NEMT fleet insurance Essentials for Fleet Managers

NEMT fleet managers face a constant challenge: finding the right insurance coverage without overpaying or leaving gaps that could cost thousands. The wrong policy can leave your operation exposed to liability claims, passenger injuries, and vehicle damage that insurance won’t cover.

At Saberlines Insurance Services, we’ve seen too many NEMT fleets operate with inadequate protection. This guide walks you through the coverage types you actually need, the gaps most fleets miss, and how to choose a provider that understands your business.

What Coverage Actually Protects Your NEMT Fleet

Commercial Auto Liability: The Foundation

Commercial auto liability is non-negotiable for NEMT operations, but the limits matter far more than most fleet managers realize. Federal regulations require a minimum of $1.5 million in coverage for interstate for-profit carriers transporting 1 to 15 passengers, yet most state Medicaid programs and medical transport brokers like ModivCare, MTM, and MAS demand $1 million per occurrence as a baseline. In practice, many MCO contracts push requirements higher to $2 million per occurrence because of the severity of claims involving medically vulnerable passengers. A single at-fault accident involving a fall or medical emergency can trigger damage awards well beyond $500,000, making the difference between $1 million and $2 million coverage genuinely consequential.

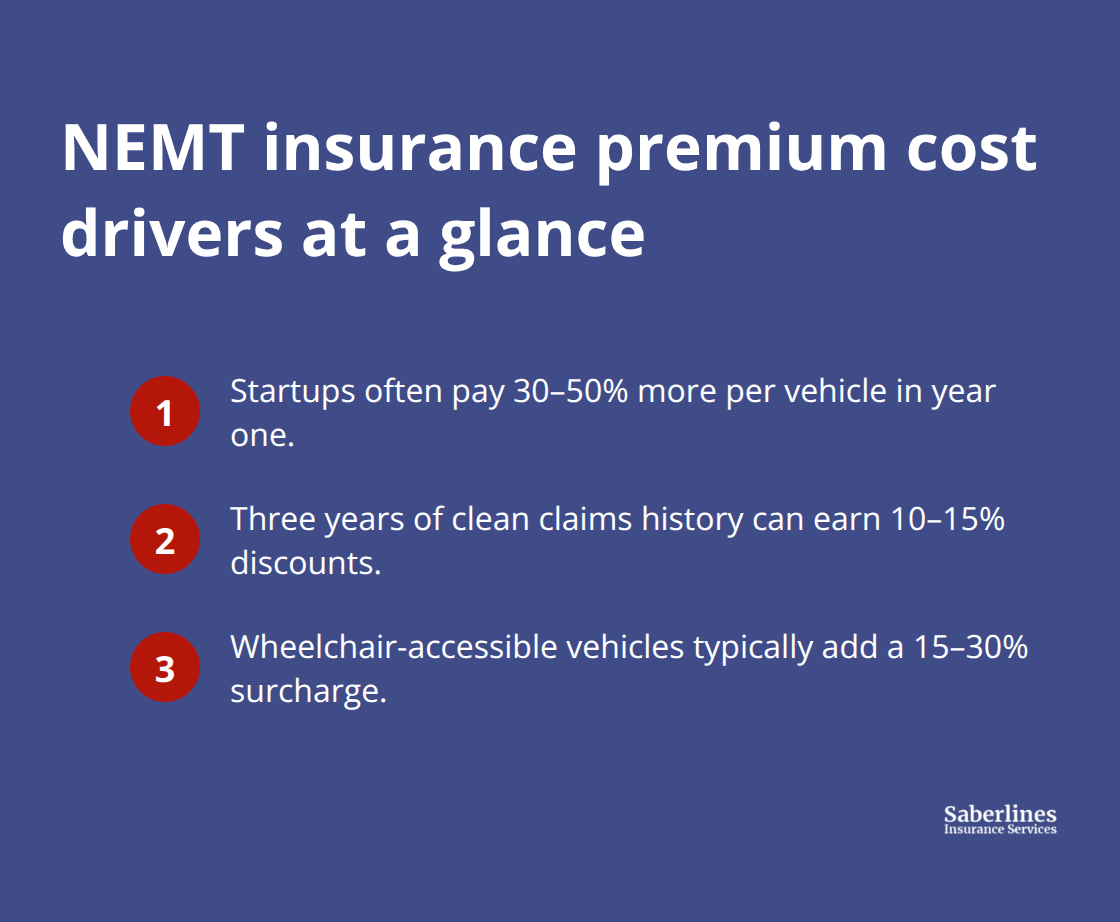

Cost varies dramatically based on your operation’s age and vehicle type. Startups pay 30 to 50 percent more per vehicle in their first year due to lack of loss history, so a new sedan-based operation might face $4,200 to $7,500 annually for basic coverage. An established fleet with three years of clean claims history accesses discounts of 10 to 15 percent. Wheelchair-accessible vehicles carry a 15 to 30 percent surcharge because lift failures and securement problems drive higher litigation costs.

Workers’ Compensation and State Requirements

Workers’ compensation is mandatory in every state and covers employee injuries on the job, with costs varying significantly by state and driver classification. A driver earning $45,000 annually might cost $1,500 to $3,000 per year in workers’ comp premiums depending on jurisdiction. This coverage is non-negotiable for compliance with state labor laws and Medicaid enrollment requirements.

General Liability: The Overlooked Protection

General liability covers third-party bodily injury and property damage claims that fall outside vehicle accidents-loading and unloading injuries, sidewalk falls near your facility, or damage to a patient’s home during transport. Most NEMT brokers require $1 million per occurrence and $2 million aggregate, and this coverage typically costs $400 to $800 annually as an add-on to your auto policy. Many fleet managers mistakenly assume auto liability handles all exposure, but a patient who trips while exiting your vehicle at their home and files a premises liability claim would fall under general liability, not auto.

Medical Payments Coverage: Where Fleets Underinsure

Medical payments coverage or passenger injury protection is where many fleets underinsure themselves. Standard limits often cap at $5,000 per person, which barely covers emergency room costs for a fractured hip in a medically fragile population. You should evaluate your actual medical costs in your region and try for at least $10,000 to $25,000 per person, especially if you transport bariatric or stretcher patients who face higher injury severity.

Total Cost and Compliance Impact

A three-vehicle fleet with comprehensive coverage including $2 million auto liability, $1 million/$2 million general liability, workers’ compensation, and enhanced medical payments typically runs $5,000 to $15,000 annually per vehicle, or roughly $15,000 to $45,000 for the fleet. This investment directly protects your business from the financial devastation of a single serious claim and keeps you compliant with Medicaid and broker mandates. Understanding these coverage layers positions you to identify gaps before they become expensive problems-which brings us to the coverage gaps that catch most NEMT fleets off guard.

Where NEMT Fleets Actually Face Coverage Shortfalls

Most NEMT fleet managers discover their coverage gaps only after a claim lands on their desk. The policies they bought looked adequate on paper, but real-world scenarios expose serious vulnerabilities. Passenger liability limits sit too low for the actual medical costs your population faces. Physical damage coverage caps out before repair bills arrive. And scenarios that don’t fit neatly into standard auto or general liability slip through unprotected. This pattern repeats across the industry, and the financial damage is preventable.

The Passenger Injury Reality Check

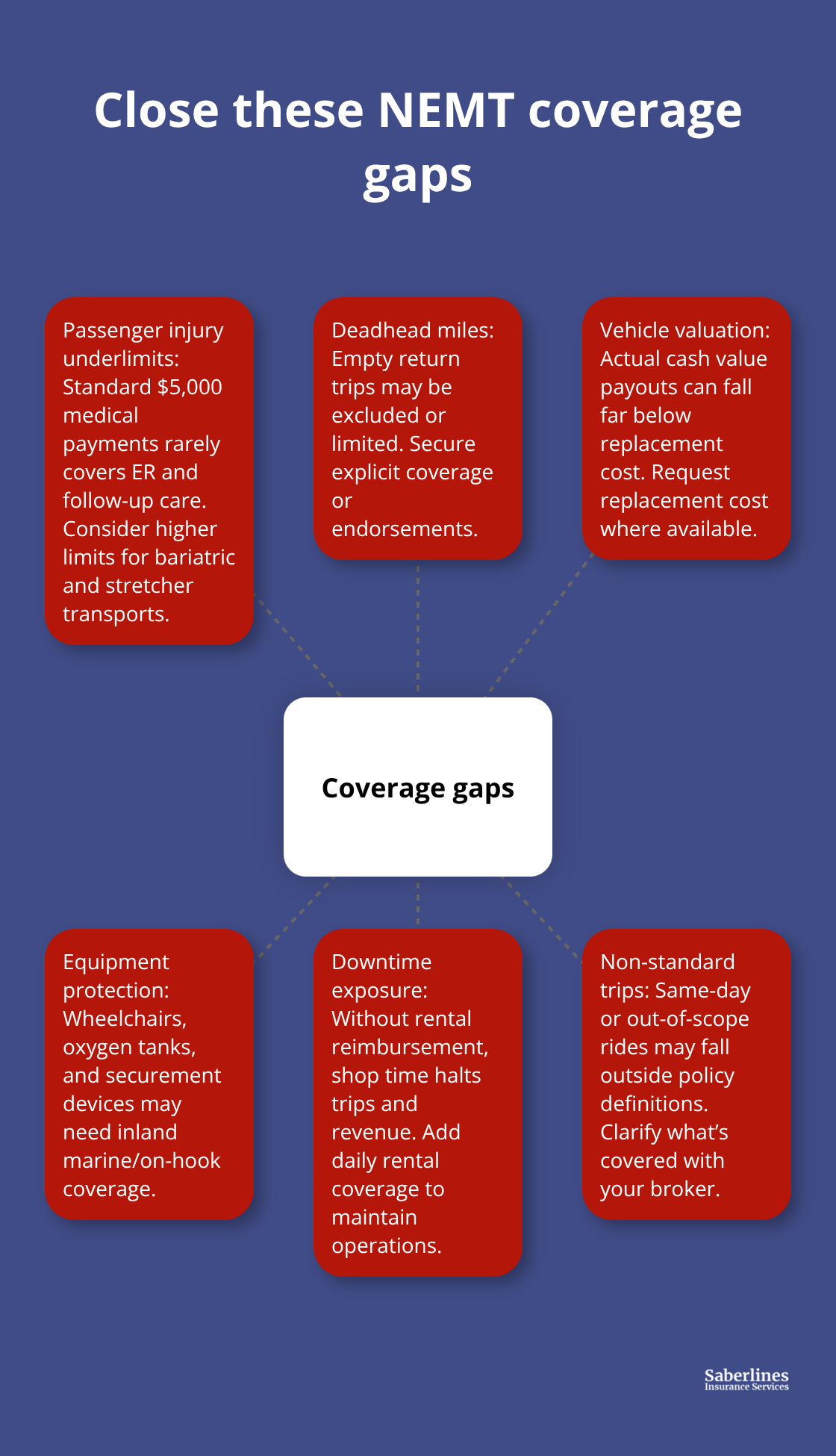

Passenger injury claims in NEMT operations run higher than most fleet managers expect because your passengers are medically fragile. A fall during transport or a vehicle accident involving an elderly patient with osteoporosis can generate six-figure medical costs fast. Emergency room treatment for a fractured hip exceeds $30,000 to $50,000 in most urban markets before rehabilitation and long-term care enter the picture. Yet many standard NEMT policies cap medical payments coverage at $5,000 per person, which means your fleet absorbs the remainder.

Brokers like ModivCare and MTM typically require $1 million per occurrence in auto liability, but that covers property damage and third-party claims, not your own passengers. Medical payments or passenger injury protection is the separate coverage layer that protects your passengers, and it remains routinely underestimated. A $10,000 limit sounds reasonable until a bariatric patient requires emergency surgery after a transport incident. Try setting passenger injury limits at $25,000 to $50,000 per person minimum, especially if you transport stretcher or bariatric patients. This costs roughly $300 to $600 annually as an add-on and eliminates the gap between what insurance pays and what your fleet ends up covering from cash flow.

Non-Emergency and Deadhead Miles Left Unprotected

Many NEMT fleets operate in gray zones that standard policies don’t address clearly. Your vehicles sometimes transport patients outside normal medical appointment scenarios-an urgent same-day request, a trip to a pharmacy, or a ride to a dialysis center that falls outside your broker contract. These trips may not qualify as NEMT under your policy’s specific definitions, leaving you exposed if an accident occurs.

Deadhead miles, where your vehicle returns empty after dropping a patient, represent another common gap. Some carriers exclude or limit coverage on deadhead runs, which means half your annual mileage could sit unprotected. A vehicle traveling 60,000 miles annually might spend 30,000 on deadhead, and if an accident happens during those miles, your policy might deny the claim. Confirm with your broker or insurer exactly which trips your policy covers and request explicit endorsements for non-standard scenarios.

Ask whether deadhead coverage is included or available as a rider. For fleets operating across state lines, verify that your coverage applies in every state where you operate, because state Medicaid requirements vary and some carriers write NEMT policies in select states only.

Physical Damage Gaps in High-Mileage Operations

Comprehensive and collision coverage protect your vehicles from damage, but NEMT fleets often underinsure this layer because vehicle replacement costs exceed what they budgeted. A wheelchair-accessible van costs $45,000 to $65,000 new, and if your collision coverage limits are set to actual cash value rather than replacement cost, you’ll receive depreciated payouts that fall short of replacement. A five-year-old WAV with 120,000 miles might have an actual cash value of $20,000, but replacement cost would be $50,000. The gap comes from your fleet’s pocket.

Medical equipment inside vehicles-wheelchairs, oxygen tanks, and securement devices-often isn’t covered under standard physical damage policies. Inland marine or on-hook coverage specifically protects patient equipment during transport and typically costs $300 to $600 annually per vehicle. Many NEMT carriers now require this coverage because wheelchair and equipment damage claims have risen sharply. Vehicle downtime creates another hidden cost most fleets overlook. If a van sits in the shop for two weeks after damage, your operation loses revenue and must rent replacement vehicles or disappoint patients. Some policies include rental reimbursement coverage; others don’t. Request replacement cost valuation for all vehicles, add inland marine coverage for medical equipment, and include rental car reimbursement at $50 to $75 daily minimum. These additions cost roughly $800 to $1,500 per vehicle annually but protect your operational continuity when damage occurs.

Identifying Your Coverage Blind Spots

The gaps that expose your fleet most often stem from assumptions rather than policy language. You assume your auto liability covers passenger injuries, but it doesn’t. You assume deadhead miles are protected, but they may not be. You assume your vehicle’s replacement cost matches what insurance will pay, but actual cash value often falls short. A conversation with your agent before you need to file a claim costs nothing and prevents thousands in denied coverage later. This foundation of clarity positions you to evaluate which insurance provider actually understands your operation well enough to close these gaps-a decision that separates adequate protection from genuine peace of mind.

Selecting an NEMT Insurer That Actually Understands Your Operation

Speed and Specificity Separate Specialists from Generalists

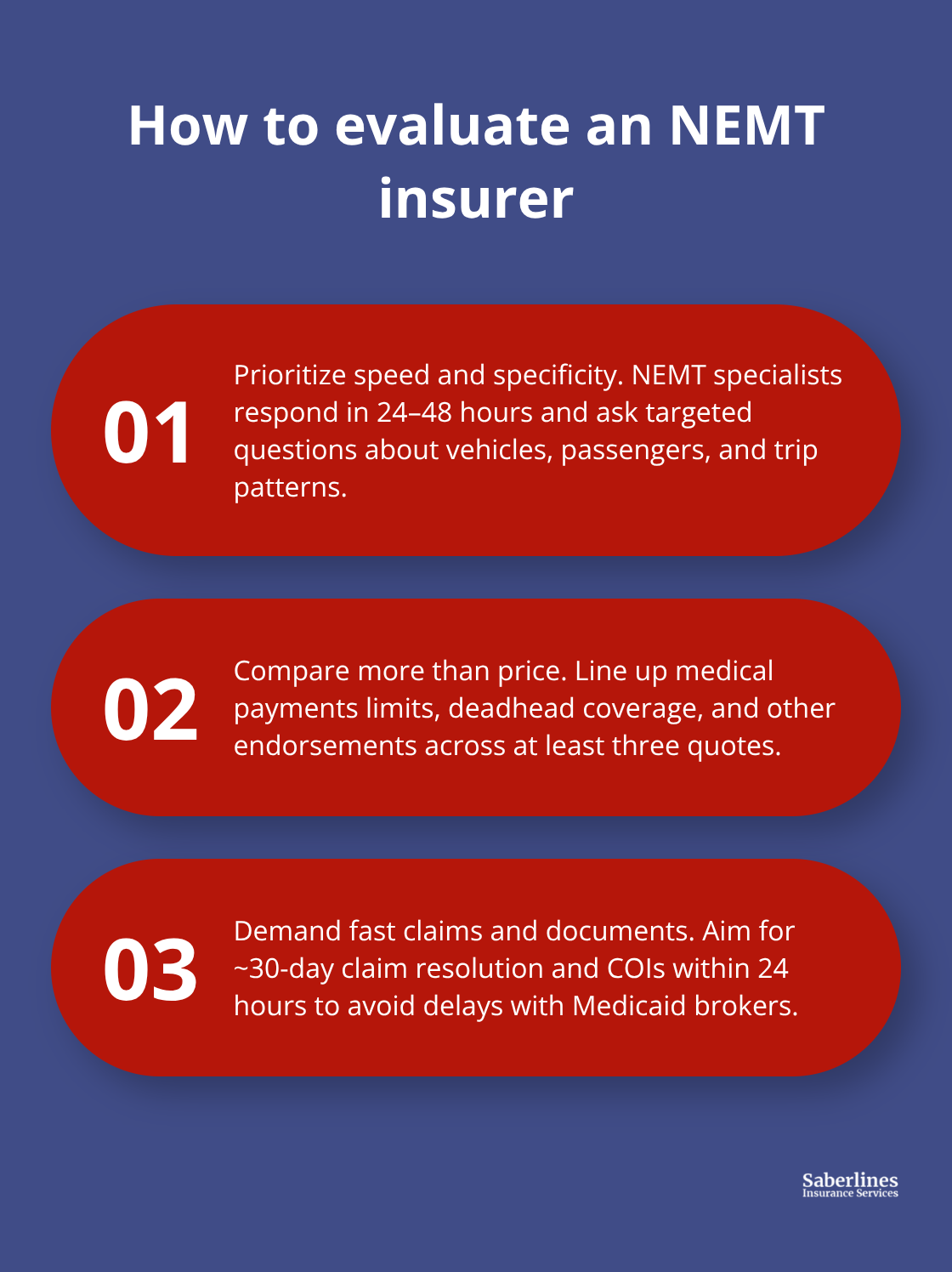

The difference between a generic commercial auto insurer and one that specializes in NEMT appears immediately when you request a quote. A specialist responds within 24 to 48 hours with specific questions about your vehicle types, passenger populations, and trip patterns because they already know what matters. A generalist takes five business days, asks vague questions about your business, and returns a quote that doesn’t account for wheelchair-accessible vehicle surcharges or deadhead coverage. This speed and specificity matter because NEMT insurance requires detailed underwriting. Fewer than 30 carriers nationwide write NEMT coverage, and many major insurers have exited the class entirely, which means your options are genuinely limited.

When you contact a potential provider, ask immediately which carriers they place business with. Specialists typically work with carriers like Nationwide, Progressive Commercial, Markel, Canal, Chubb, and Travelers, all of whom maintain active appetite for NEMT risk. If an agent cannot name their carrier relationships or mentions only one or two options, move on.

Comparing Quotes Requires More Than Price

Request at least three quotes from NEMT-specialist brokers or agencies before deciding. Compare not just price but what each quote includes. One quote might cap medical payments at $5,000 per person while another offers $25,000. One might exclude deadhead coverage while another includes it. Price alone tells you nothing if the underlying coverage differs. Saberlines Insurance Services specializes in passenger transportation including NEMT and delivers quotes within 24 to 48 hours while addressing hard-to-place risks that generalist brokers decline.

Claims Support and Response Time Matter Most

When a vehicle accident happens at 2 p.m. on a Wednesday, you need someone answering the phone, not an automated system directing you to a claims portal. Ask potential insurers whether they handle claims in-house or outsource to a third-party adjuster. In-house claims teams typically resolve straightforward incidents faster because they understand NEMT operations and don’t need education about why a patient fall during transport differs from a standard auto accident.

Request their average claims resolution time for routine liability and medical payments claims. Thirty days is reasonable; 60 days signals slower processing. Verify that your insurer provides a Certificate of Insurance within 24 hours of policy issuance because Medicaid brokers like ModivCare and MTM require this before you can accept trips. Some carriers take a week, which delays your ability to start operations.

MCO Credentialing Support and Documentation Access

Ask whether your agent or broker handles MCO credentialing support, which means they manage the paperwork for medical transport networks and Medicaid enrollment. This service saves your operation dozens of hours annually and reduces the risk of enrollment gaps that suspend your trip assignments. Confirm that your insurer can provide loss runs and driver qualification file audits if you face a Medicaid audit. State Medicaid agencies increasingly audit NEMT providers’ insurance documentation and safety records, and an insurer that can deliver these documents quickly protects you from non-compliance penalties.

Evaluating True Value Beyond the Quote Price

The cheapest quote rarely delivers the fastest claims or best support. A carrier that processes claims in 30 days, provides same-day Certificates of Insurance, and handles MCO credentialing support costs more upfront but saves your operation money through faster trip assignments and fewer administrative hours. Evaluate each potential insurer on response speed, claims handling capability, and credentialing support alongside price to identify the provider that actually protects your operation.

Final Thoughts

The coverage gaps that expose NEMT fleets most often stem from incomplete policies rather than bad luck. You now understand which coverage layers actually protect your operation, where most fleets underinsure themselves, and how to evaluate providers who understand NEMT fleet insurance deeply enough to close those gaps. The difference between adequate protection and genuine peace of mind comes down to specificity: knowing your passenger injury limits match your actual medical costs, confirming deadhead miles are covered, and verifying that your vehicle replacement costs align with what insurance will actually pay.

Start by reviewing your current policy against the coverage checklist in this guide. Pull your declarations page and compare your medical payments limits to the actual emergency room costs in your region. Confirm with your agent whether deadhead coverage is included or available as a rider, and request a loss run from your current carrier to verify whether your vehicle valuations reflect replacement cost or actual cash value (these conversations take an hour and reveal whether your existing coverage protects your fleet or leaves it exposed).

When you’re ready to move forward, request quotes from at least three NEMT-specialist brokers because specialists respond within 24 to 48 hours with detailed questions about your vehicle types and trip patterns. Compare not just price but what each quote includes: medical payments limits, deadhead coverage, inland marine protection for medical equipment, and claims resolution timelines. We at Saberlines Insurance Services specialize in passenger transportation including NEMT and understand the specific risks your operation faces-contact Saberlines Insurance Services to request a quote and speak with someone who knows NEMT fleet insurance inside and out.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.