Contractor Equipment Insurance: Protecting Your Tools and Machines

Your equipment is your livelihood. When a drill breaks down, a generator fails, or tools vanish from a job site, your business stops moving forward.

That’s where contractor equipment insurance comes in. We at Saberlines Insurance Services know that protecting your tools and machines isn’t optional-it’s essential to keeping your operations running smoothly.

What Contractor Equipment Theft and Damage Cost You

How Contractor Equipment Insurance Works

Contractor equipment insurance covers moveable tools and machines that travel between job sites. Unlike standard business property coverage that protects items in one fixed location, this specialized inland marine insurance follows your equipment wherever it goes-to active job sites, storage yards, vehicles, and client properties. Coverage typically includes power tools, hand tools, generators, compressors, laptops, protective gear, and other portable equipment. You can insure scheduled items (high-value tools listed individually on your policy) or unscheduled items (aggregate coverage up to a limit). The Hartford and other carriers offer replacement cost coverage for equipment under five years old, meaning you receive the full cost of a new replacement rather than depreciated actual cash value. Some policies automatically cover newly purchased equipment for a grace period, giving you time to formally add items to your schedule. What matters most is that your coverage moves with your equipment, protecting against theft during transport, damage from accidents, vandalism, and weather events.

The Real Cost of Equipment Loss

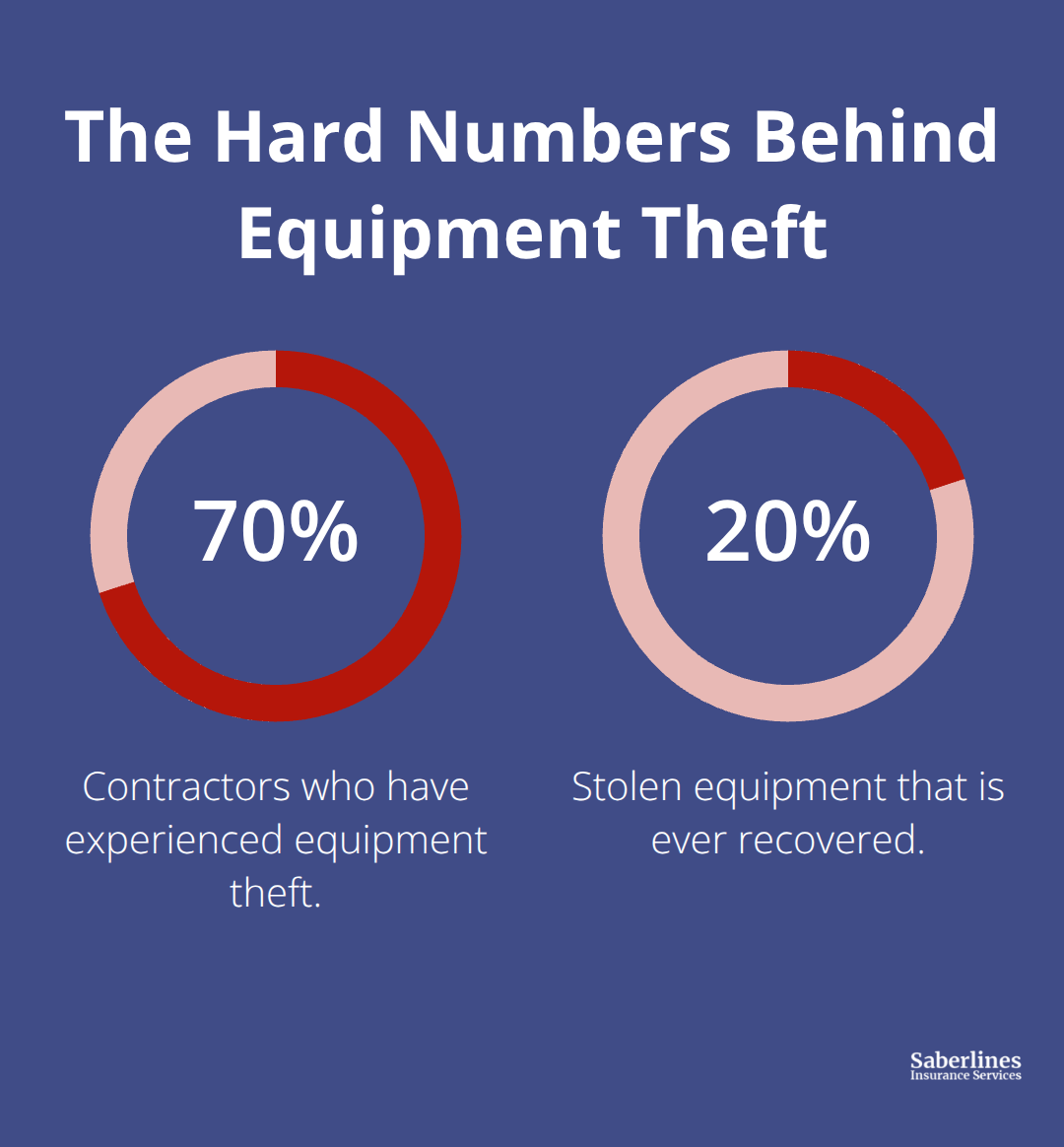

The financial reality of equipment loss hits hard. According to Equipment World survey data, approximately 70 percent of contractors have suffered equipment theft, and when theft happens, the average stolen piece of equipment costs about $46,000 to replace. U.S. contractors lose roughly $1 billion annually to heavy equipment and tool theft combined. Only about 20 percent of stolen equipment is ever recovered, which means most losses become permanent hits to your bottom line.

Theft risk varies significantly by equipment type. A skid steer is twice as likely to be stolen as a backhoe, and John Deere equipment is about three times more likely to be stolen than Bobcat according to National Equipment Register Theft Reports. This means your specific equipment type directly influences your vulnerability.

How Equipment Damage Stops Your Operations

Beyond theft, equipment damage from job site accidents, transport mishaps, or weather events stops work immediately. A broken generator halts an entire project. A damaged compressor forces you to rent a replacement at emergency rates. Without proper insurance, you absorb these costs directly, delaying projects, disappointing clients, and draining cash reserves. Equipment loss damages your reputation and can force you to turn down jobs you cannot complete on schedule.

The next section explores the specific coverage options available to protect your equipment and how to select limits that match your actual needs.

What Your Equipment Coverage Actually Protects

Three Scenarios Standard Policies Miss

Contractor equipment insurance protects three distinct scenarios that standard business policies ignore. First, it covers equipment actively used on job sites, meaning your tools stay protected while you work with them, not just when locked away. Second, it protects equipment in transit between locations and during storage at yards or off-site facilities-where most theft actually occurs.

Third, it covers theft, accidental damage, and in some cases equipment breakdown, addressing the real-world losses that halt your projects cold.

Replacement Cost vs. Actual Cash Value

The Hartford offers replacement cost coverage for equipment under five years old, which pays you the full cost of new replacements rather than depreciated values. This matters significantly when you replace a generator or compressor mid-project. Some carriers include automatic coverage for newly purchased equipment for a grace period, eliminating the gap between purchase and formal policy scheduling. This flexibility protects contractors who buy replacement equipment on an emergency basis and cannot afford coverage delays.

Scheduled vs. Unscheduled Equipment

Your specific coverage needs depend on how you operate. If you store equipment at multiple locations or transport tools constantly between job sites, you need transit and storage protection explicitly included in your policy. Equipment scheduled individually on your policy receives higher coverage limits, while unscheduled miscellaneous tools typically cap at $500 per item and $10,000 per occurrence. For high-value items like generators or specialized machinery, scheduling protects your actual investment. Unscheduled coverage works well for hand tools and lower-value portable equipment that accumulates over time.

Borrowed and Rented Equipment Protection

Rented or borrowed equipment deserves explicit coverage too, since clients sometimes hold you liable when their leased machinery sustains damage in your possession. Most carriers offer up to $50,000 per occurrence for liability on borrowed equipment and up to $100,000 for damage to equipment you’re borrowing. The National Equipment Register Theft Reports show John Deere equipment faces three times higher theft risk than Bobcat, meaning your equipment type directly influences what deductible and limit structure makes financial sense.

Theft Recovery as an Active Tool

Theft protection becomes even more valuable when carriers offer rewards up to $5,000 for information leading to recovery, turning your policy into an active recovery mechanism rather than just a payout mechanism. This approach transforms your insurance from passive protection into a tool that actively works to return your stolen assets. Understanding what your coverage actually protects sets the stage for the next critical decision: determining the right coverage limits and cost structure for your specific operation.

How Your Equipment Type and Storage Habits Shape Your Premium

Your insurance premium reflects three concrete realities: what equipment you own, where you store it, and your history of losses. Equipment value drives the base cost, with small tools averaging around $14 per month while specialized machinery costs significantly more. Location matters enormously. A job site in a high-crime area or disaster-prone region costs more to insure than the same equipment stored in a secured, locked facility. According to industry data, secure offsite storage substantially lowers your premium compared to leaving equipment on open job sites or in unsecured yards. Your claims history determines everything else. Contractors who file multiple claims pay higher rates regardless of equipment value, while those with clean records negotiate better pricing.

Equipment Type and Theft Risk

The type of equipment itself influences theft risk dramatically. John Deere machinery costs roughly three times more to insure than Bobcat according to National Equipment Register Theft Reports, reflecting actual theft patterns in your market. Your deductible choice directly impacts monthly cost. Selecting a $1,000 deductible costs less than a $500 deductible, but you absorb more of each loss yourself. The coverage type matters too. Replacement cost coverage for newer equipment costs more than actual cash value but protects your real financial exposure when a generator or compressor fails mid-project.

Security Investments That Lower Your Premiums

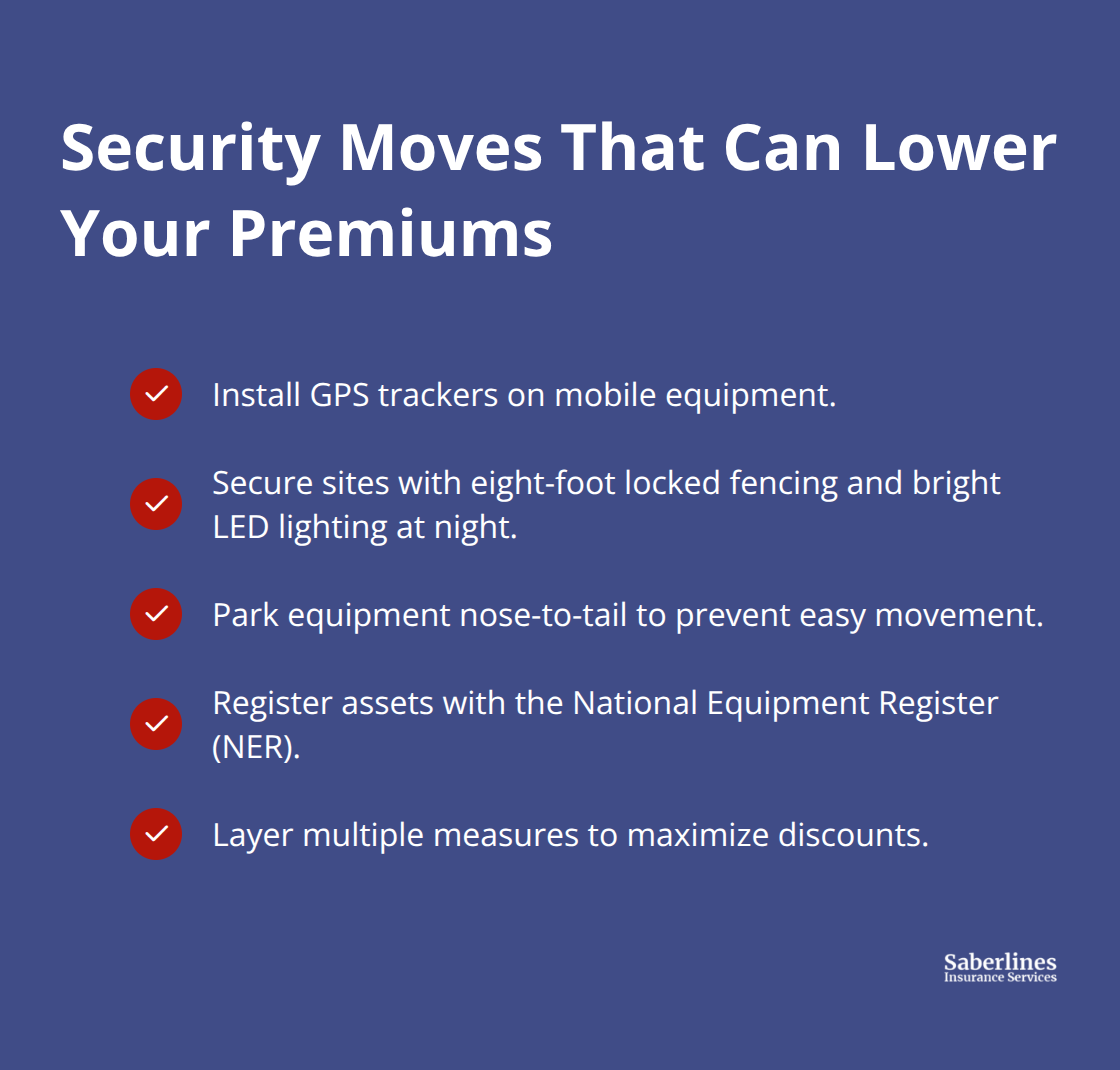

Security measures directly lower your premiums because they reduce theft risk. Installing GPS trackers on mobile equipment qualifies for theft protection discounts from many carriers, sometimes including deductible waivers if you maintain an active tracking device. Surrounding your job site with an eight-foot locked fence and fully illuminating it at night with LED lighting signals serious loss prevention to insurers.

Parking equipment nose-to-tail so thieves cannot move one machine without moving others demonstrates practical theft deterrence. Registering equipment with the National Equipment Register provides identification and theft alerts while signaling to insurers that you take security seriously. These measures accumulate, and insurers reward contractors who implement multiple protections with meaningful rate reductions.

Deductible Strategy and Coverage Limits

Your deductible strategy controls cost effectively. Paying your annual premium upfront instead of monthly can unlock discounts from most carriers. Bundling your contractor equipment insurance with a business owners policy or commercial general liability policy typically reduces your overall cost versus purchasing policies separately. Paying more upfront through higher deductibles on lower-value items while maintaining lower deductibles on high-value equipment balances protection and affordability. Your coverage limits should match your actual equipment inventory, not theoretical maximum scenarios. Overinsuring creates unnecessary expense, while underinsuring leaves gaps that cost far more when losses occur.

Final Thoughts

Contractor equipment insurance protects your most valuable business assets from the financial devastation that theft and damage create. The data proves this reality: 70 percent of contractors experience equipment theft, and when it happens, the average loss exceeds $46,000. Without proper coverage, a single theft or accident can derail your operations, damage client relationships, and force you to absorb costs that directly reduce your profit margin.

The protection you need depends on your specific situation-if you transport tools between job sites regularly, you need transit and storage coverage explicitly included; if you own high-value equipment like generators or specialized machinery, scheduled coverage with replacement cost protection makes financial sense; if you work with borrowed or rented equipment, liability coverage for damage in your possession protects you from unexpected claims. Your deductible choice, security measures, and equipment type all influence your final premium, but the investment in proper contractor equipment insurance costs far less than replacing stolen or damaged equipment out of pocket. Comparing quotes from multiple carriers reveals significant price differences based on your specific risk profile, and bundling with general liability or a business owners policy typically reduces your overall cost.

Gather your equipment inventory with values and serial numbers, note your storage locations and security measures, and contact an insurance agent who understands contractor operations. Paying your annual premium upfront instead of monthly unlocks additional discounts from most carriers. Visit Saberlines Insurance Services to explore your options and secure the right protection at competitive rates.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.