General Liability for Shuttles: Protecting Passenger Transport Services

Shuttle operators face real liability exposure every single day. From passenger injuries to property damage claims, the risks are substantial and often underestimated.

General liability for shuttles isn’t optional-it’s the foundation of responsible business operations. We at Saberlines Insurance Services help shuttle companies understand exactly what they need to protect themselves and their passengers.

Coverage Gaps That Put Shuttle Operators at Risk

Bodily Injury Claims From Passenger Accidents

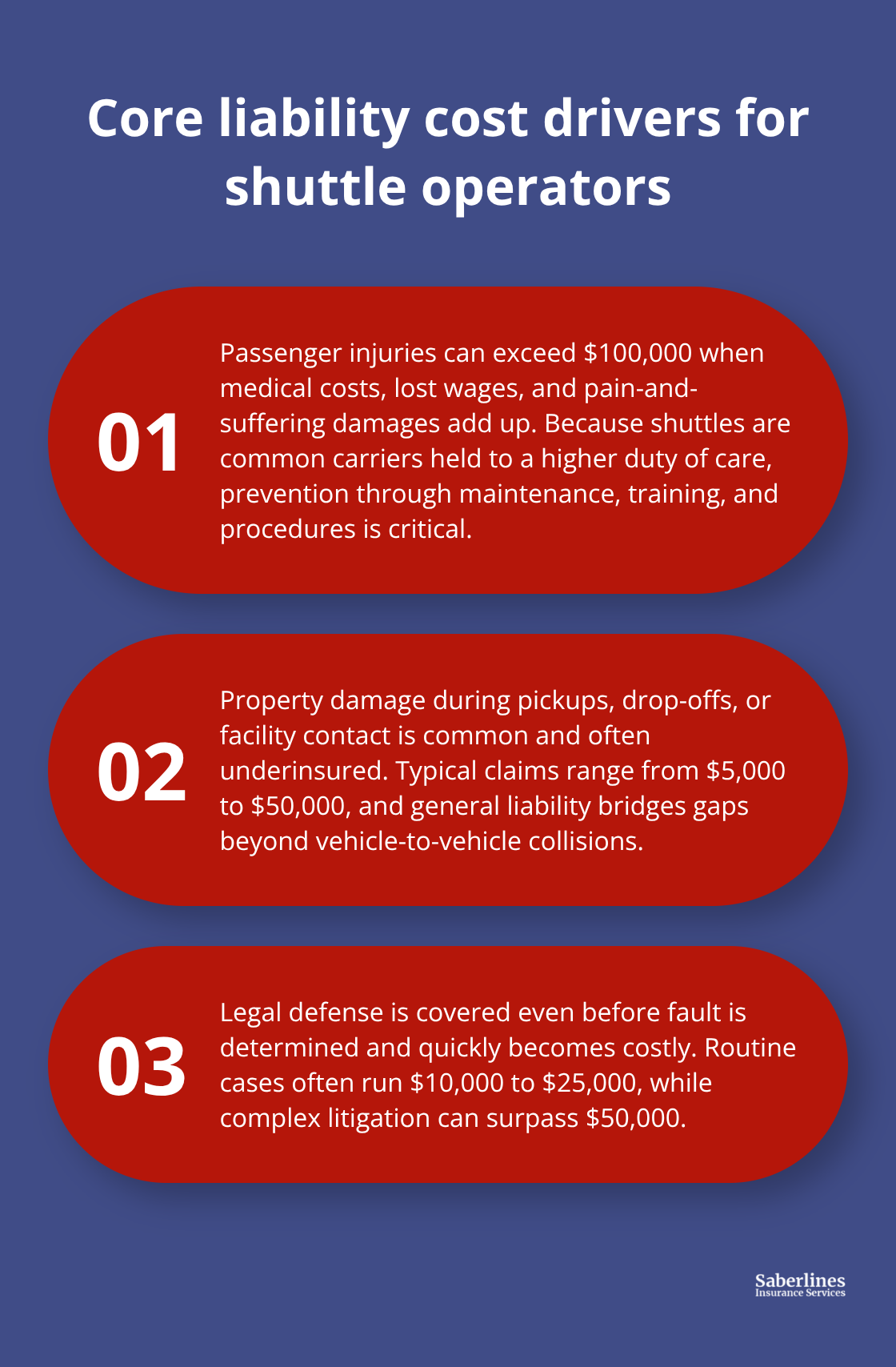

Passenger injuries during transport represent the most expensive liability exposure shuttle operators face. A single bodily injury claim from a passenger injured during boarding, transit, or disembarking can exceed $100,000 when medical expenses, lost wages, and pain-and-suffering damages combine. Common carriers like shuttles are held to a higher standard of care than ordinary businesses, meaning courts expect you to prevent foreseeable injuries through proper maintenance, driver training, and safety procedures.

If a passenger slips on a wet floor, falls during sudden braking, or sustains injuries from defective seating, your general liability policy must cover the medical expenses, legal defense, and judgment costs. Without adequate coverage limits, a single incident can drain your operating capital and force you to shut down.

Property Damage Liability During Transport Operations

Property damage claims arise frequently but often go unaddressed in inadequate policies. When your shuttle damages a client’s facility during pickup or drop-off, strikes a parked vehicle, or causes structural damage to a building, the property owner will pursue compensation. These claims typically range from $5,000 to $50,000 depending on the damage severity.

Shuttle operators often assume their commercial auto policy covers property damage-it does not. General liability fills this gap by protecting against third-party property claims that fall outside vehicle-to-vehicle collisions. This distinction matters because your auto policy focuses on vehicle-related incidents, while general liability addresses broader operational exposures.

Third-Party Claims and Legal Defense Costs

Third-party claims and legal defense costs create the hidden expense that surprises unprepared operators. When a passenger’s family member files a claim, a vendor sues over a scheduling dispute, or a pedestrian claims injury near your shuttle stop, your insurer covers your legal defense even before determining fault. Legal defense costs alone can reach $10,000 to $25,000 for a straightforward case, and complex litigation quickly exceeds $50,000.

The Global Passenger Transportation Insurance market, valued at USD 52.4 billion in 2025, reflects the scale of liability exposure across the industry. Regulatory compliance adds another layer of risk: if your shuttle violates safety regulations and a passenger is injured, the injured party can cite regulatory violations to strengthen their negligence claim. Court judgments increasingly favor passengers in cases where operators failed to follow industry safety standards or warn passengers of dangerous conditions.

Coverage limits matter significantly here-a $1 million per-occurrence limit protects you against most standard claims, but shuttle operations with multiple daily trips and high passenger volumes should consider higher limits like $2 million. The right coverage structure depends on your specific routes, passenger volume, and operational complexity, which is why selecting the appropriate policy requires careful assessment of your actual risk profile.

What General Liability Actually Covers for Shuttle Services

Passenger Injuries and Medical Expenses

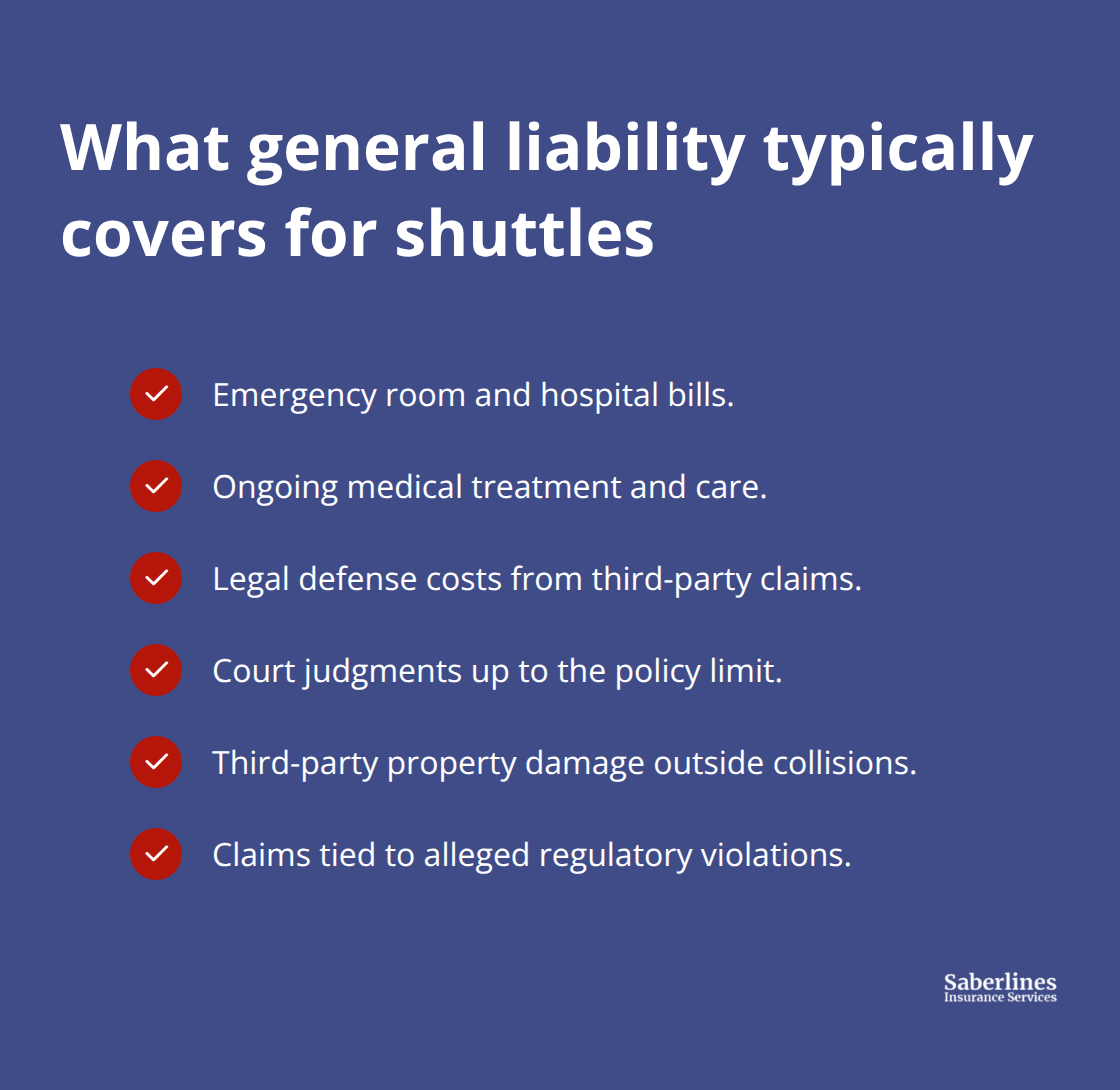

Passenger injuries during transport trigger your general liability coverage immediately. When a passenger slips on boarding stairs, sustains injury from sudden braking, or experiences a medical emergency during transit, your policy activates to cover medical treatment costs. Your general liability policy pays for emergency room visits, hospital stays, and ongoing care related to the incident-often without requiring proof that you caused the injury. Medical expense coverage within transportation general liability protects passengers and third parties regardless of fault in many cases, which accelerates claim resolution and passenger care. A single emergency room visit costs $3,000 to $15,000 before any legal action occurs, making this coverage essential for protecting both your passengers and your business finances.

Property Damage Beyond Vehicle Contact

Property damage claims arise when your shuttle operations cause damage outside of vehicle-to-vehicle collisions. Your shuttle strikes a building during drop-off, damages client facility infrastructure while passengers load, or causes structural damage near a business entrance. These claims typically range from $5,000 to $50,000 and fall completely outside your commercial auto coverage. Many shuttle operators mistakenly assume their auto policy covers all property damage-it does not. General liability fills this critical gap by protecting against third-party property claims that your auto policy explicitly excludes. This distinction separates vehicle-related incidents (handled by auto insurance) from broader operational exposures (handled by general liability).

Regulatory Compliance and Court Judgments

Common carriers like shuttles face a higher legal standard than ordinary businesses. Courts expect you to maintain vehicles properly, train drivers rigorously, and warn passengers of dangerous conditions. When passengers sue and cite safety regulation violations, your general liability policy covers both the court judgment and your legal defense costs. Legal defense expenses commonly reach $10,000 to $25,000 for routine cases and exceed $50,000 for complex litigation. If you fail to meet heightened safety standards and a passenger wins a judgment, your policy covers the award amount up to your selected limit. The Global Passenger Transportation Insurance market reached USD 52.4 billion in 2025, reflecting the substantial liability exposure shuttle operators manage daily.

Selecting Coverage Limits for Your Operation

Coverage limits directly affect your protection level and should match your operational complexity. A minimum of $1 million per-occurrence limit handles most standard passenger injury claims for smaller shuttle operations. Shuttle operations running multiple daily trips with high passenger volumes should seriously consider $2 million limits instead. Your specific operational risks-routes, passenger volume, and regulatory environment-determine the right coverage structure. Operators with charter services, medical transport, or high-value passenger loads face elevated exposure that demands higher limits. The right policy structure protects your business while keeping premiums manageable, which is why assessing your actual risk profile before selecting limits and deductibles matters significantly.

Moving Forward With Coverage Assessment

Your general liability policy protects against the three liability exposures that threaten shuttle operations most: passenger injuries, property damage, and regulatory violations. Understanding what your policy covers prevents costly gaps when claims arise. The next step involves evaluating your specific operational risks and comparing policies that match your shuttle business model.

How to Choose the Right General Liability Policy for Your Shuttle Business

Map Your Operational Exposure First

Selecting general liability coverage requires moving past generic policy comparisons and focusing on what actually matters for your shuttle business. Start by mapping your specific operational exposure rather than defaulting to standard coverage limits. If you run airport shuttles with hourly passenger turnover, your injury exposure differs dramatically from a charter service with fewer daily trips or a medical transport operation serving non-emergency patients. Document your average daily passenger count, typical trip duration, routes through high-traffic or high-risk areas, and whether you handle any cargo alongside passengers. This operational snapshot becomes your foundation for determining appropriate coverage limits. Many shuttle operators purchase $1 million per-occurrence limits because that number sounds standard, but your actual needs depend entirely on your risk profile.

A shuttle running 40 passenger trips daily across urban routes faces far higher exposure than one operating 8 charter trips weekly on highway corridors. The Global Passenger Transportation Insurance market shows that operators with clearly defined risk profiles secure better rates than those purchasing generic coverage, because insurers can accurately price the actual exposure.

Balance Coverage Limits Against Premium Costs

Coverage limits and deductibles directly impact both your premium costs and your financial exposure after a claim. In 2025, the median monthly general liability premium for new Progressive customers was $55, with average rates reaching $79 per month, but shuttle operations typically pay substantially more due to passenger injury exposure. Lowering your deductible from $1,000 to $500 increases premiums noticeably, while raising it to $2,500 or $5,000 reduces costs significantly. However, this trade-off matters operationally: a $5,000 deductible means you cover the first $5,000 of every claim from your operating cash, which becomes problematic if you face multiple claims in a single year. For shuttle operations, a $1,000 deductible balances manageable premium costs against reasonable out-of-pocket exposure. Coverage limit selection requires honest assessment of your maximum potential loss. A single catastrophic passenger injury claim can reach $200,000 to $500,000 when medical costs, lost wages, pain and suffering, and legal judgments combine. If your operation generates $500,000 in annual revenue, a $1 million limit provides meaningful protection without excessive premium burden. Higher-volume operations or those serving vulnerable populations like medical transport patients should seriously consider $2 million limits despite the premium increase.

Assess Insurer Experience With Transportation Risks

Your insurer’s experience with shuttle operations determines how smoothly claims get handled and whether coverage gaps emerge when you need protection most. National Indemnity, a Berkshire Hathaway subsidiary with an A++XV rating from A.M. Best, maintains deep expertise in transportation general liability and specializes in both standard market and surplus line shuttle risks. Their track record since 1940 demonstrates stability through economic cycles and changing regulatory environments. When evaluating insurers, ask directly about their experience with your specific shuttle category: airport shuttles, charter services, medical transport, or party buses all present different risk profiles. Request references from other shuttle operators they insure and ask about claims handling speed, coverage interpretation disputes, and premium stability over multiple renewal periods. Avoid insurers that treat shuttle operations as generic commercial liability risks; transportation-focused carriers understand common carrier liability standards and regulatory compliance requirements that standard insurers frequently misinterpret. Your broker or agent should maintain relationships with multiple carriers experienced in transportation to ensure competitive quotes and appropriate coverage placement, rather than defaulting to whichever insurer offers the lowest initial premium.

Final Thoughts

General liability for shuttles protects your business from passenger injuries, property damage, and regulatory violations that threaten your operation’s survival. A single claim can exceed your annual operating budget and force you to shut down, which is why adequate coverage matters more than cost savings. The higher legal standard applied to common carriers means courts expect rigorous safety practices, driver training, and passenger protection-and your insurance must reflect that elevated responsibility.

Securing coverage starts with honest assessment of your operational risks, including daily passenger volume, typical routes, trip frequency, and whether you handle cargo alongside passengers. Contact an agency experienced in transportation insurance to obtain quotes from carriers that understand shuttle operations rather than treating them as generic commercial liability. We at Saberlines Insurance Services specialize in passenger transportation coverage and can help you navigate your specific coverage needs.

Once you secure coverage, review your policy annually as your operation changes-adding routes, increasing passenger volume, or expanding services all shift your liability exposure. Implement driver safety programs, maintain detailed vehicle maintenance records, and establish clear boarding and loading procedures to reduce incident frequency. These practices lower your claims history, which directly reduces future premiums and protects the passengers who depend on your shuttle service.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.