General Liability for Fleets: Strategies to Protect Multi-Vehicle Operations

Running a fleet means managing multiple vehicles, multiple drivers, and multiple liability exposures. One accident involving any vehicle in your operation can trigger claims that threaten your business finances and reputation.

General liability for fleets is your first line of defense against third-party lawsuits. At Saberlines Insurance Services, we’ve seen how the right coverage strategy separates fleet operators who recover quickly from incidents versus those who face crippling legal costs.

What General Liability Actually Covers

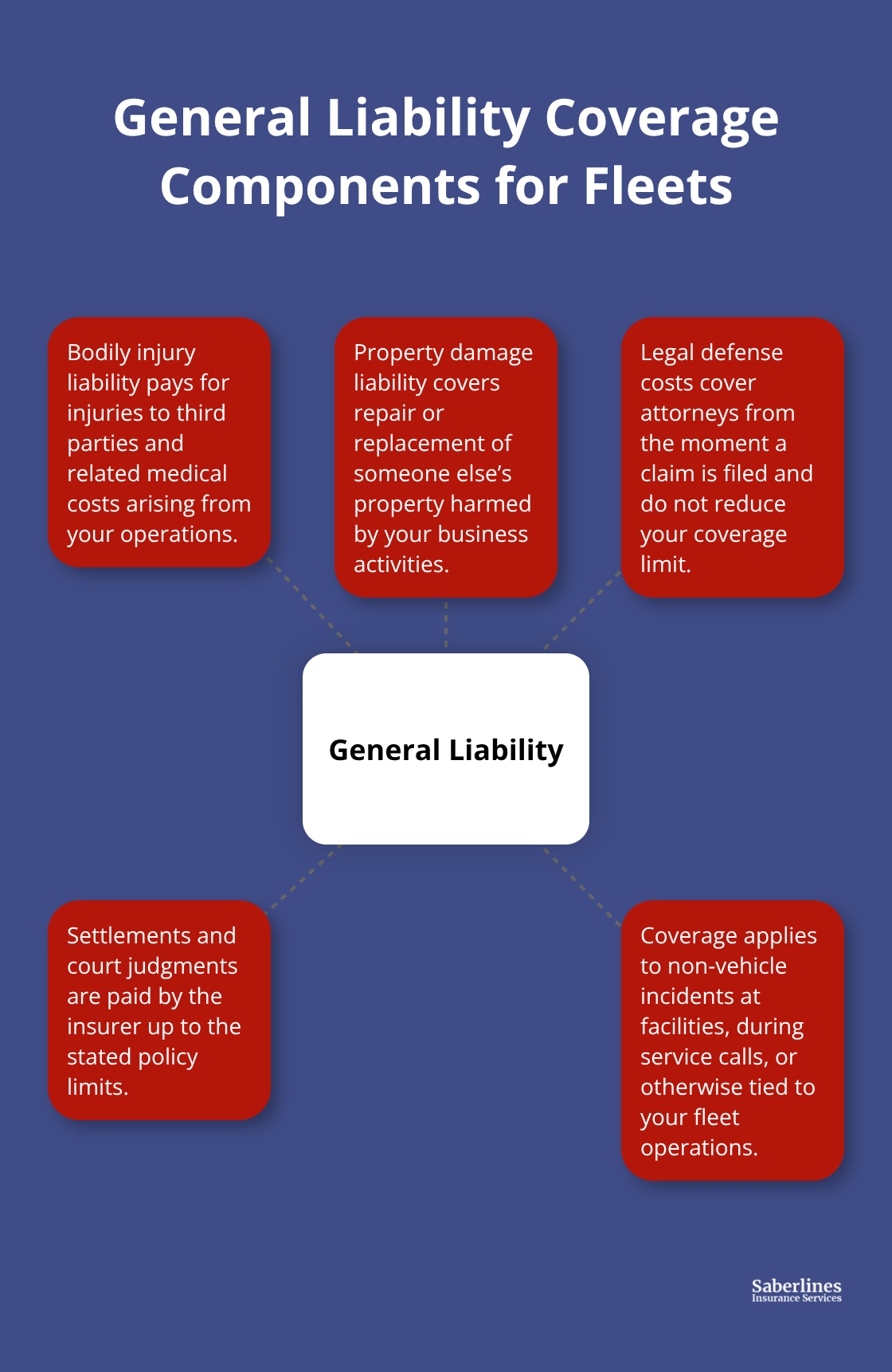

General liability for fleets protects your business when a third party claims bodily injury or property damage caused by your operations. This differs from auto liability, which covers accidents involving your vehicles. General liability applies when someone is hurt or property is damaged at your facility, during service calls, or as a result of non-vehicle incidents tied to your fleet business. If a customer is injured while visiting your dispatch office, or if your equipment damages a client’s property during a service delivery, general liability covers medical expenses, repair costs, and legal fees. The coverage typically includes bodily injury liability (which pays for injuries to third parties) and property damage liability (which covers damage to someone else’s property). It also includes legal defense costs-the insurer pays attorneys to defend you in court, plus settlement or judgment amounts if you lose a case. Nuclear verdicts in commercial transportation have exceeded $10 million in recent years, making adequate limits non-negotiable for any fleet operation.

Bodily Injury Claims and Your Fleet Exposure

Bodily injury claims arise when someone claims your fleet operation caused them physical harm. A pedestrian struck near your facility, an employee of a client injured during your service, or a visitor harmed by equipment or conditions at your location can all trigger these claims. General liability covers medical bills, rehabilitation costs, lost wages, and pain-and-suffering awards up to your policy limit. The injury must stem from your business operations, not a vehicle accident, which falls under commercial auto liability instead. Your policy limit matters significantly; carriers often recommend minimum limits of $300,000 to $1,000,000 per occurrence for fleets, depending on industry and size. Underinsurance creates real risk-if a claim exceeds your limit, you pay the difference out of pocket.

Property Damage Liability and Legal Defense

Property damage liability covers harm your fleet operation causes to someone else’s property. Your driver negligently damages a loading dock while delivering cargo, or your equipment causes structural harm-general liability pays repair or replacement costs. Legal defense costs are built into the policy and activate immediately when a claim is filed, even before fault is determined. Insurers assign counsel to defend you, and those legal fees do not reduce your coverage limit. Settlement expenses and court judgments also come from your policy, up to the stated limit. For multi-vehicle fleets operating across multiple locations, property damage exposure grows with every facility and service touchpoint.

Why Coverage Limits Matter for Multi-Location Operations

Fleets with multiple service locations face compounded exposure across facilities, equipment, and client interactions. A single incident at one location can trigger claims that test your coverage limits. Adequate limits protect your entire operation from financial strain when third-party claims arrive. The next section examines how to assess your specific fleet risks and select coverage limits that match your actual exposure.

How to Reduce Fleet Liability Through Proactive Risk Management

Risk reduction starts with measurable driver behavior, not intentions. Fleets that invest in structured safety programs recover faster from incidents and negotiate better insurance terms. The FMCSA reported over 900,000 roadside inspection violations in 2024, many tied to driver qualification gaps and maintenance failures-problems that compound liability exposure when claims arise.

Driver Training and Documented Safety Programs

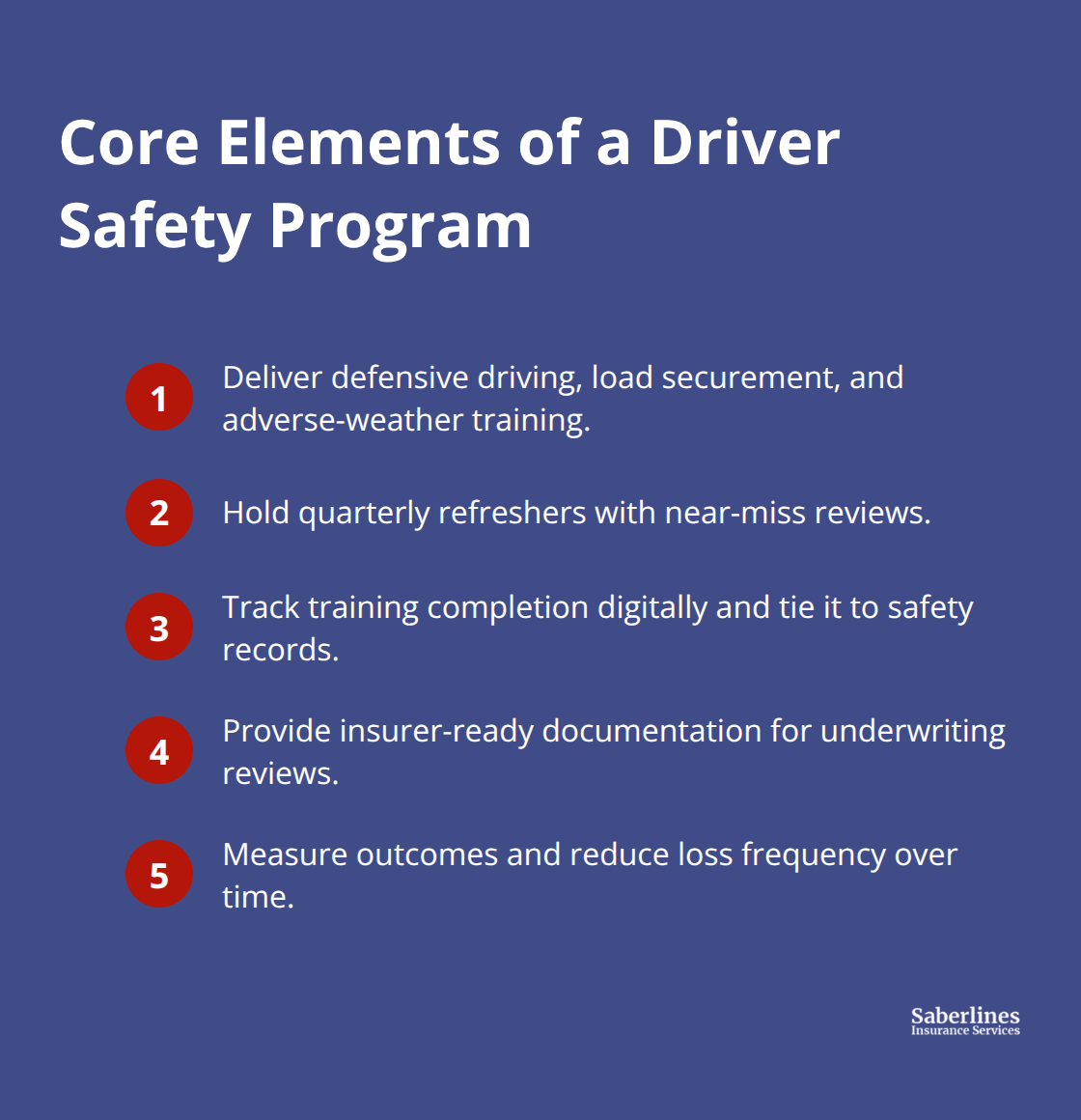

A documented driver training program addresses defensive driving, load securement, and adverse-weather response, with quarterly refresher sessions that include near-miss discussions. Track training completion digitally and link it to your safety record; insurers recognize this documentation and factor it into underwriting decisions. Structured driver training correlates with measurable declines in loss frequency and repair expenses.

Establish clear written safety policies that define acceptable vehicle operation, mobile-device usage limits, seat-belt enforcement, and disciplinary escalation. Assign owners to each policy element and enforce them consistently across all locations-inconsistent enforcement signals weak risk management to insurers and creates liability gaps in litigation. Digital maintenance logs and telematics data demonstrate ongoing compliance; use them to track speed, braking patterns, and idling behavior.

Coaching and Behavioral Accountability

Share specific coaching clips with drivers tied to exact road conditions and their performance, which accelerates behavior change far more effectively than generic feedback. A regular coaching cadence of 15–20 minutes daily review sustains safety improvements and builds the documentation insurers trust when underwriting renewals. This approach connects drivers directly to the data that shapes their risk profile and creates measurable accountability.

Preventive Maintenance and Digital Inspection Records

Vehicle maintenance failures drive both liability and claims costs. Develop a preventive maintenance schedule covering oil changes, brake inspections, tire rotations, and fluid checks, then log all services digitally with completion dates and technician names. Maintenance diligence directly affects your risk class and renewal pricing.

Conduct regular vehicle inspections using digital DVIRs that capture defect details with photos and timestamps; retain records for at least 90 days at the fleet level and route defects automatically to repairs for faster resolution. This standardized workflow prevents the pencil-whipping that creates audit vulnerabilities. Multi-location operations require centralized recordkeeping so compliance status remains visible in real time across all facilities.

Video Evidence and Claims Defense

Video telematics eliminates fraudulent claims and accelerates legitimate settlements. Lansberry Trucking deployed driver-facing cameras and documented a dramatic reduction in claims losses, demonstrating how video evidence strengthens your position in disputes. Accountability systems work best when they connect drivers, dispatchers, and maintenance teams through a single data hub.

Build dashboards that surface failed inspections, overdue maintenance, and recurring defects immediately, rather than waiting for monthly reports. When a pattern emerges-say, brake defects on three vehicles in the same fleet-assign an owner with a deadline to investigate root cause and implement corrective action. Track these closure timelines and use them to demonstrate continuous improvement to your insurer.

This proactive posture shifts the liability narrative from reactive damage control to systematic risk prevention. The next section examines how to select coverage limits and policy structures that align with your fleet’s actual exposure and operational footprint.

Selecting Coverage Limits That Match Your Fleet’s Real Exposure

Assess Your Fleet Size and Operating Footprint

Choosing the right general liability limit requires honest accounting of your fleet size, geographic footprint, and the industries you serve. A five-vehicle local delivery fleet operating within a single state faces fundamentally different exposure than a twenty-vehicle operation spanning multiple states with service contracts in high-density urban markets. The baseline recommendation across the industry is a minimum of $300,000 per occurrence for small fleets, but that floor rises sharply once you operate across state lines or serve industries with higher injury frequency. Geotab research shows that couriers and taxi services pay higher premiums due to strict time pressures and elevated driving risk, which translates directly to greater bodily injury exposure and higher claim potential.

Determine Your Coverage Floor Based on Industry Risk

If your operation touches any high-risk vertical, your coverage floor should start at $500,000 per occurrence and climb to $1,000,000 or higher if you have multiple service locations or high-value client interactions. The cost difference between a $300,000 limit and a $1,000,000 limit is rarely the barrier people imagine; what matters is whether your limit actually covers the realistic worst-case scenario in your market. A single nuclear verdict in commercial transportation has exceeded $10 million, but even mid-sized claims routinely settle in the $500,000 to $2,000,000 range once medical expenses, legal fees, and pain-and-suffering awards accumulate. Underestimating your limit forces you to cover the gap yourself, which erases any premium savings instantly.

Account for Operational Hazards and Regulatory Complexity

Your coverage must also account for the specific hazards embedded in your operations. A fleet delivering to construction sites faces property damage exposure at client facilities that a courier service does not encounter. A fleet operating in California must account for California’s emissions standards and regulatory complexity, which elevates both operational risk and litigation exposure if non-compliance surfaces during a claim investigation. Multi-state operations introduce compounded regulatory risk; FMCSA reported over 900,000 roadside inspection violations in 2024, many tied to documentation and driver qualification gaps that plaintiffs’ attorneys weaponize in liability cases to argue negligence.

Review Policy Exclusions and Coverage Coordination

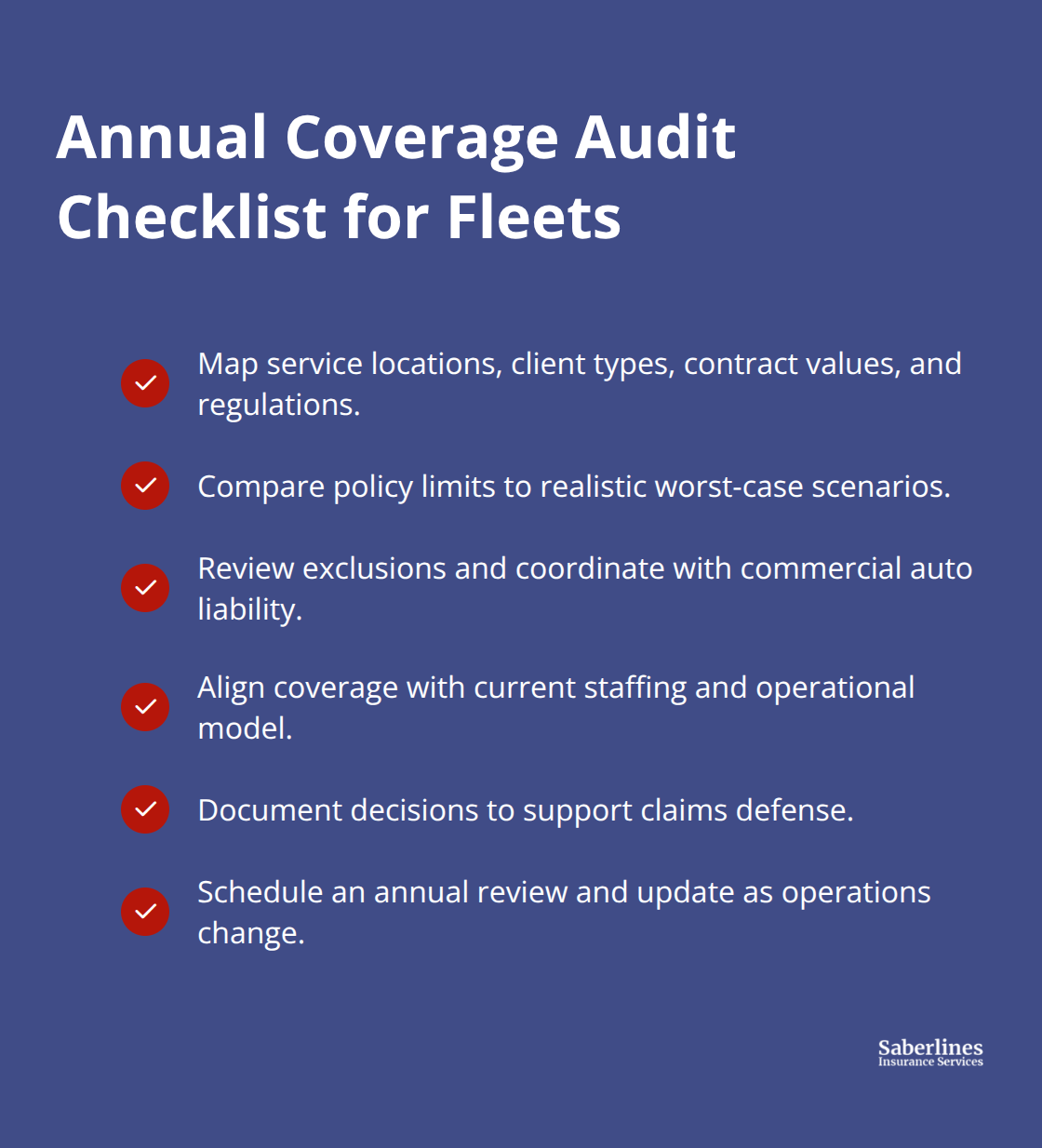

Review your policy exclusions carefully because general liability policies often exclude coverage for damage caused by your vehicles, which forces you to rely on commercial auto liability instead-a critical distinction that creates coverage gaps if you don’t coordinate both policies correctly. Your liability coverage must align with your staffing model, especially if employees use personal vehicles for business purposes. This coordination prevents expensive surprises when a claim arrives and coverage questions emerge.

Conduct an Annual Coverage Audit

An annual coverage audit maps your actual service locations, client types, contract values, and regional regulations against your policy limits and exclusions. This audit should track whether your coverage aligns with your current operations and staffing structure. The audit becomes your defense documentation if a claim arrives; it demonstrates that you selected limits based on deliberate risk assessment, not guesswork.

Final Thoughts

General liability for fleets protects your business when third-party claims arrive, but coverage alone does not prevent incidents or control costs. The real protection comes from combining adequate limits with measurable risk reduction across driver behavior, maintenance, and compliance. Fleets that document safety programs, maintain digital inspection records, and deploy video evidence recover faster from claims and negotiate better renewal terms with insurers.

Your coverage limits must match your actual operational footprint-a five-vehicle local operation needs different protection than a multi-state fleet serving high-risk industries. Annual audits ensure your policy aligns with your current service locations, client contracts, and regulatory environment. Without this alignment, you risk underinsurance that forces you to cover claim gaps yourself, erasing any premium savings instantly.

Conduct an honest assessment of your fleet’s exposure and map your service locations, identify your highest-risk operations, and calculate realistic worst-case scenarios in your market. Then compare those scenarios against your current coverage limits and exclusions. Contact Saberlines Insurance Services to review your current policy, identify coverage gaps, and build a protection strategy that matches your fleet’s real exposure and growth plans.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.