General Liability Insurance California: What Local Businesses Need

Running a business in California means facing real liability risks every single day. One accident or injury claim can drain your finances fast, which is why general liability insurance California is non-negotiable for local operations.

At Saberlines Insurance Services, we’ve helped countless California business owners understand exactly what coverage they need and why it matters. This guide breaks down the essentials so you can protect your business with confidence.

What Your General Liability Policy Actually Protects

The Three Core Areas of Coverage

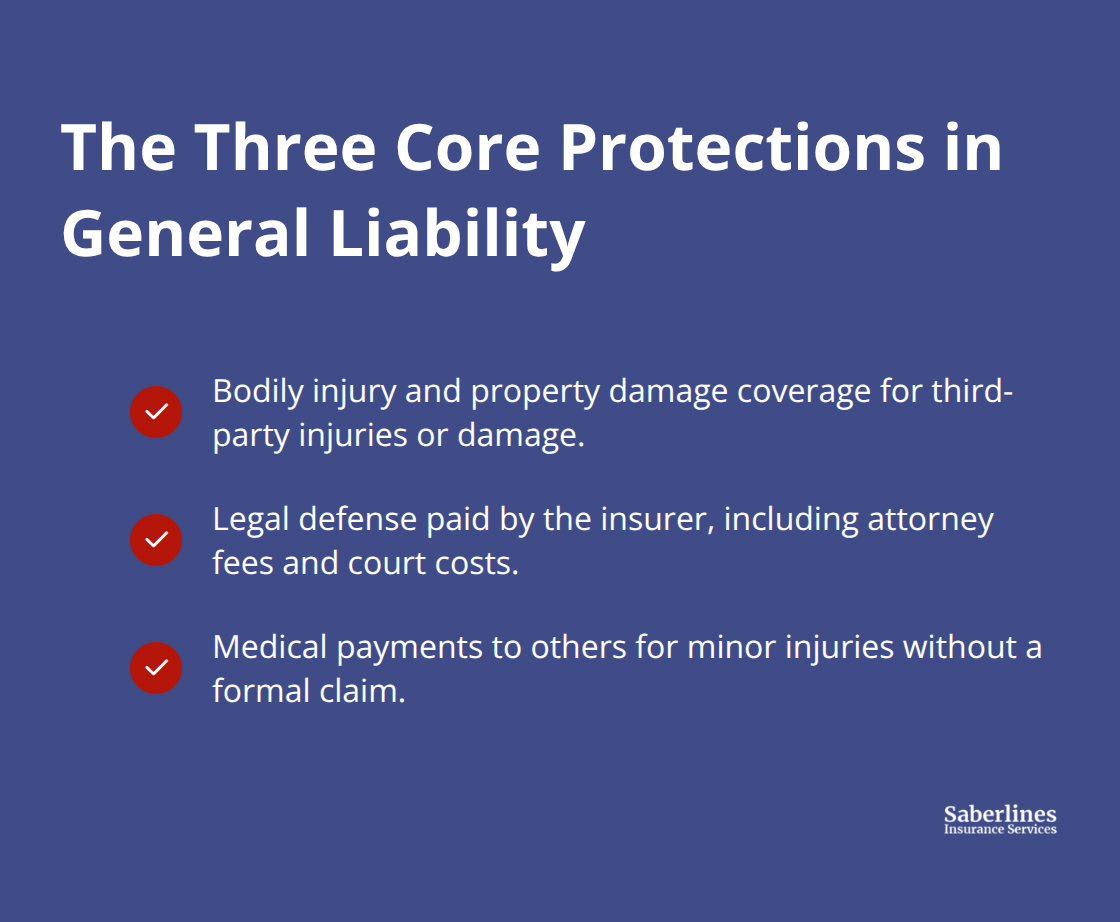

General liability insurance covers three core areas that directly impact your bottom line when something goes wrong. First, bodily injury and property damage claims-these are the situations where someone gets hurt on your premises or during your operations, or your business accidentally damages someone else’s property. If a customer trips in your store and breaks their leg, or your delivery vehicle hits a parked car, general liability steps in to cover medical bills and repair costs. Second, the policy pays for your legal defense.

If you are sued, the insurer covers attorney fees, court costs, and investigation expenses, which can easily exceed $50,000 even for a straightforward case. Third, medical payments to others provides immediate coverage for minor injuries without requiring a formal claim or lawsuit, typically up to $5,000 or $10,000 per person depending on your policy limits.

This coverage matters because it stops small incidents from becoming expensive disputes. A single lawsuit can cost tens of thousands in legal fees alone, even if you ultimately win the case.

Determining Your Coverage Limits

California businesses typically carry $1 million per occurrence and $2 million aggregate limits as a baseline, according to MoneyGeek’s analysis of over 20,000 California business profiles. However, your actual coverage needs depend entirely on your industry and operations. A landscaper working on residential properties faces different exposure than a consulting firm operating from an office-riskier professions with physical work or customer interaction on-site naturally require higher limits.

Your specific exposure determines what you should carry. Construction companies, manufacturers, and service businesses that work on client premises typically need higher limits than office-based operations.

Critical Coverage Gaps You Must Address

The policy excludes certain exposures you need to know about, such as care, custody, and control of property that isn’t yours. If you store client equipment, you will need additional inland marine coverage. For businesses that contract with others, contractual liability coverage is essential because it covers indemnity clauses in those agreements. Many California contractors and service businesses overlook this gap until a contract requires them to assume liability they thought was covered.

If your work involves products you manufacture or sell, products liability and completed operations coverage protect you after delivery or project completion. This protection matters because claims often surface months or even years later, long after you have moved on to other projects.

Understanding these gaps now prevents costly surprises when you need coverage most. The next section walks you through how to assess your specific risks and select the right limits for your operation.

Why California Businesses Need General Liability Coverage

The Legal and Financial Reality

California law does not mandate general liability insurance the way it requires workers’ compensation coverage, but operating without it exposes your business to financial ruin. A single liability claim can exceed your annual revenue, and California courts award damages aggressively. According to data from the California Department of Insurance, premises liability, operations liability, and products liability claims represent the largest categories of commercial losses in the state. If a customer is injured at your location or your product causes harm, you face medical bills, property damage costs, and legal defense expenses that pile up faster than most business owners anticipate. Without coverage, you pay these costs directly from your operating account, which forces you to choose between staying solvent and honoring the injured party’s claim. This risk is not theoretical-it happens to California businesses every month.

How Legal Defense Costs Drain Your Resources

Legal defense costs alone can drain $50,000 to $150,000 before a case settles or goes to trial, even if you ultimately win. Your general liability policy covers these attorney fees and court costs upfront, which means you are not forced to liquidate inventory or delay payroll to pay lawyers. For small and mid-sized operations with limited cash reserves, this protection is the difference between surviving a claim and closing your doors.

California’s Higher Insurance Costs and Exposure

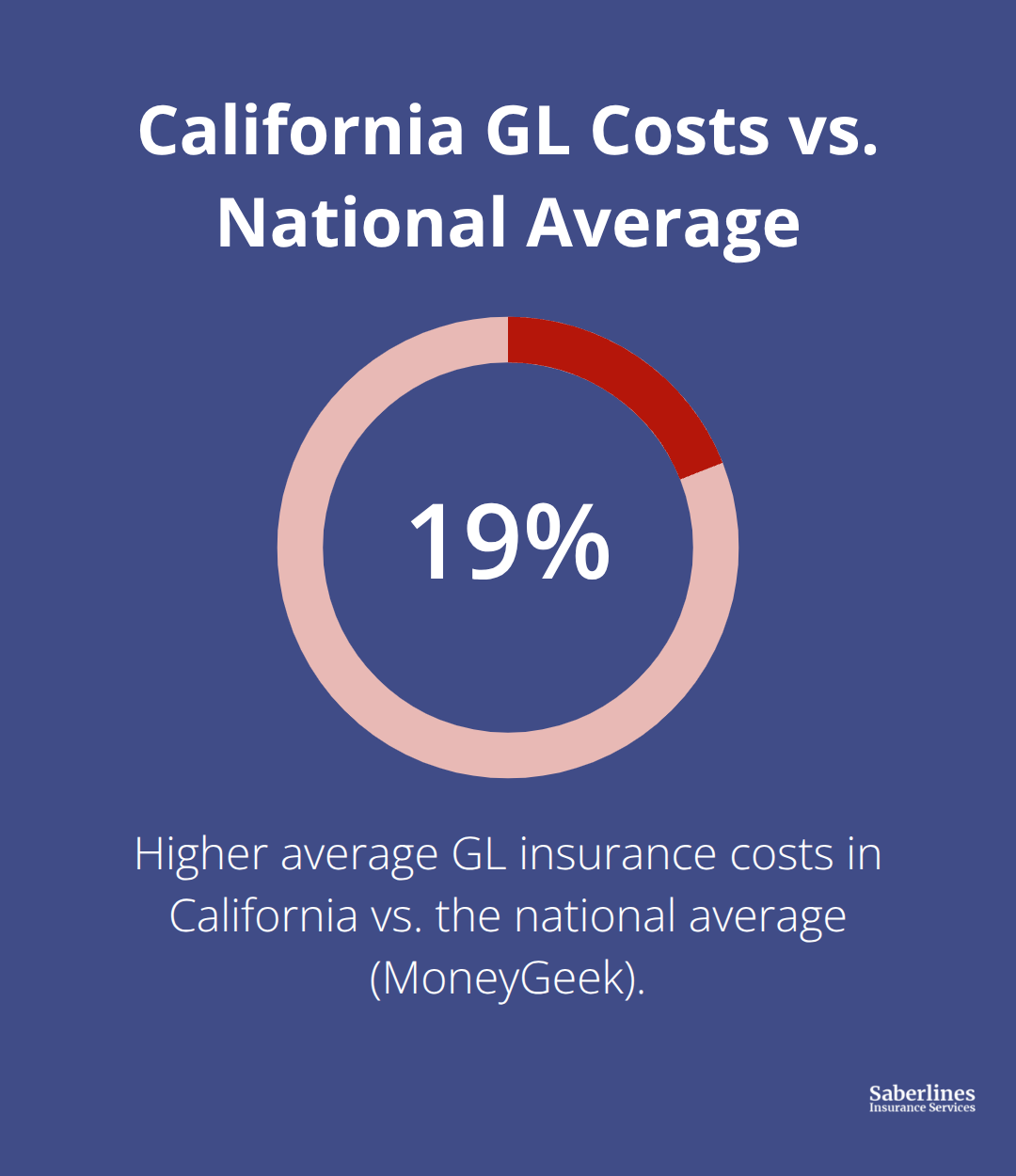

California businesses face higher insurance costs than the national average-roughly 19 percent higher according to MoneyGeek analysis of over 20,000 California business profiles-which means the financial impact of an uninsured loss hits harder in this state. Construction companies, landscapers, contractors, and any business that works on client premises or delivers products faces constant exposure.

Even office-based operations need coverage because customer injuries, property damage, and contractual liability obligations arise without warning.

Determining Your Baseline Coverage

A $1 million per occurrence and $2 million aggregate baseline provides essential protection for most California operations, though your specific industry and work scope determine whether you need higher limits or additional endorsements. The cost of a policy is predictable and manageable; the cost of a single uninsured claim is not. Your next step involves assessing your actual industry risks and selecting coverage limits that match your specific operations.

How to Choose the Right General Liability Policy

Map Your Actual Exposure First

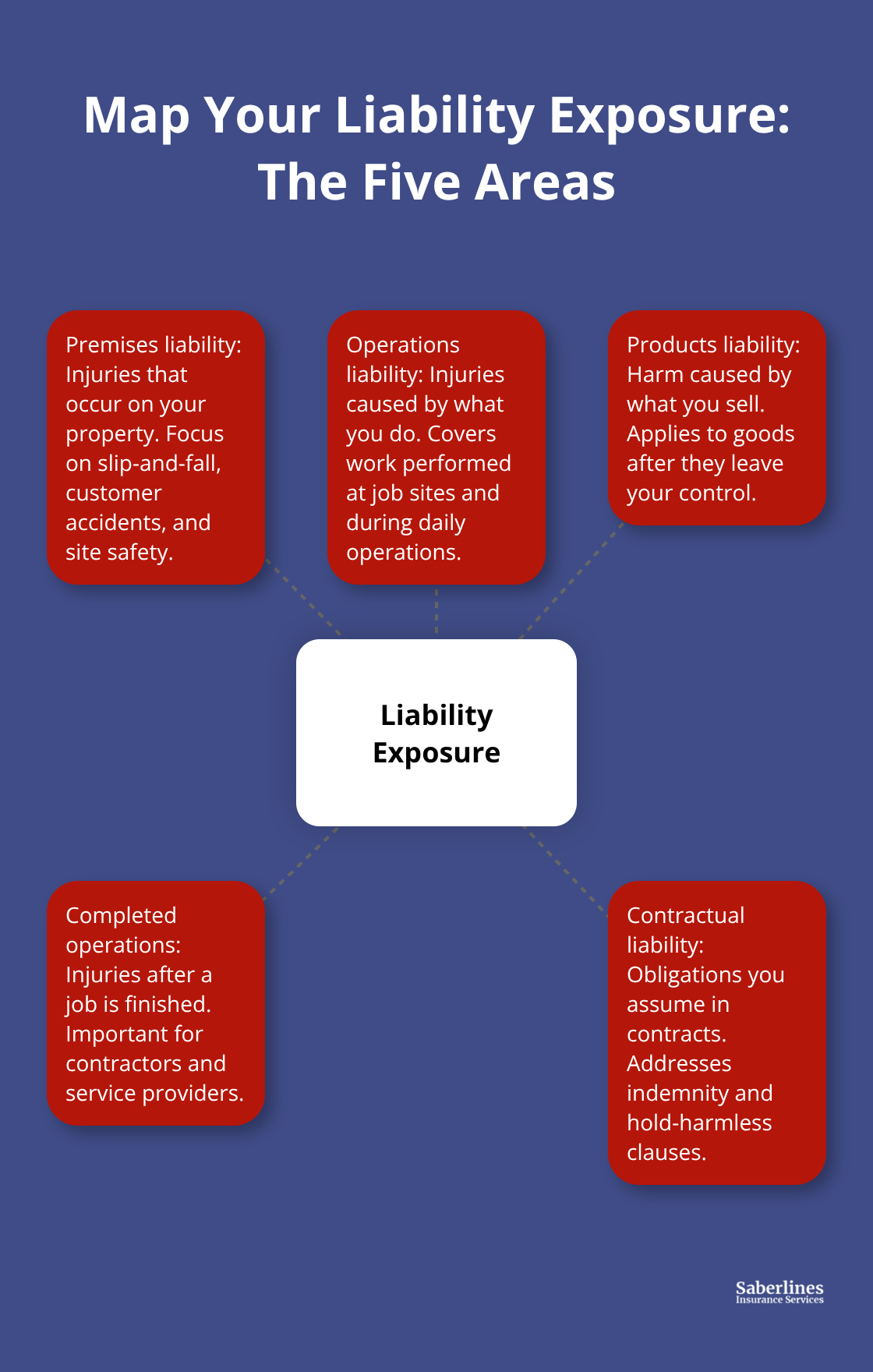

Start by identifying exactly what your business does and where the exposure lives. A contractor installing commercial HVAC systems faces different risks than a staffing agency placing temporary workers, and both differ from a retail shop selling sporting goods. The California Department of Insurance breaks liability into five distinct areas: premises liability (injuries on your property), operations liability (injuries from what you do), products liability (injuries from what you sell), completed operations (injuries after you finish a job), and contractual liability (liability you assume through contracts). You need to know which of these five actually apply to your operation before you can pick intelligent coverage limits.

A roofing company worries most about operations and completed operations; a restaurant worries about premises and products; a consultant might only need contractual liability to cover indemnity clauses in client agreements. Spend time mapping your actual exposure instead of defaulting to the $1 million per occurrence baseline that works for many California businesses.

Set Coverage Limits That Match Your Risk

Higher-risk industries like construction, landscaping, and manufacturing typically need $2 million per occurrence or more. MoneyGeek’s analysis of California businesses shows that riskier professions like landscapers pay substantially more than lower-risk professions like consultants, which means your premium already reflects your industry’s exposure. The question is whether your limits match that exposure.

If you work on client premises, install equipment, or manufacture products, $1 million per occurrence leaves you dangerously exposed. Your actual rate depends on your business type, location, number of employees, and claims history. Work with an agency that understands California’s specific risks and can explain exactly why your policy options are what they are.

Understand Deductibles and Aggregate Limits

Deductibles and aggregate limits matter more than most business owners realize. Raising your deductible from $500 to $2,500 or $5,000 cuts your premium noticeably, but it also means you pay more out of pocket when a claim happens. For established businesses with strong safety records and healthy cash reserves, higher deductibles make financial sense. For newer operations or those with tight cash flow, accepting a lower deductible costs more upfront but protects your working capital.

Your aggregate limit is the total the insurer pays across all claims in a year. A $2 million aggregate with a $1 million per-occurrence limit means one major claim can exhaust most of your annual protection. Businesses that operate multiple locations or serve dozens of customers daily need higher aggregates because claim frequency matters. A landscaper doing 50 jobs a month faces higher frequency risk than one doing 5 jobs a month, even if per-occurrence exposure is identical.

Compare Quotes Using Identical Terms

When comparing quotes, use identical limits and deductibles across all carriers so you can actually compare pricing. Many California businesses make the mistake of comparing a $1 million/$2 million policy from one carrier against a $2 million/$4 million policy from another and concluding the second is overpriced, when really the limits are different. Progressive’s 2024 data shows a median monthly cost of $60 for new general liability customers with an average of $85 per month, but these are baselines for minimal exposure.

Final Thoughts

General liability insurance California protects your business from the financial devastation that follows a single accident or injury claim. The coverage you carry today determines whether your operation survives tomorrow’s lawsuit or closes its doors. At Saberlines Insurance Services, we understand that California businesses face unique risks and higher costs than most states, which is why choosing the right policy requires more than picking the cheapest quote.

Your takeaway is straightforward: map your actual exposure across premises, operations, products, completed operations, and contractual liability, then set coverage limits that match your industry’s real risk rather than just the baseline $1 million per occurrence. Understand how deductibles and aggregate limits affect both your premium and your out-of-pocket costs when a claim happens. Compare quotes using identical terms so you can actually see what you are paying for.

Your next step is getting a quote tailored to your specific operation. Contact Saberlines Insurance Services to discuss your coverage needs with an agency that specializes in California commercial insurance, and we can explain exactly what your business needs and why. Review your policy annually or whenever your business changes-new employees, additional locations, expanded services, or changes to your products all shift your exposure and create gaps that cost money to fix later.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.