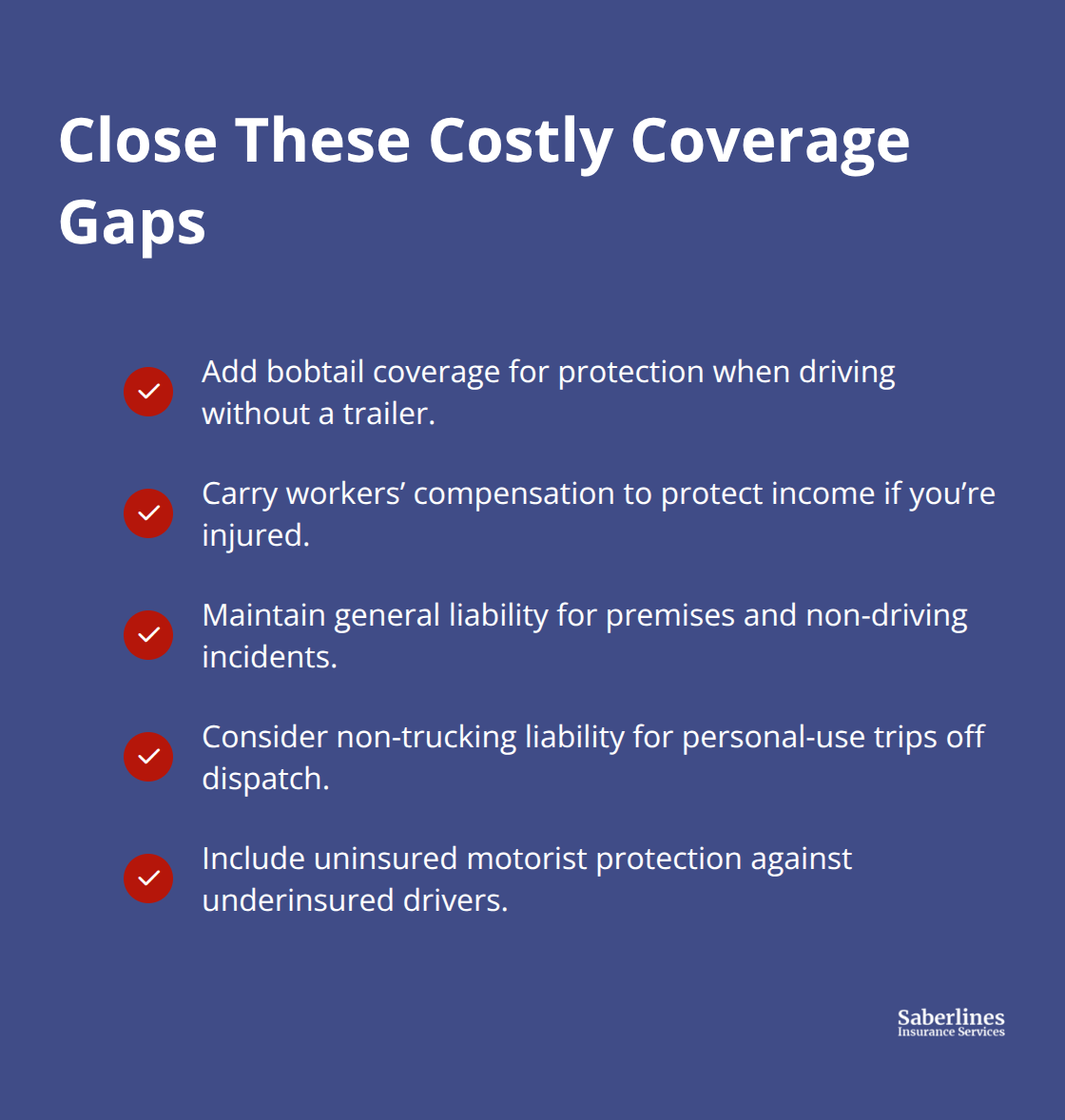

The three core coverages protect your truck and load, but they leave dangerous blind spots that cost owner-operators thousands annually. Bobtail coverage, workers’ compensation, and general liability aren’t optional add-ons-they’re essential gaps that standard policies ignore. Too many owner-operators discover these gaps only after a claim gets denied.

Bobtail Coverage: Protection When You Travel Empty

Bobtail coverage protects you when you drive empty between loads or to the mechanic. Your commercial auto liability vanishes the moment you disconnect from a trailer, leaving you legally exposed with zero protection. A single accident while deadheading can result in personal liability claims that your primary policy won’t cover. This gap costs owner-operators $350–$480 annually to fill, yet many operate without it.

Workers’ Compensation: Protecting Your Income

Workers’ compensation seems irrelevant for solo operators, but it’s not. Most states require it if you have any employees, even part-time or occasional help. More importantly, it protects you if you’re injured and cannot work-your business income doesn’t pause while you recover. Annual workers’ compensation costs run roughly $1,600–$2,200 for owner-operators, according to industry data, but skipping it exposes you to catastrophic financial risk if injury strikes.

General Liability: Coverage Beyond Your Truck

General liability addresses the incidents your auto policy ignores. Slip-and-fall claims at shipper facilities, property damage to customer premises, or injury claims from non-driving incidents fall outside commercial auto coverage entirely. A customer injured at your facility or damaged property at a loading dock creates liability exposure that general liability covers. Most owner-operators pay $500–$800 annually for general liability, yet operate without it.

Additional Gaps Worth Addressing

Non-trucking liability and uninsured motorist coverage deserve attention as well. Non-trucking liability covers you when using your truck for personal errands or when not under dispatch, typically costing $350–$480 annually. Uninsured motorist protection safeguards you against drivers without adequate coverage-increasingly critical given that uninsured driver rates remain stubbornly high nationwide. The math is straightforward: spending an extra $3,000–$4,000 annually to eliminate coverage gaps costs far less than a single claim that falls outside your existing policies.

These three gaps compound over time, and each one represents a scenario where a single claim could exceed your total annual premium savings. Identifying which gaps apply to your operation requires honest assessment of your actual business activities, not just regulatory minimums. The next step involves understanding what factors actually drive your insurance costs and how to secure competitive quotes that reflect your real risk profile.

How to Get Affordable Quotes and Choose the Right Policy

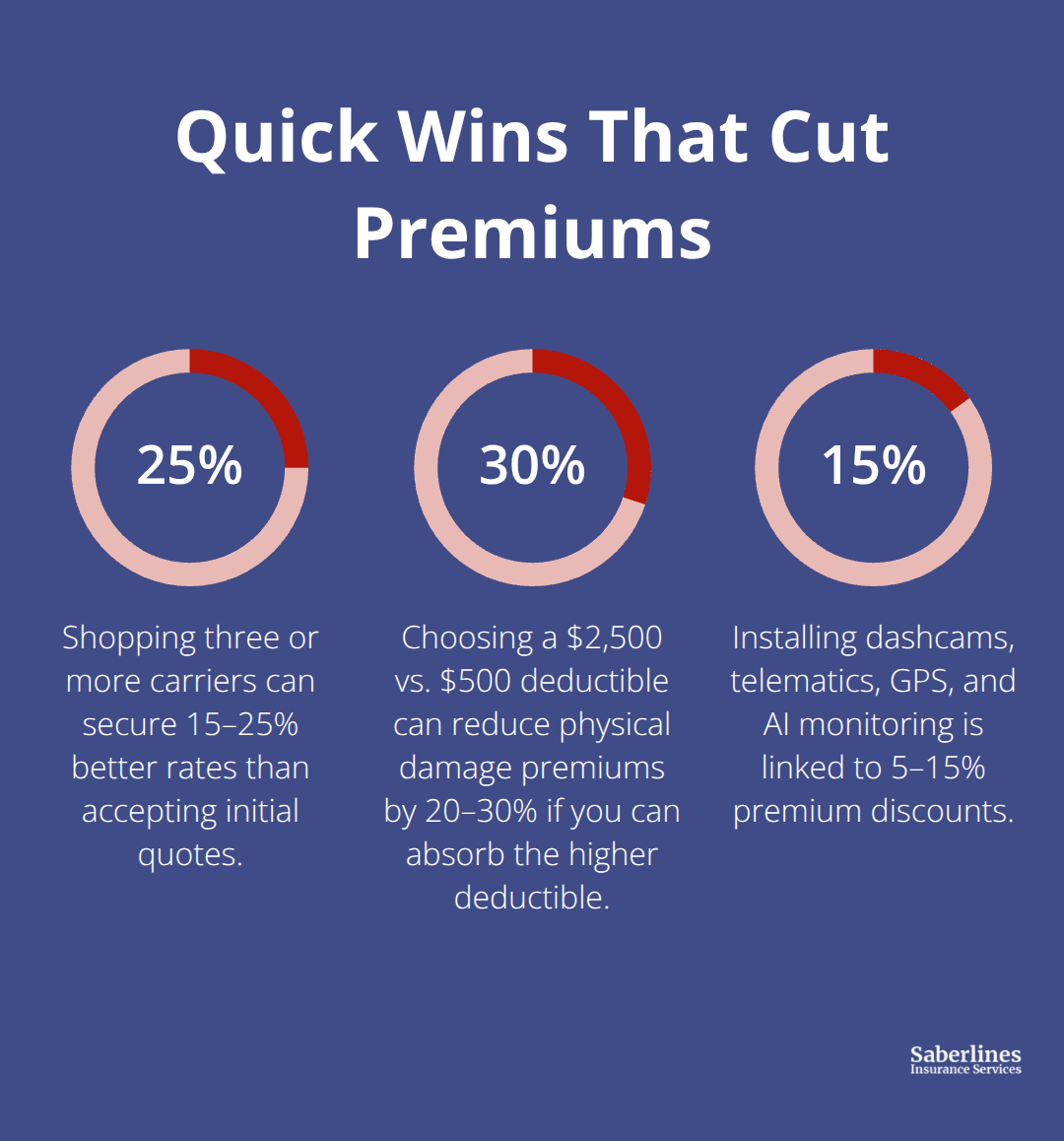

Shopping for owner-operator insurance the wrong way costs you thousands in overpayment and exposes you to coverage gaps you didn’t know existed. Most owner-operators contact one or two carriers, accept the first quote, and move on. This approach guarantees you’re overpaying. The data supports this: established independent operators typically pay $750–$1,167 monthly, while new authorities pay $1,000–$1,833 monthly, yet operators who shop three or more carriers consistently secure 15–25% better rates than those accepting initial quotes.

Start Shopping Early and Compare Multiple Carriers

Start shopping 60 days before your renewal date, not two weeks before. Early shopping gives you time to compare actual policy terms, not just premium numbers, and allows carriers time to properly underwrite your application instead of rushing through a quick quote. Request quotes from at least three carriers simultaneously so you’re comparing apples to apples on the same day. Premium fluctuations across carriers for identical coverage can swing dramatically based on their appetite for your specific risk profile.

A carrier that charges $1,200 monthly for a new authority with a clean MVR might offer the same coverage at $900 monthly next year after you build a loss-free history.

Understand What Drives Your Premium Costs

Your driving record, CSA scores, and years of CDL experience matter enormously. Operators with less than two years of experience typically face 40–100% higher premiums than established carriers, but this gap shrinks significantly after three years of clean operation. Your credit history influences pricing as well, though many operators don’t realize this connection. Vehicle size and value drive costs upward too: a newer, larger truck costs substantially more to insure than an older sprinter van, even with identical coverage limits.

The specific freight you haul dramatically reshapes your costs. Hazardous materials, refrigerated loads, oversized freight, and car-hauling classifications increase premiums substantially compared to general freight. Oil-field work requires specialized coverage and carries significantly higher rates. Your service territory matters more than most operators expect: a carrier operating exclusively in Maine averages roughly $275 monthly for $1 million liability coverage, while New York carriers average around $666 monthly for identical limits, according to MoneyGeek’s 2025 analysis. Regional operations within a limited radius typically cost less than unlimited nationwide coverage.

Optimize Your Deductibles and Safety Technology

Your deductible choices directly impact monthly costs: accepting a $2,500 deductible instead of $500 can reduce your physical damage premium by 20–30%, though this strategy only works if you can actually absorb that deductible from cash reserves. Try higher deductibles on paid-off older trucks to avoid over-insurance. Safety technology investments pay measurable dividends: forward-facing and driver-facing dashcams, telematics systems, GPS tracking, and AI-powered driver monitoring systems are linked to 5–15% premium discounts because they reduce claims frequency and provide documentation that protects you in disputes.

Offset Insurance Costs with Fuel Savings

The AtoB fuel card offers a practical cost offset: it saves an average of $0.45–$2.00 per gallon across 3,500+ truck stops with 99% acceptance, plus it provides IFTA reporting tools and early pay options to smooth cash flow. Freeing up $2,000–$4,000 monthly in fuel savings directly offsets insurance expenses. Work with specialists who understand trucking insurance complexities rather than generalist agencies. Your agent should ask detailed questions about your actual operation, not just fill out a form based on assumptions.

Provide Complete Information and Documentation

Provide complete, accurate information about your safety history, maintenance records, and compliance documentation. Incomplete applications trigger conservative underwriting that inflates quotes unnecessarily. Document everything: your clean safety record, driver training investments, and compliance with DOT requirements. This documentation becomes leverage when negotiating rates with carriers. Most shippers and brokers demand at least $1 million in liability coverage, even though federal minimums sit lower, so understanding your actual coverage needs prevents costly gaps.

Final Thoughts

Owner-operator trucking insurance requires three critical decisions: selecting the right coverage types, understanding what drives your costs, and taking action before your renewal date arrives. The three core coverages-commercial auto liability, physical damage, and cargo insurance-form your minimum foundation, but bobtail coverage, workers’ compensation, and general liability represent the real financial exposure most operators face. A single claim that falls outside your existing policies can transform a manageable loss into a business-ending disaster.

Your premium depends on factors largely within your control: your driving record, CSA scores, safety technology investments, and service territory all shape what carriers will charge. Shopping three or more carriers 60 days before renewal consistently saves 15–25% compared to accepting the first offer, and your deductible choices plus documentation of compliance give you negotiating leverage that most operators never use. Adding bobtail, general liability, and workers’ compensation costs $3,000–$4,000 annually-far less than a single claim that falls outside your existing policies.

We at Saberlines Insurance Services specialize in helping owner-operators navigate these decisions and secure coverage that actually protects them while keeping costs competitive. Contact us today for a fast, affordable quote that reflects your actual risk profile, not generic assumptions. Your owner-operator trucking insurance strategy determines whether a claim strengthens or destroys your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.