Why Commercial Fleet Insurance Options Matter for Small Truck Fleets

Small truck fleet owners face a constant balancing act between keeping costs down and protecting their business from financial disaster. One accident, one cargo loss, or one compliance violation can wipe out months of profit.

At Saberlines Insurance Services, we’ve seen firsthand how the right commercial fleet insurance options can be the difference between a thriving operation and a struggling one. This guide walks you through the coverage types you actually need, the real costs of falling short, and how to find a provider that gets your business.

What Coverage Do Small Truck Fleets Actually Need

Commercial Auto Liability: Your Foundation

Commercial auto insurance forms the foundation of any fleet operation, but it’s not one-size-fits-all. For small truck fleets, liability coverage typically starts at state minimums-often $25,000 to $50,000 per accident-but that’s dangerously low. Most freight brokers and shippers demand $1 million in liability limits before they’ll contract with you, according to industry standards in trucking operations. If you haul goods or run regular delivery routes, carrying only state minimums leaves you exposed to lawsuits that can exceed your assets.

Physical Damage: Protecting Your Vehicles

Physical damage coverage matters just as much as liability. Collision coverage pays for damage from crashes, while comprehensive covers theft, vandalism, weather, and other non-collision events. For a small fleet with vehicles worth $15,000 to $40,000 each, one major accident without physical damage coverage forces you to replace equipment out of pocket, draining cash flow for months.

The real decision isn’t whether to carry physical damage-it’s choosing the right deductible. A $2,500 deductible typically costs 15–25% less per year than a $500 deductible, but only if your fleet can absorb that out-of-pocket hit after a claim.

Cargo Insurance: Protecting Your Freight

Cargo insurance deserves serious attention if you transport freight. Motor truck cargo coverage protects the goods in your vehicle from damage, theft, or loss during transit. Rates typically run $500 to $1,500 annually depending on cargo value and routes, but a single cargo loss without coverage can cost thousands. If you haul high-value goods like electronics or pharmaceuticals, cargo insurance is non-negotiable. For occasional shipments, per-shipment cargo policies offer flexibility without locking you into annual contracts.

The Real Price of Underinsurance

Underinsurance hits harder than you’d expect. A delivery fleet in California operating with minimal liability limits faced an $850,000 judgment after a serious accident; the insurer covered only $100,000, leaving the owner personally liable for the difference. That owner’s business didn’t survive. CDC data show that more than one-third of long-haul truck drivers experience a serious crash during their careers, which means the odds aren’t in your favor. Small fleets operating in dense urban areas or high-traffic corridors face even higher accident frequencies.

The cost of being underinsured extends beyond the immediate claim: lost revenue while vehicles sit out of service, increased insurance premiums after claims, reputational damage, and potential loss of customer contracts.

Building Your Coverage Stack

The strongest approach combines commercial auto liability at $1 million minimum, physical damage with a deductible matched to your cash reserves, and cargo insurance if you transport goods. Additional endorsements fill critical gaps. Non-trucking liability covers you when you use a vehicle for personal purposes, preventing a gap between commercial and personal coverage. Trailer interchange covers you when hauling non-owned trailers, essential if you lease equipment from other operators.

For fleets growing beyond five vehicles, average annual costs range from $1,200 to $2,400 per vehicle depending on location, vehicle type, and driver history. A five-vehicle fleet in a mid-cost region typically runs $6,000 to $10,000 annually. Shopping across multiple insurers is essential-quotes for identical fleets can differ by thousands. An insurer with deep trucking expertise understands the specific risks small fleets face and can tailor coverage to your actual operations rather than generic industry templates. Once you’ve mapped your coverage needs, the next step is finding a provider that delivers both competitive pricing and the service quality your operation demands.

What Happens When Your Fleet Isn’t Properly Covered

The Immediate Financial Shock

One accident exposes the gap between what you think you’re covered for and what actually happens when a claim lands on your desk. A small delivery fleet operating with state-minimum liability limits of $50,000 faced an $850,000 judgment after a serious accident; the insurer covered only $100,000, leaving the owner personally liable for the remaining $750,000. That business did not survive the judgment. CDC data show that more than one-third of long-haul truck drivers experience a serious crash during their careers, which means your fleet faces real risk. When underinsurance meets reality, the financial consequences ripple across every aspect of your operation.

The uncovered portion of the judgment hits first, but the damage extends further. Your personal assets become vulnerable to creditors, lenders demand repayment of business loans, and your ability to secure future financing evaporates. A single uncovered claim can wipe out years of accumulated profit and leave you personally responsible for amounts that exceed your net worth.

Legal and Compliance Consequences

State regulators suspend your operating authority if you fail to maintain adequate coverage, which means your trucks sit idle while you scramble to find new insurance. Compliance violations carry fines ranging from $300 to $10,000 per violation depending on your state and the severity of the lapse, and repeat offenses result in license suspension.

These penalties compound quickly. A lapsed coverage period of even a few days can trigger multiple violations, each carrying separate fines. Once regulators flag your operation, they scrutinize future filings more closely, making it harder to maintain clean compliance records.

Operational Disruption and Revenue Loss

Underinsurance creates operational chaos that extends far beyond the initial claim. While vehicles sit in the shop after an accident, you lose the revenue those trucks would have generated, forcing you to subcontract work to competitors or turn down shipments entirely. A single week of downtime for a five-vehicle delivery fleet costs approximately $2,000 to $5,000 in lost revenue, depending on your market and typical job value.

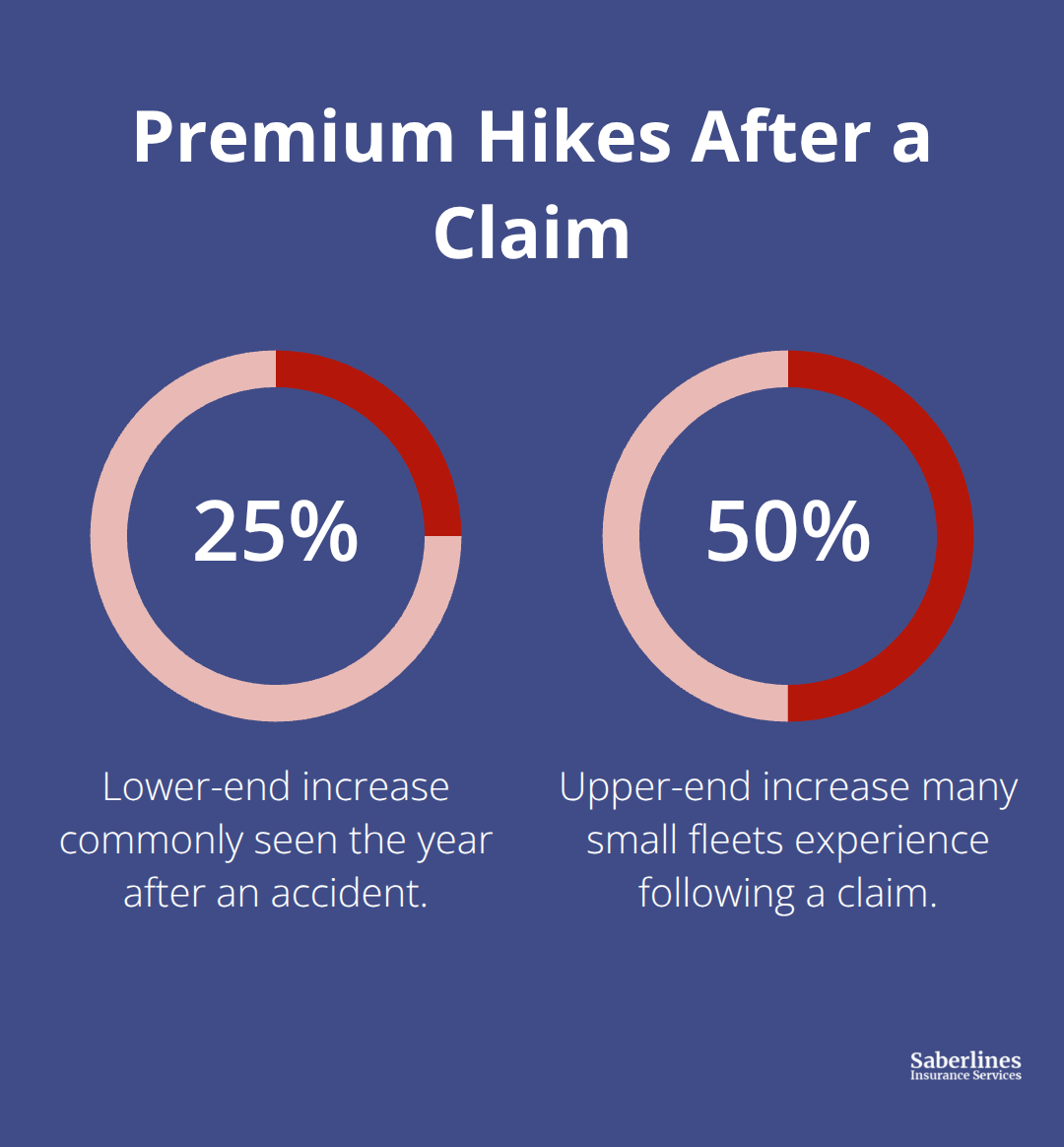

Insurance premiums skyrocket after claims, with increases of 25% to 50% common in the year following an accident. Customers who learn about compliance violations or serious accidents often terminate contracts, and rebuilding that reputation takes months or years. The operational damage from a single uncovered incident can take longer to repair than the financial damage.

The Cost of Proper Coverage

Commercial auto liability at $1 million minimum, physical damage with a deductible matched to your cash reserves, and cargo insurance if you transport goods creates a protective barrier that keeps your business operating when accidents happen. The annual cost for this protection on a five-vehicle fleet typically ranges from $6,000 to $20,000 depending on location, vehicle type, and driver history, but that investment looks trivial compared to the cost of a single uncovered claim.

Shopping across multiple insurers reveals dramatic price differences for identical coverage; quotes for the same five-vehicle fleet can vary by $5,000 or more annually. This variation makes comparison essential before committing to any policy, and working with an insurer that understands trucking operations helps you identify which coverage options actually matter for your specific routes and cargo types.

Picking an Insurer That Actually Understands Your Fleet

Why Insurer Expertise Matters More Than You Think

Finding the right insurance provider matters far more than most fleet owners realize. The difference between a generic carrier and one with deep trucking expertise shows up in premium quotes, coverage options, and how claims get handled when your truck sits in a ditch at 2 AM. According to JD Power’s 2025 U.S. Small Commercial Insurance Study, 55% of small commercial insurance customers say they will definitely renew with their current insurer, down 6 percentage points from 2024. That drop signals rising frustration as premiums climb without clear explanation.

The real problem isn’t just price-it’s that most general commercial insurers don’t understand the specific risks small truck fleets face. An insurer with actual trucking knowledge recognizes that a delivery fleet operating in Los Angeles carries different risks than one running rural routes in Montana. They understand DOT compliance requirements, cargo exposure, and driver safety patterns in ways that generic carriers simply don’t.

How Industry Knowledge Affects Your Rates and Loyalty

When you work with an insurer that demonstrates understanding of your business or industry, renewal intent improves by 37 points year-over-year, according to JD Power. For fleets, this means choosing a carrier with transportation expertise directly translates to better rates and stronger loyalty. Saberlines Insurance Services specializes in trucking and passenger transportation, combining deep industry expertise with fast quotes and access to preferred and hard-to-place risks. That focus matters when you build a coverage strategy that fits your actual operations rather than industry templates.

Compare Quotes Across Multiple Carriers

Comparing quotes across multiple insurers reveals how dramatically pricing varies for identical coverage. Quotes for the same five-vehicle fleet can differ by $5,000 or more annually, which makes shopping non-negotiable before you sign anything. Request quotes from at least three carriers, and provide identical information about your fleet composition, driver history, routes, and cargo types so comparisons stay meaningful.

Look beyond the premium number-evaluate how each insurer explains rate increases and whether they fully answer your questions about coverage gaps. Customers who understand why their premiums changed report the same satisfaction levels as those receiving no increase (around 722 out of 1,000 according to JD Power). Equally important is assessing how easily you can manage your policy online and resolve problems through digital channels. The ability to handle policy updates, file claims, or access documents entirely on an insurer’s website improves renewal intent by 23 points.

Prioritize Flexibility and Customization

This matters because your time is expensive; a provider with robust self-service tools keeps you operational without constant phone calls. When you evaluate candidates, prioritize carriers that offer flexibility in endorsements and deductibles tailored to your specific operation. A provider willing to adjust coverage limits, add non-trucking liability or trailer interchange endorsements, or customize deductibles to match your cash reserves shows they treat your fleet as a unique operation rather than a standard account number.

Final Thoughts

The right commercial fleet insurance options protect far more than your vehicles-they protect your business, your personal assets, and your ability to operate when accidents happen. Underinsurance creates cascading problems: uncovered claims drain cash flow, compliance violations suspend your operating authority, and lost revenue from downtime compounds the damage. Proper coverage at $1 million liability minimum, physical damage matched to your vehicle values, and cargo insurance if you transport goods costs between $1,200 and $2,400 per vehicle annually, but that investment pales against the cost of a single uncovered incident.

Your choice of insurance provider matters just as much as the coverage itself. An insurer with genuine trucking expertise understands the specific risks your fleet faces and tailors coverage to your actual operations rather than generic templates. When you work with a carrier that demonstrates industry knowledge, your renewal intent improves significantly, and you gain access to better rates and more flexible endorsements that fit your operation.

The next step is straightforward: review your current coverage limits, compare quotes across multiple carriers, and identify any gaps between what you carry and what you actually need. Request quotes from at least three insurers using identical fleet information so comparisons stay meaningful. Contact Saberlines Insurance Services to discuss your fleet’s specific coverage needs and get a quote that reflects your actual operations rather than industry assumptions.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.