Small Business General Liability: Essential Protection for Growth

One accident on your business premises can derail months of growth. At Saberlines Insurance Services, we’ve seen how quickly a single claim can become expensive without the right protection.

Small business general liability insurance isn’t optional-it’s the foundation that keeps your business standing when things go wrong. This guide walks you through what coverage actually protects you, the claims we see most often, and how to pick limits that match your real business needs.

What General Liability Actually Covers

The Core Protection Your Business Needs

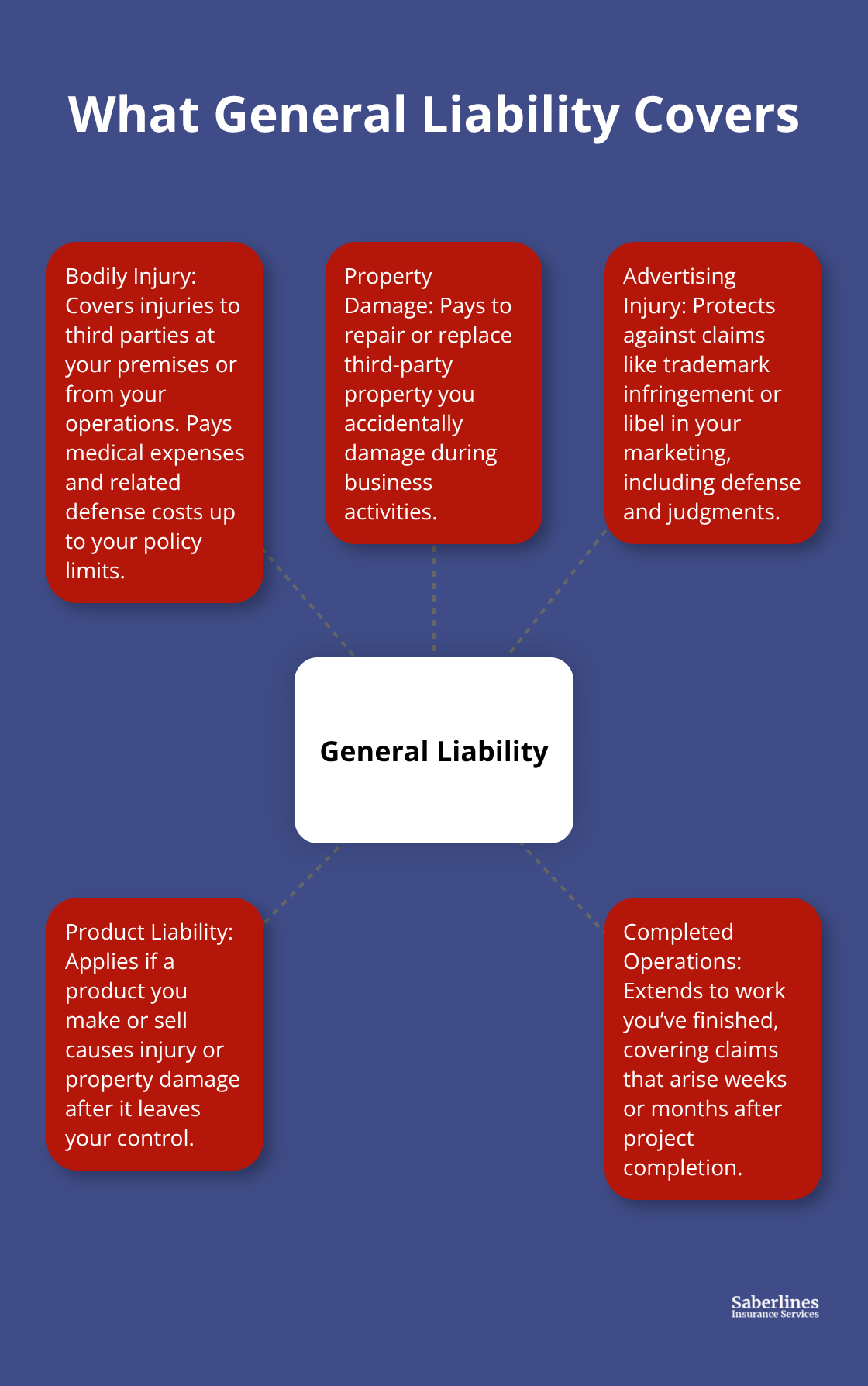

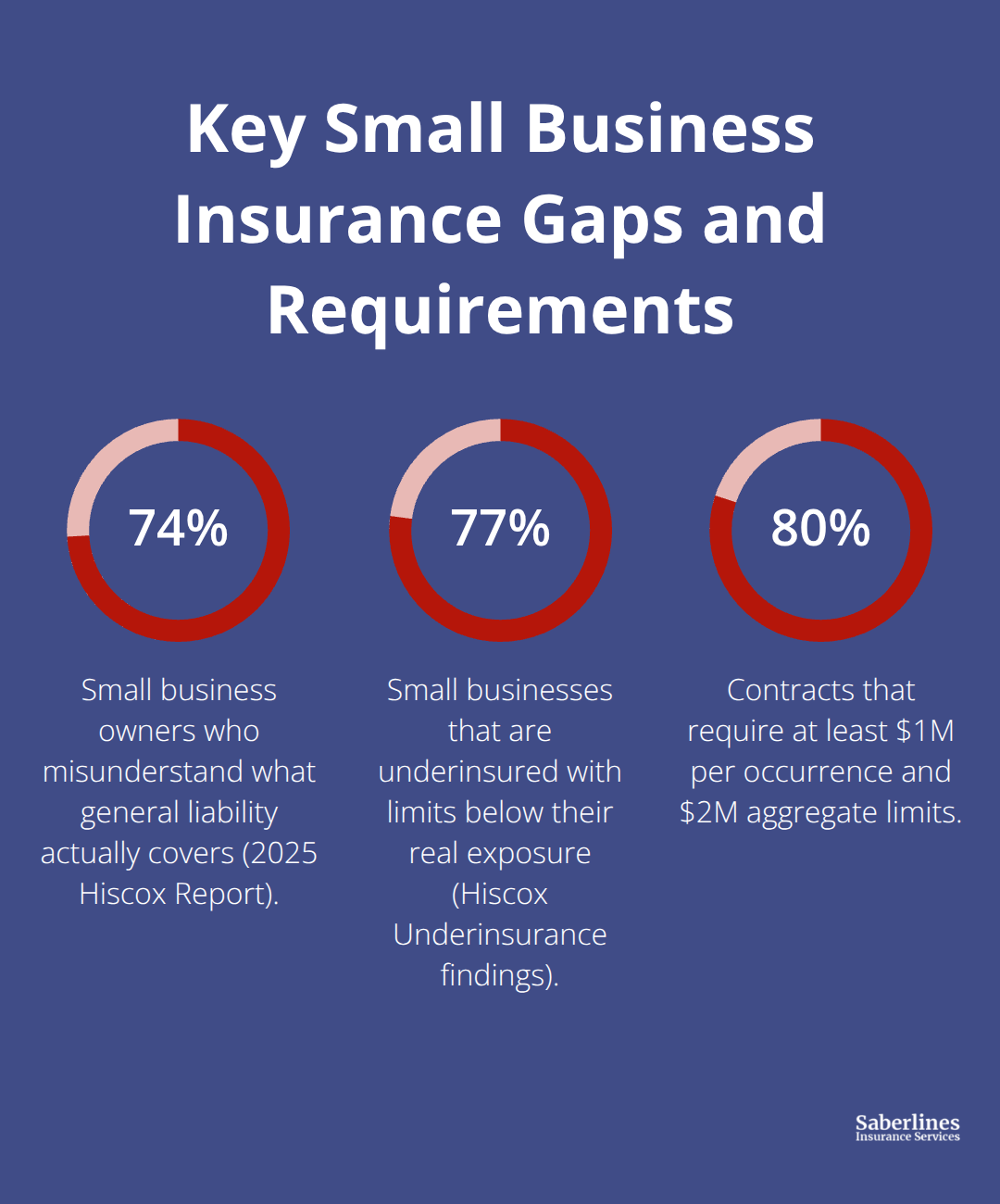

General liability insurance protects your business when a third party claims you caused them harm. This means a customer who slips on your floor, a vendor whose property you damage, or someone who alleges your marketing materials infringed their copyright. The coverage pays for medical bills, property repairs, legal defense, and settlements up to your policy limits. The 2025 Hiscox Underinsurance in Small Business Report found that 74% of small business owners misunderstand what general liability actually covers, which is why specifics matter.

What Your Policy Actually Pays For

Your policy covers bodily injury claims when a client gets injured at your office. It pays medical expenses for a customer hurt on-site and covers third-party property damage such as accidentally damaging equipment belonging to a client. Advertising injury claims also fall under this protection-if someone alleges your ad infringed their trademark or published false statements about them, your insurer handles the legal costs and any judgment.

Product liability applies if you manufacture or sell products that cause injury or damage. Completed operations coverage extends protection to work you finished, so claims arising weeks or months after a project ends remain covered.

What General Liability Does Not Cover

Your policy will not pay for injuries to your own employees, which workers’ compensation handles instead. It will not cover damage to your own property or loss of business income from a fire or natural disaster. It will not pay for professional mistakes or negligence in delivering services, which is why service-based businesses need professional liability insurance separately. Understanding these gaps prevents costly surprises when a claim arrives.

Pricing and Practical Next Steps

The Hartford’s typical annual premium for general liability runs around $810, though your actual cost depends on your industry, revenue, employee count, and location. A small salon faces different risk than a consulting firm, so underestimating your exposure can leave you unprotected. Many businesses start with a Business Owner’s Policy that bundles general liability with commercial property and business income coverage, simplifying management and often reducing total premium costs through bundling discounts up to 10%. Clients will frequently request a certificate of liability insurance before signing contracts, so having this coverage in place removes friction from sales conversations and signals professionalism to prospective partners. The right coverage limits, however, depend on understanding your specific industry risks and contractual obligations.

Common Claims Small Businesses Face

Slip and Fall Accidents Cost More Than You Expect

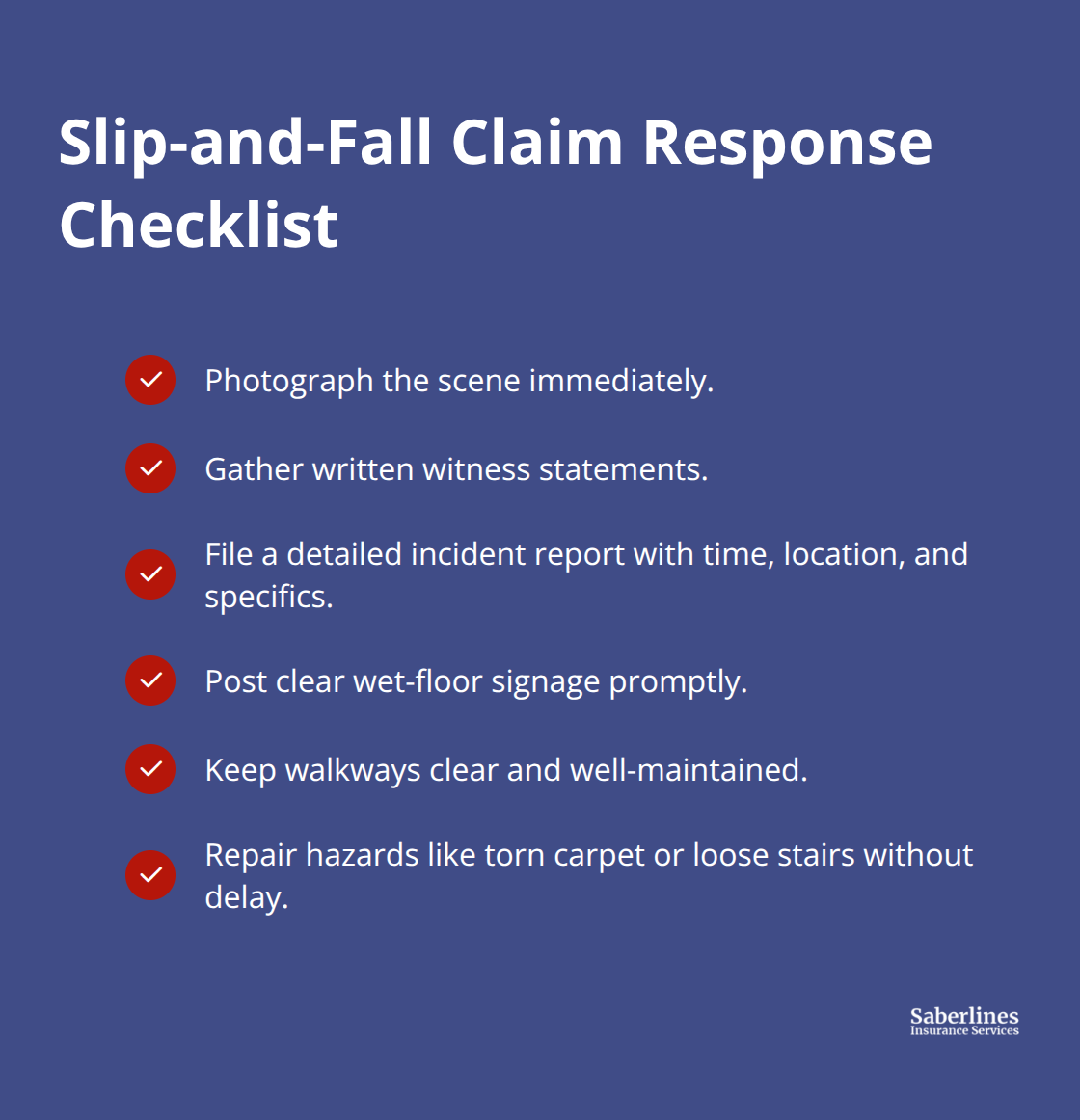

Slip and fall accidents dominate general liability claims across small businesses. A customer steps on a wet floor without a warning sign, or someone trips on a loose carpet in your waiting area, and suddenly you face medical bills, lost wages, and legal fees. The Hartford’s data shows these incidents cost businesses thousands in settlements and defense expenses, which is why your general liability policy covers medical payments for third parties injured on your premises. Documentation separates a manageable claim from a catastrophic one. Photograph the scene immediately after an incident, gather witness statements, and file an incident report with specific details about what happened, where, and when.

If you operate a retail location, salon, or office with customer traffic, slip and fall risk is not theoretical-it becomes a near-certainty over time. Install proper signage for wet floors, maintain clear pathways, and fix hazards like torn carpet or loose stairs within days, not weeks. Your general liability policy covers the medical expenses and legal defense if someone is injured despite your precautions, but prevention remains cheaper than any claim.

Third-Party Property Damage Claims Hit Service Businesses Hard

Third-party property damage claims arrive when your business operations damage someone else’s equipment, vehicle, or building. A contractor accidentally breaks a client’s window during installation work. A delivery driver clips a parked car while unloading merchandise. A plumber’s tools damage a customer’s flooring during a repair job. These claims happen constantly in service-based and trades businesses, and general liability covers the repair costs and legal defense up to your policy limits.

The 2025 Hiscox report revealed that 77% of small businesses are underinsured, meaning many owners carry limits far too low for their actual exposure. If you cause damage worth $50,000 but your policy limit is $25,000, you pay the difference from cash flow. Evaluate your contract requirements carefully-many clients demand minimum coverage limits of $1 million or higher before they hire you. Document all work with photos before and after completion, use written scope statements that detail exactly what you will and will not touch, and require clients to point out pre-existing damage.

Transportation Businesses Face Acute Property Damage Exposure

For transportation businesses, property damage exposure reaches especially high levels. A single accident involving cargo or a parked vehicle can trigger claims in the six figures. Owner-operators and fleets need coverage limits that match real-world risk, not wishful thinking. The stakes in this industry demand that you assess your actual exposure honestly and secure adequate limits before an incident occurs.

How to Choose the Right Coverage Limits

Your Industry Determines Your Exposure

Your industry determines your exposure far more than your wishful thinking does. A salon with three employees faces entirely different liability risk than a construction contractor moving heavy equipment on client property. Owner-operators carrying $500,000 in coverage limits often discover they need $1 million or $2 million after reviewing actual contract demands and cargo value. Start by examining your contracts-most clients specify minimum coverage limits before they sign with you, and these requirements are non-negotiable.

Match Your Policy to Contract Requirements

If you work in trades or service delivery, pull your last ten contracts and list every insurance requirement you’ve agreed to. You’ll likely find that 80% demand $1 million per occurrence and $2 million aggregate at minimum. Matching your policy to these contractual obligations prevents claims from being denied due to insufficient limits and keeps your relationships intact.

Transportation businesses face acute exposure because a single incident involving cargo or vehicles can generate six-figure claims instantly.

Calculate Coverage Based on Revenue and Assets

Revenue and assets matter next. The Hiscox Underinsurance Report found that 77% of small businesses carry limits too low for their actual exposure. A business generating $500,000 annually with $250,000 in equipment and inventory should carry at least $1 million per occurrence. If you cause damage worth $800,000 but your limit is $500,000, you absorb the $300,000 gap personally.

If you operate commercial vehicles, your general liability limit should account for potential injuries to third parties plus property damage to vehicles or goods. Many owner-operators underestimate this exposure because they focus on frequency rather than severity. One catastrophic claim can exceed a $500,000 limit in minutes.

Compare Premium Costs Against Protection Gaps

The Hartford’s data shows typical general liability premiums around $810 annually, but limits of $1 million per occurrence run closer to $1,200 to $1,500 depending on your industry and location. Transportation businesses and contractors pay more because their risk profiles demand it. Ask your agent to model three scenarios: your minimum contractual requirement, one tier above that, and the limit that matches your revenue and asset value.

Compare the premium difference honestly. The gap between $500,000 and $1 million coverage often costs only 20% to 30% more annually but protects exponentially more of your business. Document your decision in writing so you can prove you made an informed choice. This matters if an underinsured claim arrives and someone questions whether you assessed your exposure properly.

Review Limits When Your Business Changes

Review these limits every two years or immediately if your revenue grows by more than 20%, you add locations, or you change service offerings. A business that doubled revenue in the past year likely needs higher limits. Transportation companies should reassess whenever cargo values increase, routes change, or fleet size expands. Your coverage must scale with your actual exposure, not remain frozen at the limits you chose three years ago.

Final Thoughts

A claim arrives without warning, and suddenly your small business general liability coverage becomes the difference between recovery and financial crisis. We at Saberlines Insurance Services have watched businesses bounce back quickly because they carried adequate limits, and we’ve seen others struggle for years after underestimating their exposure. The premium difference between $500,000 and $1 million coverage often costs only 20 to 30 percent more annually, yet it protects exponentially more of what you’ve built.

Pull your contracts today and identify every insurance requirement your clients demand, then compare those minimums against your actual revenue and asset value. Transportation businesses and owner-operators face acute exposure that demands honest assessment-a single incident involving cargo or vehicles can generate claims that dwarf a $500,000 limit in minutes. Document your coverage decision in writing so you can prove you made an informed choice based on your contract requirements, revenue, and industry benchmarks.

Review your limits every two years or whenever your business changes meaningfully (revenue growth of 20 percent or more, new locations, or expanded service offerings all signal that reassessment matters). Contact us for a quote and let’s match your small business general liability limits to your real exposure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.