NEMT Liability Coverage: Coverage That Protects Patients and Operators

NEMT operators face real liability risks every day, from patient injuries to vehicle accidents. Without proper NEMT liability coverage, a single incident can devastate your business financially and legally.

At Saberlines Insurance Services, we’ve seen too many operators operate without adequate protection. This guide walks you through what you need to know to protect your patients, your team, and your operation.

What NEMT Liability Coverage Actually Protects

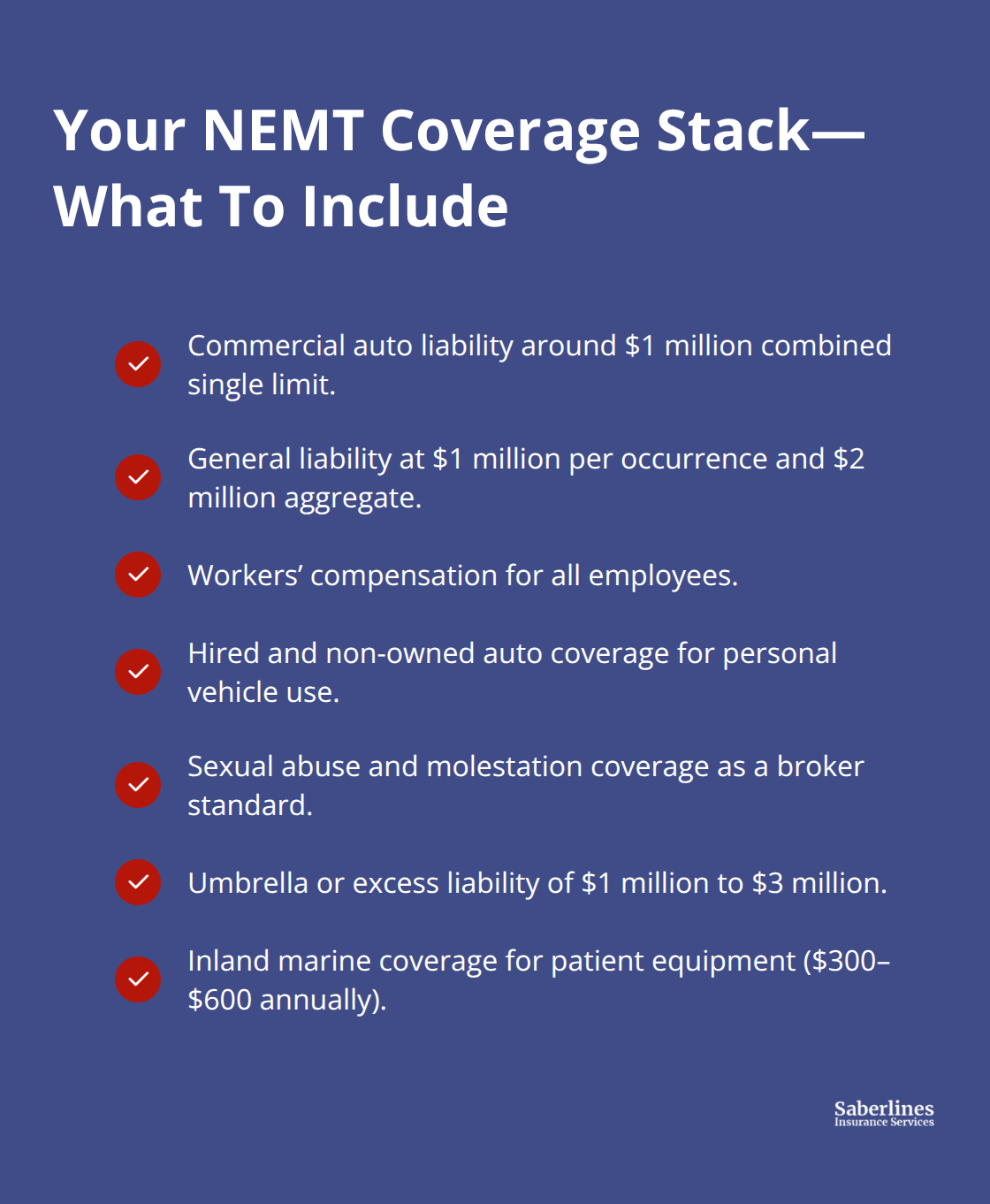

NEMT liability coverage is not a single policy-it’s a coordinated stack of policies designed to cover exposures that standard auto insurance explicitly excludes. When you transport patients on a pre-arranged basis funded by Medicaid or medical providers, you operate in a specialized category that falls outside traditional commercial auto policies. Standard policies won’t cover passenger injuries during medical transport, ADA-related liability from wheelchair handling, or door-through-door patient assistance. Many operators discover this gap mid-claim when their insurer denies coverage. The typical NEMT liability stack includes commercial auto liability around $1 million combined single limit, general liability at $1 million per occurrence and $2 million aggregate, workers’ compensation for employees, hired and non-owned auto coverage for drivers using personal vehicles, and sexual abuse and molestation coverage as a standard broker requirement. This layered approach exists because patient transport liability differs fundamentally from hauling cargo or delivering packages. A single incident-a patient fall during loading, a wheelchair securing failure, or an accident involving multiple passengers-can trigger claims across multiple coverage types simultaneously.

Why Claims in NEMT Cost More Than Standard Auto

Industry data shows that claims severity in NEMT runs 2 to 5 times higher than standard auto claims on average. The loading and unloading phase accounts for 40 to 60 percent of incidents, when patients face the greatest vulnerability. This reality drives both premium costs and coverage requirements across the board. A single patient injury claim can easily exceed $45,000, and serious incidents involving multiple passengers or permanent disability can reach six figures.

One operator in Chicago faced a $45,000 claim from a wheelchair securing incident. Another operator in the Midwest faced a $25,000 slip-and-fall claim that exposed gaps in professional liability protection. These documented incidents shaped how NEMT operators now approach coverage stacking.

Standard Commercial Auto Policies Exclude Medical Transport

Standard commercial auto policies contain explicit exclusions for passenger-for-hire operations, medical transport activities, and door-to-door assistance. Your insurer will deny claims if your policy lacks specific NEMT coverage language. Many operators receive coverage denial letters when they submit claims. The distinction matters legally and financially. Medicaid and Medicare Advantage plans require you to maintain continuous coverage that explicitly covers medical transport. Failure to meet these requirements triggers immediate contract termination and loss of trip assignments. Federal requirements under FMCSA 49 CFR Part 387 set minimum liability limits at $1.5 million for operations transporting 1 to 15 passengers and $5 million for 16 or more passengers when crossing state lines. Intrastate operators may follow state rules, but multi-state routes automatically trigger these federal thresholds.

What Your Contracts Actually Demand

Many brokers and healthcare facility contracts impose stricter requirements than state minimums, sometimes demanding $2 million or higher limits with primary and non-contributory language. These aren’t suggestions-they’re binding contract obligations that affect your ability to operate and receive payment for trips. Saberlines Insurance Services specializes in passenger transportation and helps owner-operators and fleets secure the coverage needed to meet these contract demands while staying compliant.

The Real Cost of Adequate Coverage

NEMT insurance costs roughly $4,000 to $12,000 per vehicle annually for auto liability at $1 million combined single limit. Full coverage bundles including auto liability, general liability, workers’ compensation, and umbrella coverage typically run $5,000 to $15,000 per vehicle per year. Wheelchair-accessible vehicles cost significantly more due to lift mechanisms and securement system risk, with WAV-specific premiums typically 15 to 30 percent higher than standard minivans. New operators without loss history pay 30 to 50 percent premiums above established operators with clean loss runs. These costs feel substantial until you compare them against actual claim exposure. The financial protection these policies provide far outweighs the annual premium investment, especially when a single incident can devastate your operation. Understanding what each coverage layer protects helps you make informed decisions about which limits and deductibles fit your specific operation and risk profile.

What Happens When NEMT Incidents Go Wrong

Patient Injuries Strike During the Highest-Risk Moments

Patient injuries during transport represent the most costly exposure NEMT operators face. A fall during loading, improper wheelchair securing, or inadequate assistance during a transfer results in serious injury claims that exceed $45,000 in a single incident. The loading and unloading phase accounts for 40 to 60 percent of all NEMT claims, making this the highest-risk moment in every trip. One Chicago operator faced a $45,000 claim after a wheelchair securing failure that their standard commercial auto policy explicitly excluded. Another Midwest operator confronted a $25,000 slip-and-fall claim that exposed gaps in professional liability coverage. These incidents occur regularly across the country because patient vulnerability peaks when they transition between vehicles and assistance is most needed.

A patient with mobility limitations, cognitive impairment, or multiple medical conditions carries significantly higher injury risk than standard passengers, which explains why claims severity in NEMT runs 2 to 5 times higher than standard auto claims on average. Your liability exposure extends beyond the patient themselves. Family members who witness incidents file claims, and medical providers who referred the patient may raise liability questions that shift focus to your operation’s procedures and training.

Vehicle Accidents Create Multiple Simultaneous Exposures

Vehicle accidents involving NEMT operations trigger multiple liability exposures at once. A collision that injures passengers, damages third-party property, and disables your vehicle creates claims across auto liability, general liability, and potentially professional liability if patient care was compromised. The complexity multiplies when multiple passengers occupy the vehicle, each with their own injury claims and medical documentation requirements.

Regulatory Violations Carry Severe Financial Penalties

Regulatory violations during transport-such as HIPAA breaches when discussing patient information, billing fraud through falsified trip documentation, or failure to maintain required safety equipment-carry penalties that standard commercial auto policies do not cover. HIPAA violations alone range from $100 to $50,000 per violation, and Medicaid investigations into billing discrepancies result in recoupment demands and contract termination. These compliance exposures demand coverage layers that go far beyond basic vehicle protection.

Coverage Requirements Vary by Payer and Location

Your operation must maintain commercial auto liability with limits that meet federal FMCSA requirements ($1.5 million for 1 to 15 passengers, $5 million for 16 or more passengers on multi-state routes), general liability to cover third-party injuries and property damage, workers’ compensation for employee protection, hired and non-owned auto coverage when drivers use personal vehicles, and sexual abuse and molestation coverage as a standard broker requirement. Medicaid and Medicare Advantage plans require continuous insurance verification tied to state regulations and contract obligations, meaning gaps in coverage immediately disqualify you from receiving trip assignments.

New Operators Face Higher Premiums and Greater Risk

New operators without established loss history pay 30 to 50 percent premium increases above operators with clean loss runs, which creates financial pressure to cut corners-a decision that typically backfires when the first incident occurs. This premium penalty reflects the reality that operators without documented safety records and claims history present higher risk to insurers. Understanding what each coverage layer protects helps you make informed decisions about which limits and deductibles fit your specific operation. The next section examines how to assess your fleet’s unique risk profile and select coverage limits that actually match your exposure.

Matching Coverage to Your Fleet’s Real Exposure

Selecting NEMT liability coverage requires matching your specific fleet characteristics to coverage limits that actually reflect your risk, not chasing the cheapest quote available. Start with your vehicle count and passenger capacity, since these directly drive both your exposure and your premium. A single minivan operating locally within one state faces different federal requirements than a fleet of ten wheelchair-accessible vans crossing state lines. Intrastate operations must meet state minimums, which typically range from $500,000 to $1 million in auto liability, but multi-state routes trigger federal FMCSA requirements of $1.5 million for operations transporting 1 to 15 passengers and $5 million for 16 or more passengers. Your broker contracts and Medicaid enrollment agreements often demand higher limits than these minimums-frequently $2 million or more with primary and non-contributory language-which means your actual required limits depend on your specific payer mix and service agreements, not just state law.

Wheelchair-accessible vehicles present a separate risk calculation because lift mechanisms, securement systems, and higher repair costs push premiums 15 to 30 percent above standard minivans. If you operate WAVs, expect annual auto liability costs around $565 to $1,000 monthly per vehicle versus $350 to $625 monthly for ambulatory minivans. Your driver age and experience also matter significantly. Younger drivers or those with limited commercial driving history can restrict your coverage options entirely, and some carriers impose premium penalties of 20 to 40 percent for drivers under 25. Established operators with three or more years of clean loss history and prior livery experience qualify for discounts around 10 to 15 percent, so documenting your safety record and driver qualifications directly impacts your bottom line.

Deductible Strategy Determines Your Cash Flow Impact

Raising your deductible from $500 to $2,500 or $5,000 typically saves 10 to 20 percent on physical damage premiums, but this only works if you maintain cash reserves to cover the deductible when an incident occurs. Too many operators select high deductibles to lower monthly costs, then face financial strain when they must pay the deductible from operating cash. The right deductible balances your premium savings against the actual cash your operation can absorb without disrupting payroll or vehicle maintenance. Most established NEMT operators with stable cash flow should hold deductibles around $1,000 to $2,500 on physical damage, while maintaining $0 or $500 deductibles on liability coverage since you never want a deductible barrier between you and legal defense.

New operators without established loss history pay 30 to 50 percent premium increases above established operators, which creates financial pressure-but this is exactly when you need the strongest coverage, not the cheapest. Your coverage limits deserve the same discipline. Medicaid funds roughly 60 to 75 percent of trips nationally, and Medicaid enrollment requires proof of continuous insurance coverage that explicitly covers medical transport. A single coverage gap disqualifies you from receiving trip assignments, which means the cost difference between $1 million and $2 million in liability limits becomes irrelevant if inadequate coverage triggers contract termination and forces you out of business entirely.

Vehicle Type and Location Drive Premium Variation

Your specific vehicle configuration and operating location create substantial premium differences that most operators overlook. Ambulatory minivans cost approximately $350 to $625 monthly for auto liability, while WAVs cost approximately $565 to $1,000 monthly due to lift and securement risk. Location affects premiums significantly: rural areas typically cost around $3,500 annually per vehicle, suburban areas around $4,500, and urban areas around $5,500 to $7,500 depending on city size. State variation is large as well-California and Florida tend toward higher premiums due to litigation patterns and no-fault rules, while Texas and Georgia show mid-to-high ranges. No-fault states and high-litigation jurisdictions push premiums higher overall because claims severity increases in these environments.

Building Your Coverage Stack with Specialist Guidance

Working exclusively with carriers and agencies that specialize in NEMT produces better results than working with general commercial auto brokers who treat medical transport as an afterthought. The specialized NEMT carrier market includes fewer than 30 carriers nationwide, and appetite for the class continues shrinking due to high loss ratios and severe claims. This limited market means finding the right carrier requires someone who understands which carriers currently write which states, which ones accept new operators, and which impose the strictest underwriting requirements. A general commercial auto broker will waste your time with carriers that decline NEMT entirely or impose unrealistic underwriting demands.

Your coverage stack must include commercial auto liability around $1 million combined single limit, general liability at $1 million per occurrence and $2 million aggregate, workers’ compensation for all employees, hired and non-owned auto coverage if any driver uses a personal vehicle, sexual abuse and molestation coverage as a broker standard, and umbrella or excess liability of $1 million to $3 million for additional protection. Inland marine coverage for patient equipment like power wheelchairs typically costs $300 to $600 annually and protects against on-hook losses that standard policies exclude.

Maximizing Savings Through Strategic Bundling and Timing

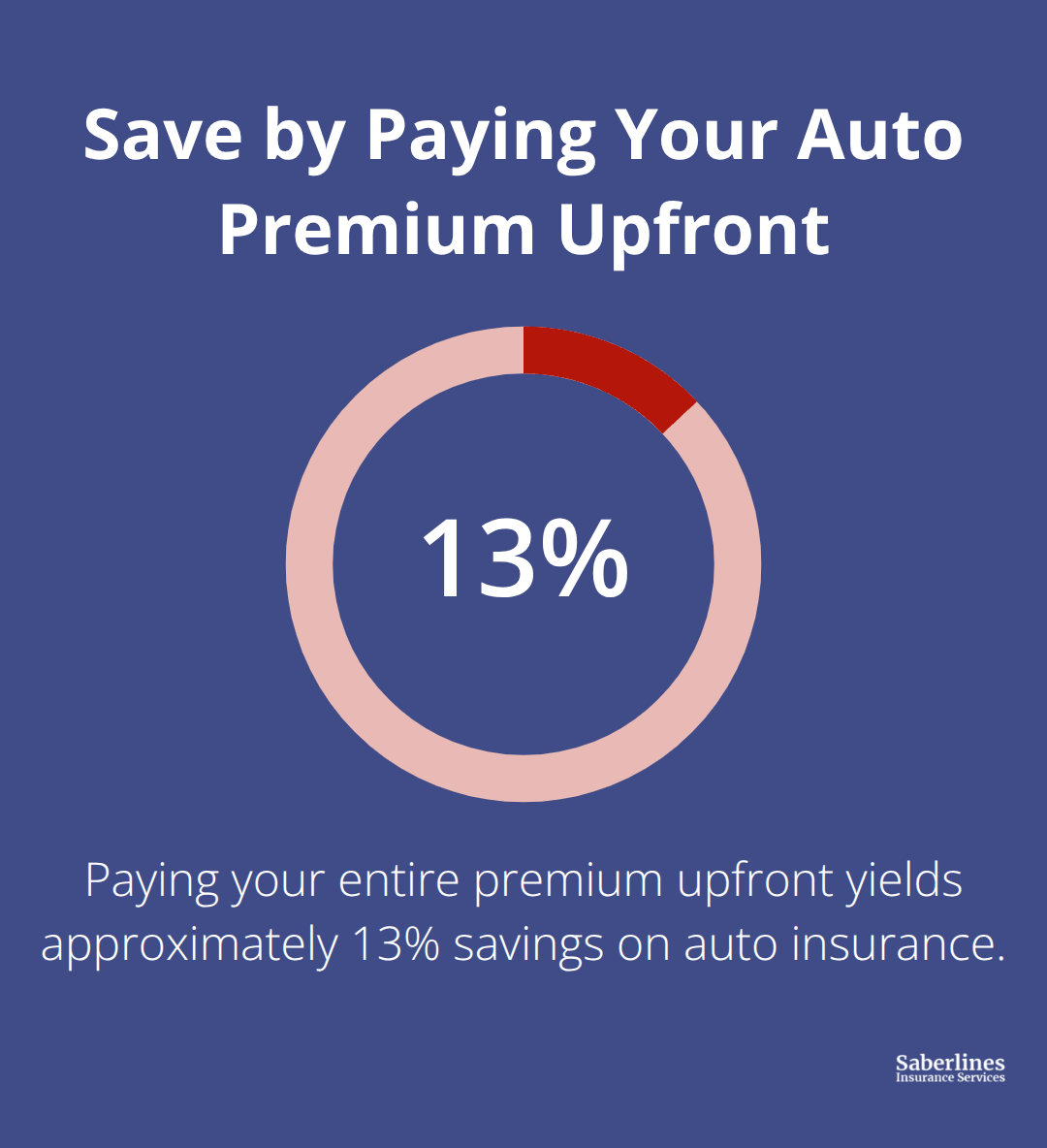

Bundling multiple coverages with a single carrier saves roughly 10 to 20 percent compared to purchasing policies separately, and paying your entire premium upfront yields approximately 13 percent savings on auto insurance. The total annual cost across all coverages averages around $12,000 per vehicle for $1 million in liability, but this varies dramatically by location, vehicle type, driver age, and claims history.

Joining NEMT associations like NEMTAC unlocks group-rate savings of roughly 10 to 20 percent, with membership around $250 annually, though you must verify that group coverage meets your specific broker requirements before binding.

Final Thoughts

NEMT liability coverage protects your operation from the financial devastation that a single patient injury, vehicle accident, or regulatory violation can cause. Standard commercial auto policies explicitly exclude medical transport, which means operating without proper NEMT liability coverage leaves you exposed to claims your insurer will deny when you need protection most. Adequate coverage is an investment in your business survival, not an expense to minimize.

Your next step requires gathering your fleet details, driver information, and current loss history, then contacting a specialist who understands NEMT insurance. General commercial auto brokers waste your time because they lack the expertise to navigate the specialized carrier market or understand which policies actually cover medical transport. You need someone who knows which carriers currently write your state, which ones accept new operators, and how to structure your coverage stack to meet both federal requirements and your specific broker contracts.

We at Saberlines Insurance Services specialize in passenger transportation and help owner-operators and fleets secure the coverage needed to operate compliantly and protect your patients and team. Start a quote with us or contact our team by phone for guidance on structuring your coverage stack that matches your real exposure.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.