General Liability for Services: Core Protections for Service Providers

Service providers operate in a high-risk environment. A single accident on a client’s property or a mistake during a project can trigger expensive lawsuits that threaten your business.

General liability for services protects you from these financial disasters. At Saberlines Insurance Services, we’ve seen how the right coverage transforms how service providers operate with confidence and security.

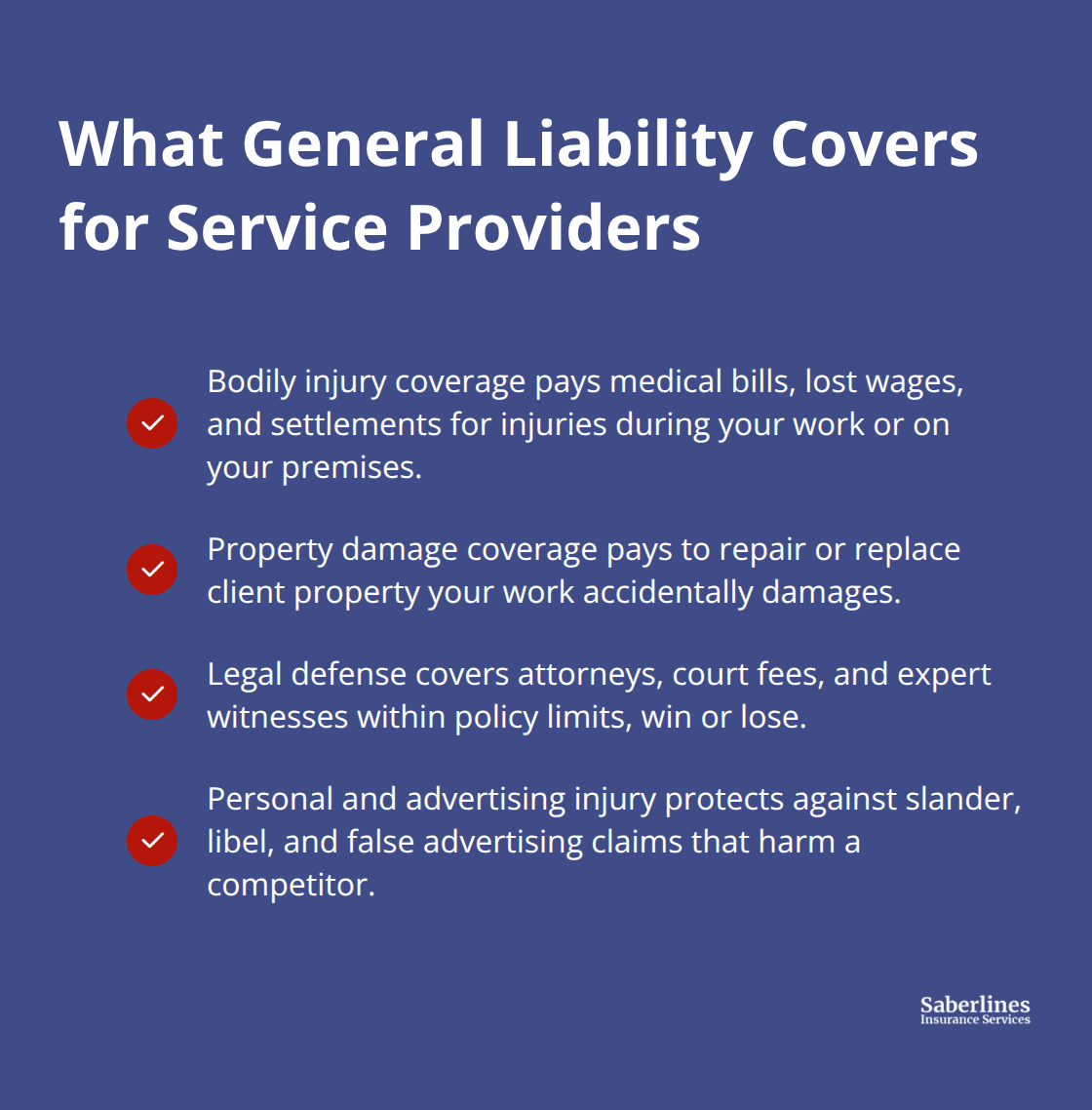

What General Liability Actually Covers

General liability insurance protects service providers from three categories of financial exposure that can devastate small businesses. Bodily injury coverage pays medical expenses, lost wages, and legal settlements when someone is injured during your work or on your premises. A slip-and-fall incident on a client’s property can cost around $200,000 in medical expenses and lost wages, according to Hartford data, with serious cases exceeding $1 million. Property damage coverage handles repair or replacement costs when your work damages client assets-for example, accidentally damaging countertops while moving equipment might cost $25,000 or more. Legal defense costs are included within your policy limits, meaning the insurer pays for attorneys, court fees, and expert witnesses regardless of whether you lose the case. This matters because defense expenses alone can drain $50,000 to $150,000 before a settlement is even reached. Personal and advertising injury coverage protects against claims like slander, libel, or false advertising that harm a competitor’s reputation, which can generate liability in the hundreds of thousands plus court costs.

Medical Payments Coverage Works Independently

Medical payments coverage operates separately from bodily injury liability and covers treatment costs for injuries on your property or caused by your operations, regardless of fault. This means you can cover a client’s medical bills immediately without waiting for a liability determination. The coverage activates quickly and removes friction from the claims process.

Critical Exclusions You Must Know

General liability explicitly does not cover commercial auto accidents, employee injuries (those require workers’ compensation), damage to your own property, professional errors in service delivery, or losses above your policy limits. If you provide professional services like consulting or accounting, you need professional liability (errors and omissions) insurance alongside general liability because GL only covers third-party bodily injury and property damage, not mistakes in your professional judgment.

Standard Coverage Limits for Service Businesses

Hartford reports that small businesses typically start with $1 million per occurrence and $2 million aggregate limits, which provides adequate protection for most service operations while keeping premiums around $810 annually (roughly $67 monthly). These limits represent the maximum amounts your insurer will pay for any single claim and for all claims combined during your policy term. Service providers should evaluate whether these baseline limits match their specific risk profile and contract requirements.

Why Service Providers Really Need This Coverage

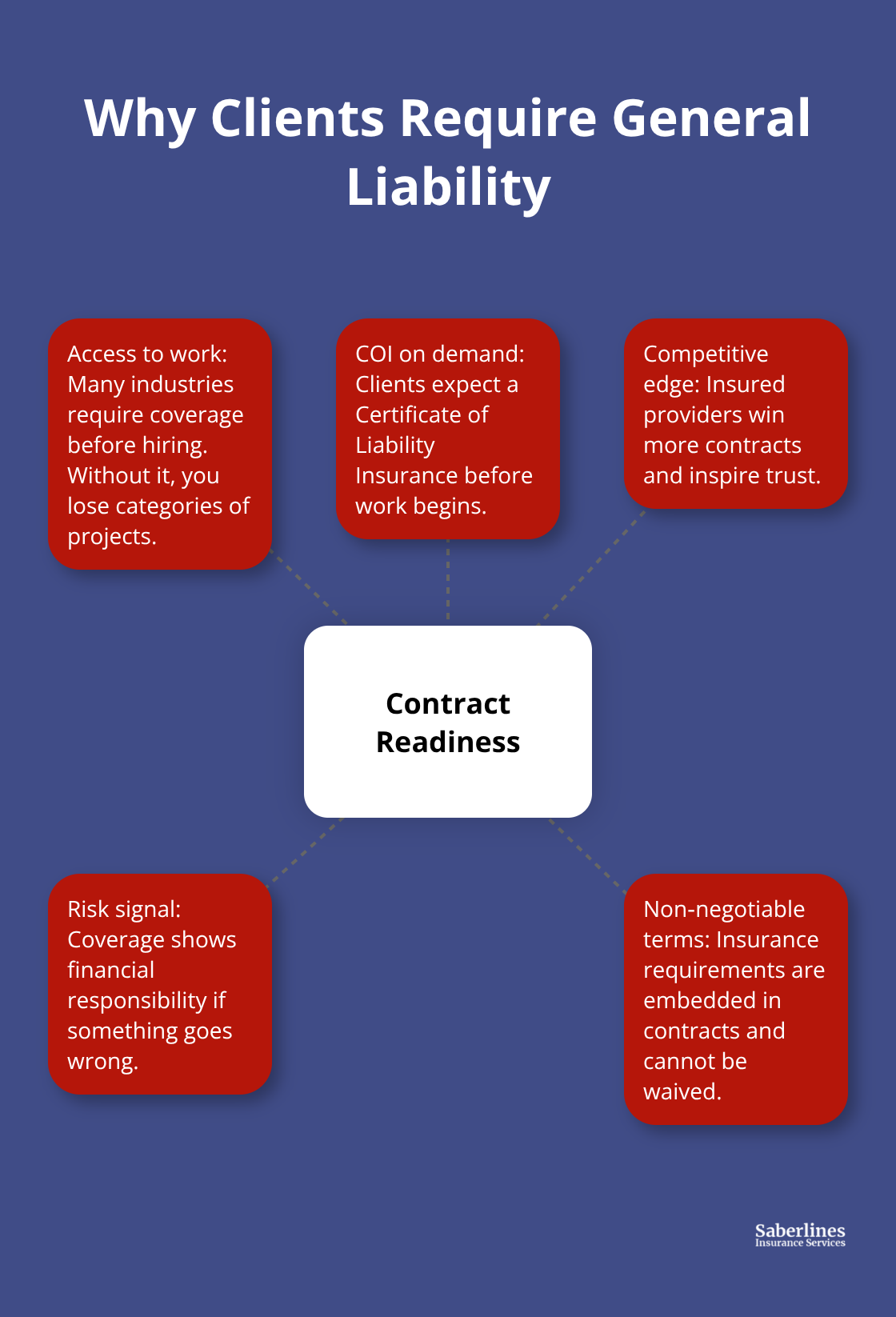

General liability insurance is not optional for service businesses operating in Virginia or anywhere else. Many industries-landlords, general contractors, and those pursuing government contracts-effectively require it before they’ll hire you, regardless of whether state law mandates it. Clients include coverage requirements in their contracts because they want assurance that you’re financially responsible if something goes wrong.

Without proof of coverage, you lose access to entire categories of work and higher-paying projects. A Certificate of Liability Insurance has become standard documentation that clients request before signing agreements, and you cannot provide one without an active policy. The competitive reality is stark: service providers with general liability coverage win more contracts than those without it. You signal to potential clients that you take risk seriously and won’t disappear if an accident happens.

One Claim Destroys Uninsured Service Businesses

A single lawsuit without insurance coverage destroys service businesses. Consider a slip-and-fall incident on a client’s property that results in $200,000 in medical costs and lost wages-a realistic scenario according to Hartford data. If you remain uninsured, you personally pay this amount from your business assets and personal savings. Serious cases exceed $1 million in damages. Most service providers lack $200,000 in reserve funds, which means a judgment forces you to liquidate equipment, vehicles, inventory, and everything else you’ve built. Your business closes. Your personal assets become vulnerable to creditors. General liability coverage prevents this catastrophe by transferring the financial burden to an insurance company. The annual cost of roughly $810 for a small service business is minuscule compared to the financial exposure you carry every single day without coverage.

Clients Demand Proof Before Work Begins

Larger clients and property managers won’t allow work on their premises without documented insurance. Real estate companies, commercial property owners, and corporate clients include insurance requirements in their standard contracts. They request a Certificate of Liability Insurance naming them as an additional insured before you step foot on their property. This contractual requirement appears in the fine print of most service agreements, and violating it gives the client grounds to cancel the contract and pursue damages. You cannot negotiate this away or explain why you lack coverage-the requirement is non-negotiable. Service providers who carry general liability coverage have immediate access to these opportunities because they meet the baseline requirement. Those without coverage spend time explaining why they cannot fulfill contract terms instead of actually working and earning revenue.

Coverage Gaps Leave You Exposed to Catastrophic Risk

Professional errors in service delivery fall outside general liability protection, which means a mistake in your core work leaves you uninsured. If you provide consulting, accounting, design, or technical services, professional liability (errors and omissions) insurance covers negligence in your professional judgment while GL covers third-party bodily injury and property damage. Many service businesses operate with only GL coverage and discover too late that their primary exposure-mistakes in their professional work-sits completely unprotected. This gap transforms a single error into a business-ending liability. You need both policies working together to address the full spectrum of risk your service business faces.

Higher Limits Protect Against Larger Contracts

Standard $1 million per occurrence and $2 million aggregate limits work for many service operations, but larger clients and higher-value projects demand increased protection. Commercial clients often require $2 million per occurrence or higher before they’ll sign contracts with you. A commercial umbrella policy extends your coverage above primary GL limits (often $1 million to $10 million) at a reasonable cost and opens doors to contracts you otherwise cannot pursue. Service providers who evaluate their specific contract requirements and adjust limits accordingly avoid both underinsurance (dangerous gaps) and overinsurance (wasted premiums). Your policy limits should reflect the actual risk profile of the work you perform and the contractual demands your clients impose.

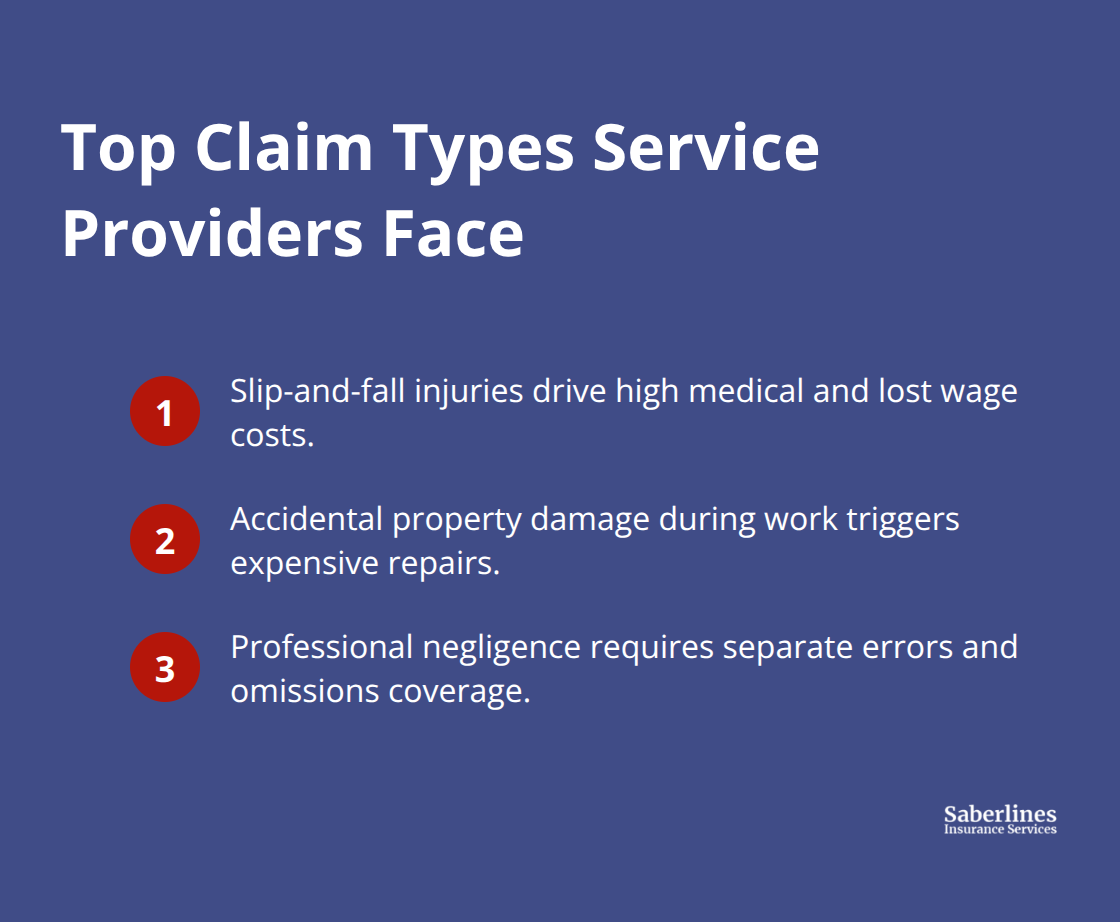

Common Claims Service Providers Face

Slip-and-Fall Incidents Create Immediate Liability Exposure

Slip-and-fall incidents remain the most common claim type service providers face, and the financial impact far exceeds what most assume. Hartford data shows that slip-and-fall accidents on client premises average around $200,000 in medical expenses and lost wages, with serious cases exceeding $1 million. A customer steps on a wet floor at your client’s location, trips over equipment you left in a hallway, or falls on stairs while you work inside-each scenario creates immediate liability exposure. The injury itself represents only the beginning; medical treatment, physical therapy, lost income during recovery, and potential permanent disability drive costs upward quickly. What makes these claims particularly dangerous is that they occur in seconds and often involve clients or their employees rather than direct customers, which means the property owner becomes a witness and potential plaintiff. Your general liability policy covers the full spectrum of these costs, including medical bills, lost wages, legal defense, and settlements, which protects you from personally absorbing five or six-figure payouts. Without coverage, a single slip-and-fall incident forces you to negotiate directly with injured parties or their attorneys from a position of financial weakness.

Accidental Property Damage During Service Work

Accidental property damage during service work ranks as the second major claim category, and the costs accumulate faster than service providers expect. Moving equipment through a client’s home and damaging countertops, cabinets, or flooring routinely generates $25,000 to $75,000 in repair or replacement bills.

Contractors accidentally puncture drywall, scratch hardwood floors, or break fixtures during installations and create similar exposure. HVAC technicians drop equipment on roofs, landscapers damage underground utilities, or IT contractors spill coffee on expensive equipment-all these incidents generate legitimate property damage claims. Your work tools and activities directly cause the damage, which means you bear full liability regardless of how careful you were. General liability coverage pays repair and replacement costs up to your policy limits, removing the need to negotiate settlements from your business bank account.

Professional Negligence Requires Separate Coverage

Professional negligence and service failures represent the third major exposure, though this category requires professional liability insurance rather than general liability alone. A consultant provides faulty business advice that costs a client thousands, an accountant misses a tax deduction that triggers an audit, or a designer creates a flawed plan that requires expensive corrections-all these situations fall outside GL protection. These errors in professional judgment demand errors and omissions coverage working alongside your general liability policy. Service providers who operate with only GL coverage and face a professional negligence claim discover too late that their primary business risk sits completely unprotected, transforming a correctable mistake into a business-closing liability.

Final Thoughts

General liability for services protects your business from the financial disasters that emerge without warning. Slip-and-fall incidents, accidental property damage, and legal defense costs can destroy an uninsured service provider, but the right coverage transfers this risk to an insurance company for roughly $810 annually. Clients demand proof of coverage before they hire you, and larger contracts require higher limits or umbrella policies that expand your protection beyond standard $1 million per occurrence limits.

Your specific risk profile determines the coverage you actually need. Service providers in different industries face different exposures, and your policy limits should reflect the actual work you perform and the contractual requirements your clients impose. Most small service businesses start with $1 million per occurrence and $2 million aggregate limits, though higher-value projects demand increased protection that opens doors to contracts you cannot access without adequate coverage.

At Saberlines Insurance Services, we help service providers secure the general liability coverage they need to operate with confidence. We specialize in commercial insurance solutions and guide you through the process of evaluating your specific exposure and selecting appropriate limits. Your policy requires annual review to keep pace with your growing business, changing operations, and new client contracts.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.