NEMT Insurance California: Key Requirements for California Operators

Running a NEMT service in California means navigating complex insurance requirements that directly impact your bottom line. The state’s regulations are strict, and getting coverage wrong can expose your business to serious liability.

At Saberlines Insurance Services, we’ve helped dozens of California NEMT operators find the right insurance solutions. This guide breaks down exactly what you need to know about NEMT insurance in California-from mandatory coverage minimums to practical cost-saving strategies.

What Coverage Do You Actually Need in California

Commercial Auto Liability: The Non-Negotiable Foundation

California requires NEMT operators to carry commercial auto liability insurance with a minimum of $1 million per occurrence. This is not negotiable if you want to work with Medicaid brokers or operate legally. Most Medicaid broker contracts in California demand exactly this limit, and hospitals or referral sources will ask for proof before sending patients your way.

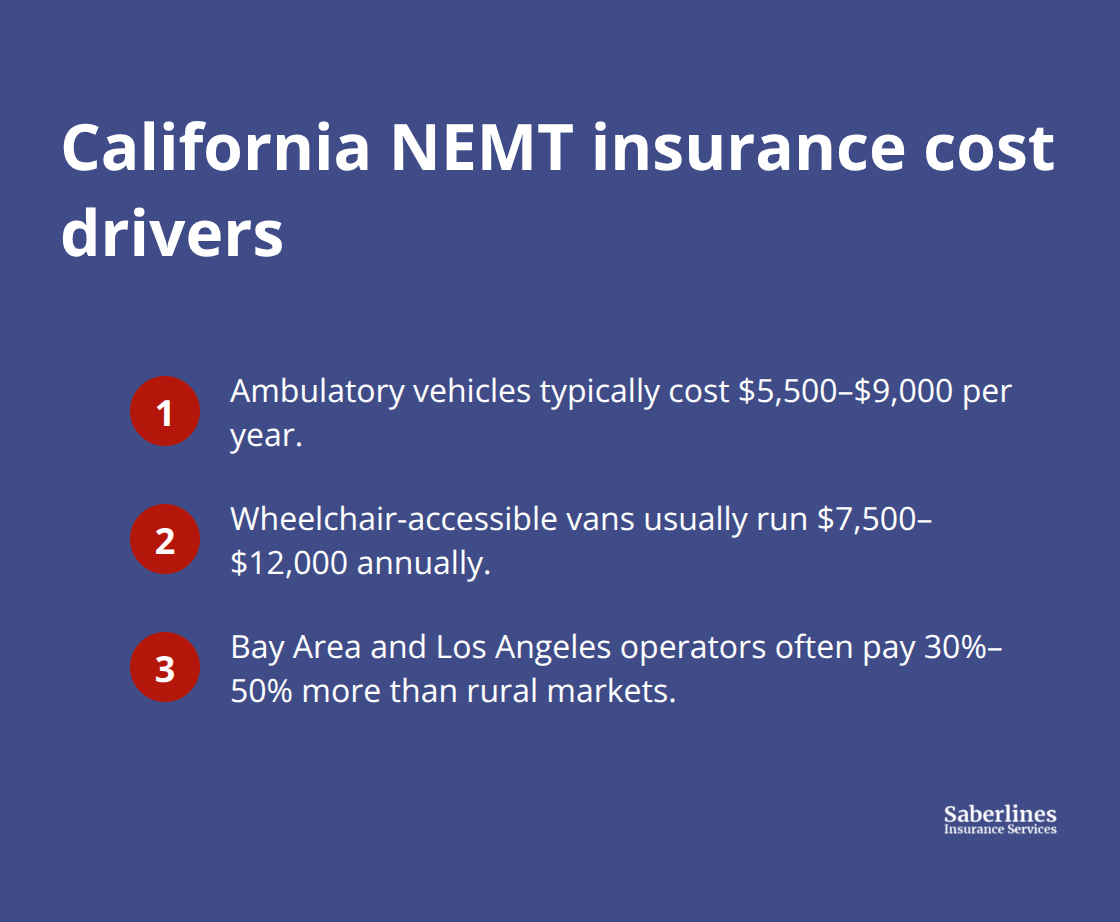

The cost varies significantly by vehicle type. Ambulatory vehicles typically run $5,500 to $9,000 per year, while wheelchair-accessible vans cost $7,500 to $12,000 annually according to 2026 California market data. Your garaging location matters more than you might think-operators in the Bay Area and Los Angeles pay at the upper end of these ranges, sometimes 30 to 50 percent more than rural California operations.

Managing Costs Through Safety and Claims History

A single at-fault accident raises your rates by 30 to 50 percent at renewal, so defensive driving training and telematics installation become serious cost management tools. General liability coverage of $1 million per occurrence and $2 million aggregate rounds out the auto liability picture and protects against third-party claims unrelated to vehicle operation.

Essential Endorsements and Additional Protections

Workers’ compensation is mandatory for California employers with employees, and AB5 labor classification rules have pushed costs higher than most other states. Every driver, aide, and dispatch staff member must be covered. Loading and unloading claims account for 40 to 60 percent of NEMT incidents, so you need a specific loading and unloading endorsement on your auto policy to close this coverage gap-standard policies simply do not cover door-through-door service.

Physical damage coverage protects your fleet investment after accidents or theft. Wheelchair securement failures drive a significant portion of claims in the WAV segment, which is why equipment coverage for lifts and mobility devices is essential, not optional. Sexual Abuse and Molestation coverage is required by California Medicaid and most brokers. Hired and Non-Owned Auto liability protects you if you rely on subcontractors or rental vehicles.

Year-One Budgeting and Long-Term Cost Reduction

A typical 3-vehicle startup in California should budget $22,000 to $45,000 for year-one insurance costs, with year-over-year reductions of 15 to 25 percent as you build a clean loss history. New operators face a 30 to 50 percent surcharge in year one that declines over two to three years, so your costs will improve substantially once you demonstrate safe operations. Understanding these baseline costs positions you to evaluate how California-specific regulations shape your compliance obligations and operational expenses.

Staying Compliant With California’s Insurance and Regulatory Framework

Verify Carrier Admission and CPUC Approval

California’s Department of Insurance oversees admitted carriers operating in the state, meaning any insurer writing your NEMT policy must hold a valid certificate of authority from the state. Admitted carriers face California’s solvency requirements and consumer protections, while non-admitted carriers operate outside this framework and expose you to greater risk if a claim dispute arises. The California Public Utilities Commission also regulates for-hire transportation, and NEMT operators must verify that their carriers hold CPUC approval for medical transport operations. Non-compliance here can result in policy cancellation mid-year, leaving you uninsured and ineligible for Medicaid broker contracts. When obtaining quotes, verify each carrier’s admitted status through the National Association of Insurance Commissioners database before binding coverage.

Prepare Documentation for Medicaid Enrollment

California Medicaid enrollment requires proof of compliant insurance before your application is complete, making documentation the operational linchpin of your business. Your certificate of insurance must list your specific vehicles, coverage limits of at least $1 million per occurrence for commercial auto liability, and include Sexual Abuse and Molestation coverage, additional insured endorsements, and primary/non-contributory language with 30-day cancellation notice. Medicaid broker contracts like ModivCare and MTM demand this exact format, and submitting a non-compliant COI delays credentialing by weeks or months. Maintain updated vehicle registrations, current DMV inspection records, and preventative maintenance logs for all fleet vehicles, as insurers review these documents during underwriting and claims investigations.

Build Driver Qualification Files and Safety Records

Driver qualification files must include five years of motor vehicle records for every operator, background checks, and proof of defensive driving training or PASS certification, which typically yields 12 to 15 percent insurance discounts. Document all incidents, accidents, thefts, and near-misses with photographs and witness statements within 48 hours, as claim defense depends on contemporaneous evidence. A documented safety culture (maintenance logs, anti-distracted driving policies, near-miss reporting) compounds safety discounts and can push claims-free discounts to 10 to 40 percent over time.

Address California Labor Classification and Regulatory Changes

California’s AB5 labor classification rules have made worker classification documentation critical; your employment contracts must clearly define whether drivers are employees or independent contractors, as misclassification can invalidate workers’ compensation coverage and trigger state penalties. Subscribe to regulatory alerts from California DHCS and the Department of Industrial Relations to track changes in Medicaid NEMT requirements and workers’ compensation rules that affect your insurance obligations annually. Specialized insurance brokers understand these state-specific compliance demands better than general commercial agents and can guide you through the documentation workflow to avoid coverage gaps or policy cancellations that derail your operation. These compliance foundations position you to evaluate the cost-saving strategies that reduce your insurance burden without sacrificing the protection your business requires.

How to Cut NEMT Insurance Costs Without Sacrificing Coverage

Reducing your NEMT insurance premiums in California requires strategy, not shortcuts. The most effective approach combines bundling coverages, installing safety infrastructure, and partnering with brokers who understand NEMT’s specific risk profile. A 3-vehicle fleet that moves aggressively on these three fronts can realistically cut year-two premiums by 15 to 25 percent compared to year one, then sustain additional 10 to 15 percent reductions in year three as claims-free discounts compound. This matters because insurance often represents 10 to 15 percent of gross revenue in a well-run California NEMT operation, so every percentage point saved translates directly to operational margin.

Bundle Your Coverage and Optimize Deductibles

Consolidating commercial auto liability, general liability, workers’ compensation, physical damage, and specialty endorsements into a single policy package rewards you with 8 to 12 percent savings across the portfolio compared to purchasing each coverage separately from multiple carriers. Within that bundle, raise your physical damage deductible from $500 to $1,000 or $1,500 if your fleet can absorb minor repairs without financial strain. This single adjustment cuts physical damage premiums by 15 to 20 percent while keeping catastrophic vehicle loss protection intact. Pay your premium annually rather than monthly whenever possible, as monthly installments cost 5 to 8 percent more due to administrative fees and payment processing overhead. For a 5-vehicle ambulatory fleet with annual bundled premiums of $35,000, switching to annual payment saves roughly $2,000 per year with zero loss of coverage.

Install Telematics and Document Your Safety Culture

Telematics systems that track vehicle speed, acceleration, braking, and route compliance generate concrete data that insurers view as risk mitigation. Installing telematics qualifies you for 10 to 15 percent premium discounts and simultaneously improves on-time performance and passenger safety. Defensive driving training for all operators yields another 8 to 15 percent discount, while PASS certification or equivalent programs add 12 to 15 percent additional credits. The cumulative effect matters: an operator with telematics, defensive driving certification, and a documented 24-month claims-free record can legitimately expect 30 to 40 percent lower premiums than a comparable operator without these safeguards. Document your safety culture formally through maintenance logs for every vehicle, written anti-distracted driving policies, and a near-miss reporting process. This documentation becomes your defense during underwriting conversations and renewal negotiations, allowing you to justify lower rates based on measurable risk reduction rather than hope.

Partner With Specialized NEMT Brokers

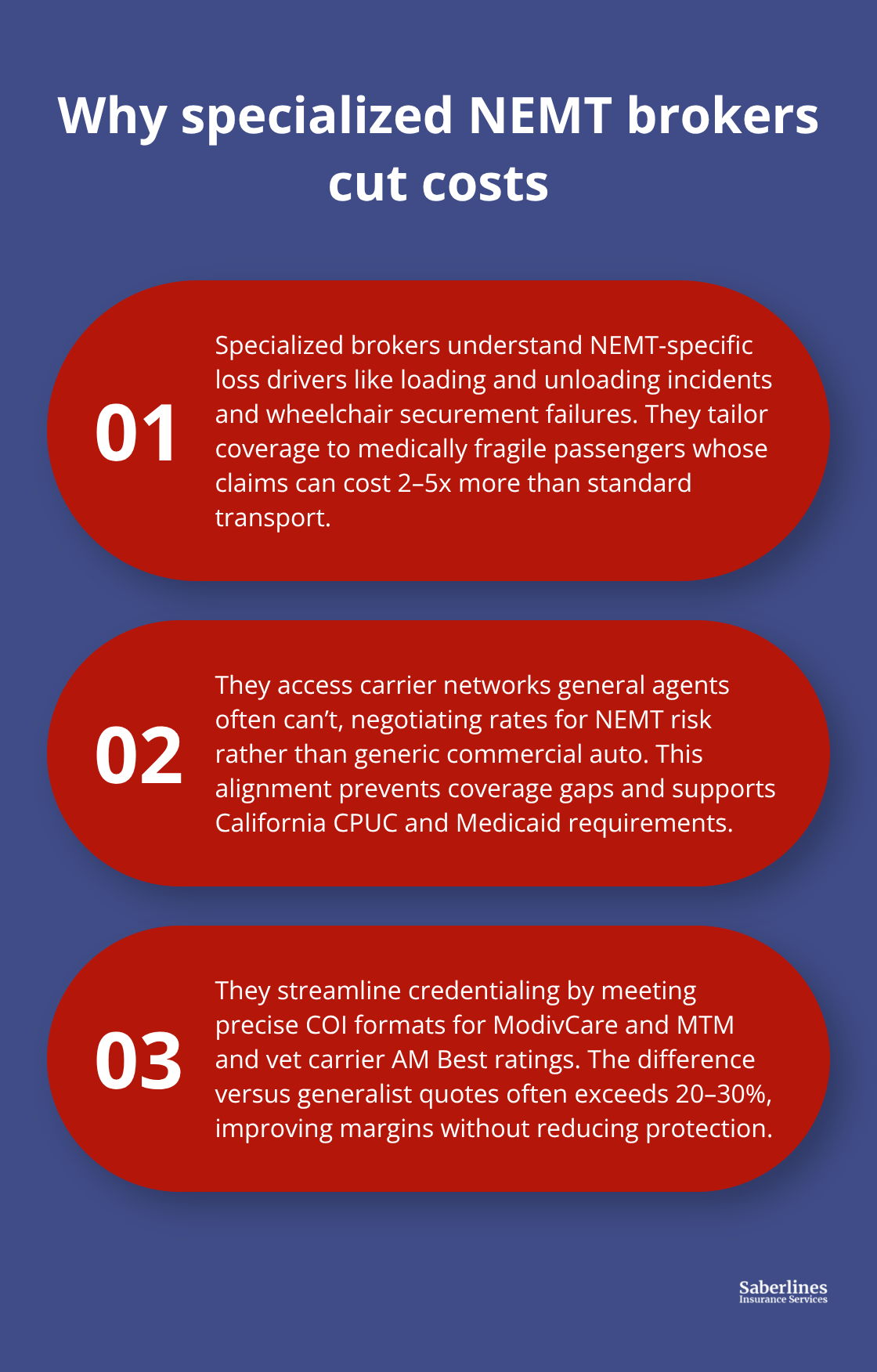

General commercial insurance agents treat NEMT as a standard commercial auto account and quote rates designed for delivery fleets or tow operators. NEMT brokers understand that 40 to 60 percent of claims occur during loading and unloading, that wheelchair securement failures spike claims severity, and that medically fragile passengers drive claim costs 2 to 5 times higher than standard transportation. Specialized brokers access carrier networks that general agents cannot reach and negotiate rates specifically for NEMT risk.

They also understand Medicaid broker contract requirements in California and ensure your certificate of insurance meets the exact format ModivCare, MTM, and other major brokers demand, eliminating credentialing delays. When requesting quotes, obtain at least three to five competing estimates and compare actual coverage limits (verify $1 million per occurrence, not lower limits), SAM riders, loading and unloading endorsements, and carrier AM Best ratings rather than price alone. A broker who can place you with a carrier rated A or better by AM Best and who understands California’s CPUC approval requirements saves you from mid-year cancellations that leave you uninsured and ineligible for Medicaid work. The difference between a generalist quote and a specialized broker quote often exceeds 20 to 30 percent, making this partnership your single largest cost-control lever.

Final Thoughts

Running a compliant NEMT operation in California requires commercial auto liability of at least $1 million per occurrence, workers’ compensation coverage for all employees, and specialized endorsements like loading and unloading protection and Sexual Abuse and Molestation coverage. These elements determine whether you access Medicaid broker contracts, hospital partnerships, and legal operation. Your certificate of insurance must meet exact formatting standards, your drivers need five years of motor vehicle records on file, and your vehicles require current registrations and maintenance documentation.

Proper NEMT insurance California coverage protects your business far beyond legal compliance. A single at-fault accident without adequate coverage can bankrupt a small operator, while medically fragile passengers involved in incidents generate claim costs 2 to 5 times higher than standard transportation claims. Your insurance becomes your defense when loading and unloading incidents occur, when wheelchair securement failures happen, or when a passenger injury claim arrives.

Gather your business documents, vehicle details, driver motor vehicle records, and any existing Medicaid broker contracts, then request quotes from at least three to five specialized NEMT brokers who understand California’s regulatory environment. We at Saberlines Insurance Services have helped California NEMT operators secure compliant coverage, and we understand the specific requirements that Medicaid brokers, hospitals, and regulators demand. Contact us for a quote tailored to your fleet size and service area.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.