Construction Contractor Liability Insurance: How to Shield Your Projects

One accident on your job site can cost thousands in medical bills, legal fees, and property repairs. Construction contractor liability insurance protects your business from these financial disasters.

At Saberlines Insurance Services, we’ve seen contractors lose everything because they underestimated their exposure. The right coverage keeps your projects moving forward without the constant worry of catastrophic claims.

What Your Liability Coverage Actually Protects

Bodily Injury Coverage Shields You from Medical and Legal Claims

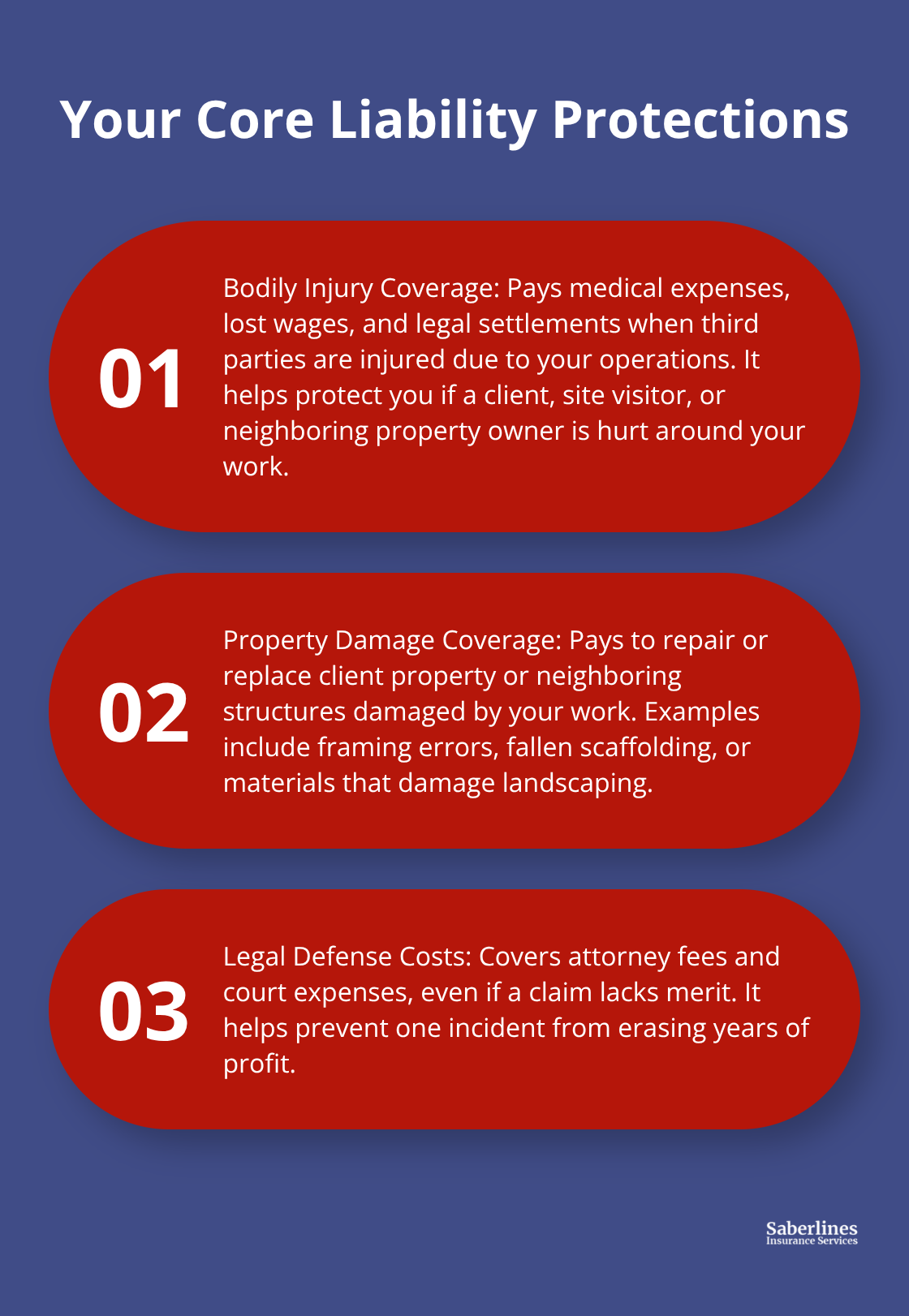

Construction contractor liability insurance covers three essential areas that protect your business from financial collapse when things go wrong on site. First, bodily injury coverage pays medical expenses, lost wages, and legal settlements when someone sustains an injury during your work-whether that’s a client, a site visitor, or a neighboring property owner. If a worker from another trade trips over your equipment and breaks their leg, your policy covers their medical bills and any lawsuit they file. According to the National Safety Council, construction remains the most dangerous industry by fatality rate, making this protection non-negotiable for any contractor operating on active job sites.

Property Damage Coverage Protects Structures and Assets

Second, property damage coverage pays for repairs or replacement when your work damages client property or neighboring buildings. A framing error that cracks a foundation, scaffolding that falls into an adjacent structure, or materials that damage a client’s landscaping all fall under this protection. Property damage claims often run $50,000 to $150,000 depending on what structure or asset your work damaged. Without this coverage, you absorb these costs directly from your operating budget.

Legal Defense Costs Keep Your Business Solvent

Third, your policy covers legal defense costs and court expenses, which means your insurer pays attorneys and court fees even if a claim lacks merit. Legal defense alone can cost $25,000 to $75,000 before a case settles or goes to trial. A single bodily injury claim can exceed $100,000 when medical costs, legal fees, and settlement damages combine. One incident without adequate coverage wipes out years of profit.

Why Liability Insurance Is Now a Business Requirement

Most construction contracts now require proof of liability insurance before you step on a job site, so carrying adequate coverage isn’t optional-it’s a business requirement that protects both you and your clients from catastrophic financial exposure. These three coverage types work together to keep your business solvent when claims arise. Understanding what each component covers helps you assess whether your current limits match your actual project risks and contract requirements.

Common Liability Risks in Construction Projects

On-Site Accidents Drain Your Budget Immediately

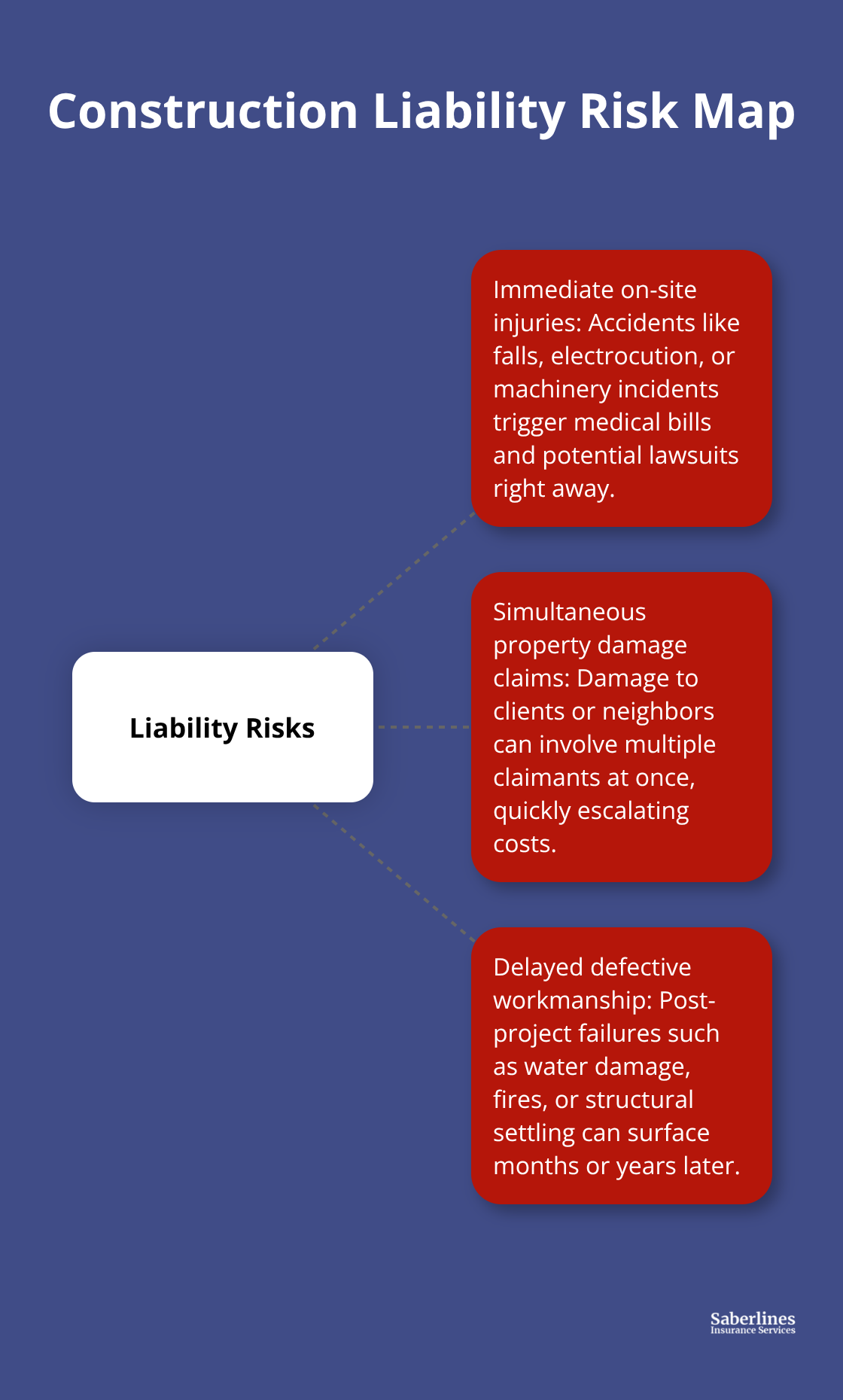

On-site accidents cause the fastest drain on contractor finances because medical bills arrive immediately while your project stalls. A worker from another trade sustains a serious injury on your site-a fall from scaffolding, electrocution near your equipment, or a crushing injury from machinery you operate-and suddenly you face $50,000 to $200,000 in liability exposure before any lawsuit materializes. The National Safety Council identifies construction as the most dangerous industry by fatality rate, which means injury claims happen more frequently in this sector than almost any other. Your liability insurance covers these medical expenses, wage replacement, and legal defense costs the moment a claim gets filed. Without coverage, you write checks from your operating account while your crew sits idle waiting for the project to restart.

Property Damage Claims Hit Multiple Parties at Once

Property damage claims move even faster because they affect multiple parties simultaneously. Damage to a client’s existing structure, neighboring buildings, or adjacent property triggers claims from the property owner, their insurance company, and their tenants all at once. A framing error that cracks a foundation wall, scaffolding that punctures a roof, or materials that damage landscaping and underground utilities all generate claims exceeding $100,000. The Insurance Information Institute reports that social inflation-larger jury awards and higher settlement demands-added roughly $30 billion in additional commercial auto liability claims between 2012 and 2021, and this same pressure affects general construction claims.

Defective Workmanship Claims Arrive Months or Years Later

Defective workmanship claims arrive months or years after you leave the site, which is why completed operations coverage matters separately from standard general liability. A plumbing installation that causes water damage six months later, electrical work that fails and starts a fire, or structural work that settles unevenly and cracks walls all generate post-project claims your standard policy may exclude. These claims cost $75,000 to $300,000 depending on the scope of damage and the number of affected properties. The longer the timeline between your work and the claim, the harder it becomes to defend your workmanship because evidence deteriorates and witnesses disappear. Completed operations coverage protects you from these hidden exposures that surface long after project completion.

Why Standard Policies Leave You Exposed

Standard general liability policies often exclude post-project defect claims entirely, leaving a significant gap in your protection. This gap means you absorb the full cost of water damage, electrical failures, or structural settling that occurs after you’ve moved to the next job. Contractors who carry only basic general liability discover this exclusion too late-when a claim arrives and their insurer denies coverage. Adding completed operations as a separate endorsement closes this gap and protects your business from the defects that emerge when you’re no longer on site.

Understanding these three risk categories-immediate on-site injuries, simultaneous property damage claims, and delayed defect claims-reveals why your coverage must address all three exposure types. Each risk type demands different protection, and each can bankrupt a contractor operating without adequate limits.

Matching Coverage Limits to Your Actual Project Exposure

Set Limits Based on Project Value, Not Industry Averages

Your project type and contract requirements should drive your coverage limits, not industry averages or your competitor’s policy. A residential remodel generating $500,000 in annual revenue demands different limits than a commercial build worth $5 million. Most contractors operate with general liability limits of $1 million per occurrence and $2 million aggregate, which costs roughly $69 per month for a $1 million single limit according to Hartford data. However, this baseline fails contractors taking on larger projects or specialized work. Commercial general contractors frequently face contract requirements demanding $2 million per occurrence limits, which increase premiums by 25 to 40 percent depending on your loss history and trade classification.

Match Property Damage Limits to Your Actual Exposure

Property damage exposure matters more than bodily injury for some trades. Plumbers and electricians face substantial post-project water damage and electrical fire claims that exceed typical medical cost exposures. Completed operations coverage should match your maximum project value, not your annual revenue, because a single defect claim can exceed your annual profit. If you install roofing systems worth $300,000 and water damage emerges two years later affecting three properties, your claim exposure reaches $500,000 to $750,000 in repairs and legal defense.

Evaluate Deductible Trade-Offs Carefully

Standard deductibles range from $1,000 to $5,000, and jumping to a $5,000 deductible saves roughly 10 to 15 percent on premiums while shifting more risk to your business. This trade-off makes sense only if your operating margin covers unexpected claims without halting operations.

Add Endorsements Your Contracts Require

Your contract stack determines which endorsements become non-negotiable rather than optional. Additional insured endorsements appear in nearly every commercial contract, and carriers charge $50 to $150 annually to add each additional insured to your policy. General contractors routinely require subcontractors to name them as additional insured, which means your policy pays defense costs and damages if their client sues your GC. Subcontractor liability exclusions can strip coverage for claims arising from subcontractor work, leaving you exposed on projects where you hire trades to complete portions of the scope.

Hired and non-owned auto coverage costs $200 to $400 annually and covers liability when you rent equipment or when employees drive their personal vehicles on project business. Most contractors skip this until a claim arrives and their policy excludes coverage because the vehicle wasn’t disclosed. Pollution coverage for environmental exposures like mold remediation or asbestos removal runs $500 to $1,500 annually but becomes mandatory if your work touches contaminated sites or involves environmental cleanup.

Protect Against Design and Employment Risks

Contractors’ professional liability or errors and omissions coverage protects you if you contribute to project designs or plans, even without employing architects. This coverage costs $1,500 to $3,500 annually for mid-sized contractors but defends you against design-related claims that general liability excludes. Employment practices liability coverage protecting against harassment and discrimination claims runs $800 to $2,000 annually and matters more as your crew grows beyond five employees.

Final Thoughts

Construction contractor liability insurance protects your business from the financial devastation that arrives when claims hit your projects. The coverage you carry determines whether a single incident becomes a manageable loss or destroys years of profit, which is why matching your limits to your actual project exposure matters far more than accepting whatever your competitor carries. Your contract stack reveals which endorsements your clients demand, and additional insured requirements appear in nearly every commercial agreement you’ll sign.

Your next move is to gather your contracts and identify the specific coverage gaps your clients require, then contact Saberlines Insurance Services to discuss your project risks and get quotes from multiple carriers. Premium differences for identical coverage often exceed 40 percent depending on your loss history and trade classification, so accepting the first offer leaves money on the table. Work with an agent who understands construction risk rather than treating your business like any other commercial account.

The contractors who build sustainable operations treat liability insurance as a strategic asset that enables growth on larger projects rather than a cost to minimize. Your coverage protects your projects, your crew, and your clients from catastrophic financial exposure when accidents or defects occur. Start your quote process today to ensure the right protection stands between your business and the next claim that arrives.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.