Truck Insurance for Fleets: Building a Solid Coverage Plan

Fleet owners face mounting pressure to balance protection with cost. The right truck insurance for fleets isn’t just about meeting legal requirements-it’s about safeguarding your operation against real financial risk.

At Saberlines Insurance Services, we’ve helped hundreds of fleet operators build coverage plans that actually work. This guide walks you through the coverage types you need, how to assess your specific risks, and concrete ways to reduce what you pay.

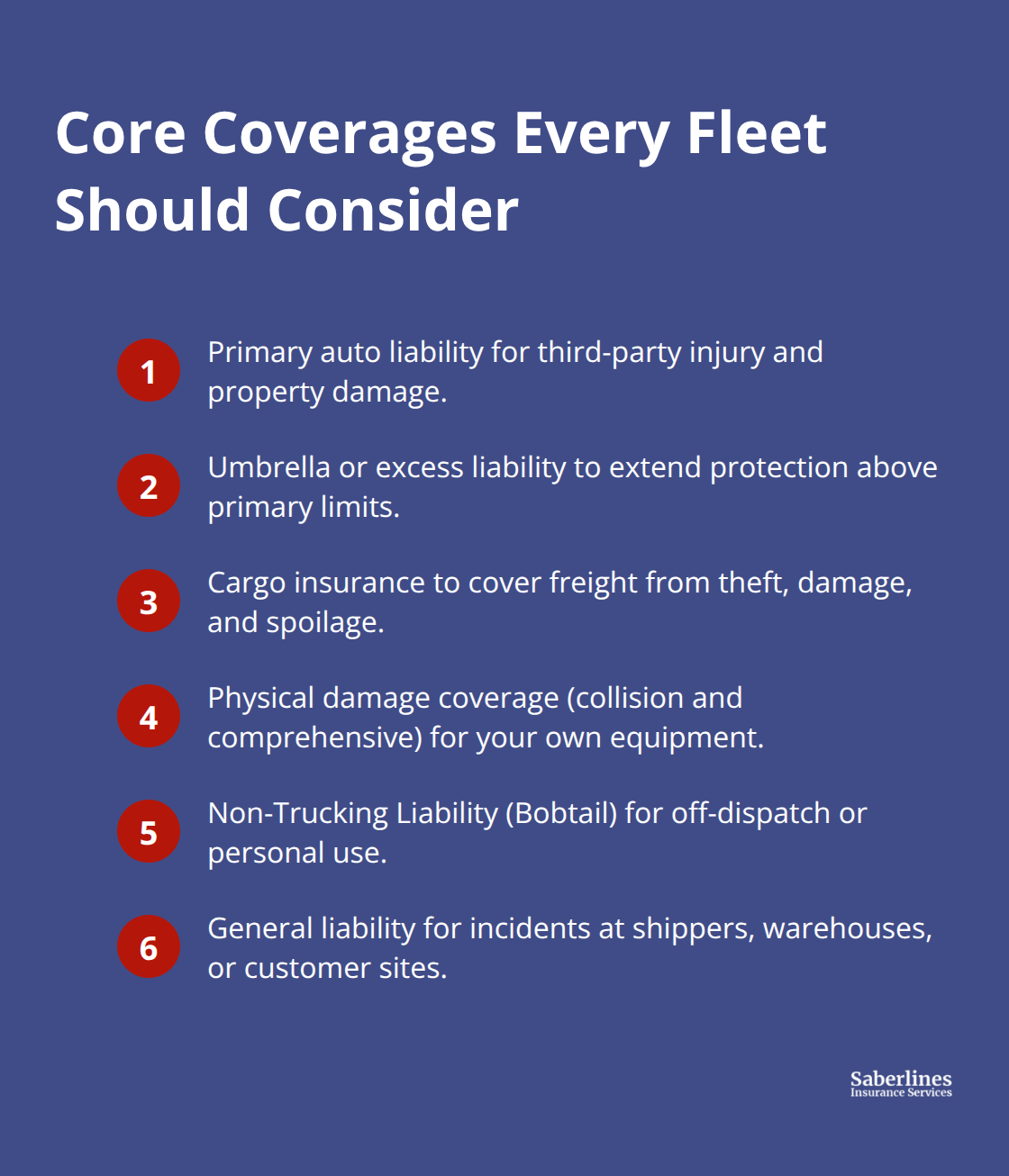

Essential Coverage Types for Fleet Operations

Your fleet needs four core coverage types working together, not in isolation. Primary auto liability sits at the foundation-the FMCSA requires $750,000 for general freight and $1,000,000 to $5,000,000 for hazardous materials depending on cargo type. Most fleets operating regionally or nationally find these minimums dangerously low. According to ATRI data, the average insurance cost per mile reached $0.102 in 2026, driven largely by nuclear verdicts exceeding $10 million. There were 135 nuclear verdicts against corporations in 2024 alone, which means a single accident exposes your fleet to liability far beyond FMCSA minimums. We recommend fleets carry $1,000,000 to $2,000,000 in primary liability as a practical floor, then layer umbrella coverage on top to address the true severity of modern litigation risk.

Protecting Freight and Equipment

Cargo insurance protects the freight itself during transit-it covers theft, weather damage, accidents, and spoilage for temperature-controlled loads. Shippers and brokers typically require specific cargo limits before they dispatch loads, making this coverage operationally essential even though it isn’t federally mandated. Physical damage coverage splits into collision (accidents, rollovers) and comprehensive (theft, fire, vandalism, weather), protecting your own equipment and allowing you to recover quickly after incidents. Non-Trucking Liability, commonly called Bobtail insurance, covers vehicles used for personal or non-dispatch business purposes. This matters more than most fleet operators realize-many states like California and New Jersey enforce strict liability standards for vehicles operating outside dispatch, and a single incident can cost tens of thousands if you lack this coverage.

Aligning Coverage Limits to Your Fleet Profile

The specific limits you choose depend directly on fleet size, cargo value, and operating radius. A 5-truck operation hauling general freight within one region needs different protection than a 25-truck fleet moving temperature-sensitive goods across state lines. Typical monthly costs per vehicle range from $300–$900 depending on fleet size, with larger fleets negotiating better rates. State location matters significantly-premiums in Louisiana, Florida, and New Jersey run 50–100% higher than in Maine or rural areas due to litigation frequency and repair costs.

Cargo Limits and Annual Reviews

If your fleet moves hazmat or operates regionally, your cargo limits should reflect actual load values, not generic minimums. We recommend you review cargo coverage annually as your freight mix changes, because underinsuring cargo creates a false economy-you save $50–100 monthly but face complete loss exposure on high-value loads. General liability rounds out the core stack, protecting against third-party bodily injury and property damage claims at shippers, warehouses, or on customer property. This coverage costs $42–66 monthly per vehicle but prevents gaps that primary auto liability won’t cover.

Moving Beyond Minimum Coverage

Most fleet operators treat insurance as a checkbox rather than a risk-management tool tailored to what they actually haul and where they operate. The next section walks you through how to assess your specific risks and determine which coverage limits actually fit your operation-not just what regulators require, but what protects your bottom line.

Sizing Coverage to What You Actually Operate

Risk doesn’t exist in theory-it lives in your specific operation. A 5-truck fleet hauling palletized goods within 150 miles of its home base faces entirely different exposure than a 20-truck outfit moving temperature-controlled freight across state lines. Fleet operators often treat coverage limits as fixed numbers rather than variables tied directly to what they haul, where they operate, and how many vehicles they run.

Document Your Operation’s Core Facts

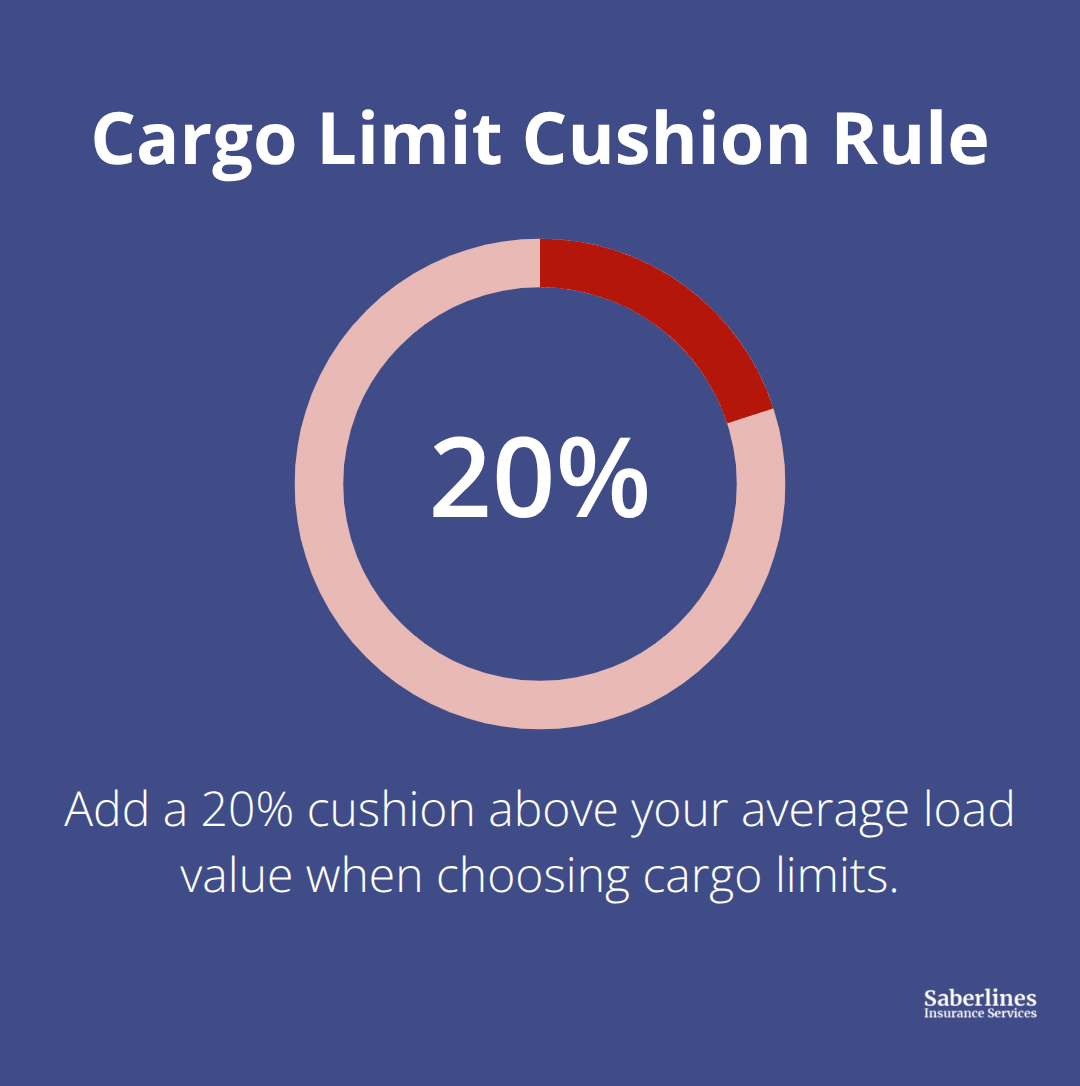

Start with three concrete facts about your operation: total annual cargo value per load, your average operating radius in miles, and your freight classification. A fleet moving high-value electronics or pharmaceuticals needs substantially higher cargo limits than one hauling general merchandise. If your average load value sits at $50,000, your cargo limit should cover that floor plus 20% cushion, meaning $60,000 minimum.

If loads regularly hit $100,000 or more, underinsuring by settling for $50,000 in cargo coverage creates catastrophic exposure that a few dollars monthly in savings can’t justify.

How Operating Radius Affects Your Rates

Operating radius directly correlates with risk severity and underwriter pricing. A 100-mile radius operation within one state typically costs 30–40% less than a multi-state or regional operation because accident frequency, weather exposure, and regulatory complexity all increase with distance and state borders. This relationship holds across fleet sizes and cargo types, making it one of the most predictable cost drivers in fleet insurance.

Fleet Size and Your Negotiating Position

Fleet size determines both your pricing tier and your negotiating power with insurers. A 2–4 vehicle operation pays $300–$900 per vehicle monthly, while a 25-vehicle fleet negotiates rates down to $150–$600 per vehicle monthly simply through volume. More importantly, larger fleets unlock access to group programs and captive insurance structures that smaller operators cannot access, creating substantial long-term savings.

State Location and Compliance Requirements

State location matters more than most operators realize because litigation costs and jury awards vary wildly. According to ATRI data, premiums in Louisiana, Florida, and New Jersey run 50–100% higher than in Maine or lower-risk states due to litigation frequency and repair costs. If you operate across multiple states, compliance requirements shift significantly. Federal FMCSA minimums set the baseline at $750,000 for general freight, but individual states layer additional requirements. California and New Jersey enforce strict non-trucking liability standards that cost $29–50 monthly per vehicle but become non-negotiable if you operate there. Some states require workers’ compensation coverage regardless of whether you have employees; others allow occupational accident insurance as an alternative for owner-operators. The practical approach involves mapping your actual operating footprint, identifying which states you enter regularly, and verifying state-specific requirements directly through your state’s Department of Motor Vehicles or trucking board rather than relying on broker assumptions.

CSA Scores Shape Your Premium and Underwriter Access

CSA scores influence underwriter appetite and final pricing more than most operators understand. A poor CSA score can add 20–40% to your premium, while maintaining clean inspection records and compliance over 12–18 months can lower your classification tier entirely. Request your CSA profile from FMCSA SAFER before shopping quotes so underwriters see the same baseline you do. Once you’ve mapped your operation’s actual profile-fleet size, cargo value, operating radius, and state footprint-you’re ready to shop for quotes that reflect your real risk, not generic minimums. The next section shows you how to compare policies across multiple carriers and identify which bundling strategies actually save money without creating coverage gaps.

How to Cut Fleet Insurance Costs Without Sacrificing Protection

Compare Quotes Across Specialized Carriers

Shopping quotes across multiple carriers reveals a hard truth: the same fleet pays wildly different premiums depending on which insurer evaluates the risk. Identical operations receive quotes at $400 per vehicle monthly with one carrier and $650 with another for the same coverage limits. The difference rarely reflects actual risk difference-it reflects underwriter appetite, loss experience with specific freight types, and how aggressively each carrier prices that particular fleet size or operating radius.

Start with at least three carriers that specialize in trucking rather than general commercial lines, because generalist insurers often overprice or decline trucking risk entirely. Provide each carrier identical information: your exact fleet composition, three-year loss history, CSA scores, current safety technology, and annual cargo values broken down by freight type. Carriers pricing based on incomplete data will quote high; once they see your actual safety portfolio, many will drop rates 15–25%.

Present Your Safety Portfolio Before Renewal

The fastest way to cut premiums at renewal involves presenting a three-year safety portfolio before underwriters even request it. Compile current MVRs on every driver, your CSA profile, dashcam footage highlights showing safe operation, and documented safety training records. Fleets that proactively demonstrate risk controls rather than waiting for underwriters to ask see rate reductions of 10–30% compared to those submitting bare-minimum information.

Consolidate Coverage Under One Insurer

Consolidating coverages under a single insurer creates measurable savings that compound across your fleet size. Carriers typically offer 10–15% discounts when you combine primary auto liability, general liability, cargo, physical damage, and workers’ compensation under one policy rather than splitting them across carriers. A 10-vehicle fleet paying $500 monthly per vehicle in consolidated premiums saves $6,000 annually at a 10% discount-money that justifies the administrative effort to consolidate. More importantly, consolidation eliminates dangerous coverage gaps that emerge when different carriers don’t communicate; one carrier might think another covers trailer interchange when actually it doesn’t, leaving you exposed on non-owned equipment.

Deploy Safety Technology and Driver Monitoring

Telematics and forward-facing dashcams reduce premiums 15–30% according to real fleet data, with most systems paying for themselves within 12–24 months. Underwriters increasingly expect this technology; fleets without it face steeper rates or outright declines from preferred carriers. Install systems that provide real-time driver alerts for harsh braking, speeding, and lane drift rather than passive monitoring-these systems cut preventable accidents 20–40%, which translates directly to lower loss frequency and better renewal rates.

Continuous driver monitoring at hire and every six months through MVR services costs $50–100 annually per driver but prevents you from insuring high-risk drivers who inflate your entire fleet’s premium. Removing even one driver with multiple violations before renewal can lower your class rating enough to offset monitoring costs across your entire operation.

Improve CSA Scores for Outsized Premium Reductions

CSA score improvement delivers outsized premium reductions; a fleet that moves from a poor CSA profile to satisfactory over 12–18 months through documented compliance and training can drop 20–40% from renewal premiums. This requires specific action: schedule quarterly safety meetings, document driver training with attendance records, conduct pre-trip inspections using digital DVIRs rather than paper forms, and track corrective actions when violations appear. Increasing your deductible from $500 to $2,500 can reduce premiums significantly, but only if your cash flow can absorb that out-of-pocket hit when damage occurs.

Final Thoughts

Building a solid truck insurance plan for fleets requires three concrete actions: align your limits to what you actually haul and where you operate, shop quotes across specialized carriers rather than accepting the first offer, and present your safety portfolio before renewal conversations start. The operators who pay the least aren’t those with the smallest fleets-they’re the ones who treat insurance as a risk-management decision tied directly to their operation, not as a regulatory checkbox. Your coverage stack should reflect your specific exposure, whether you move general merchandise within one state or temperature-controlled goods across multiple states.

The fastest path to lower premiums involves consolidating coverages under one insurer, deploying telematics and dashcams that reduce rates 15–30%, and removing high-risk drivers before renewal. CSA score improvement delivers outsized returns; moving from poor to satisfactory compliance over 12–18 months can cut 20–40% from your premium. These aren’t theoretical savings-they’re documented outcomes from fleets that took action and aligned their truck insurance for fleets with their actual operational risk.

Gather your fleet composition, three-year loss history, CSA scores, and current safety technology details, then request quotes from at least three specialized carriers. Contact Saberlines Insurance Services to discuss your specific operation and explore coverage options tailored to your actual risk profile rather than generic minimums. We help owner-operators and fleets navigate this complexity by combining deep industry expertise with fast quotes across preferred and hard-to-place risks.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.