California Trucking Insurance: Navigating State Requirements and Costs

California trucking insurance isn’t optional-it’s a legal requirement that directly impacts your bottom line. The state mandates specific coverage minimums, and getting them wrong can result in fines, license suspension, or worse.

At Saberlines Insurance Services, we help truckers understand what California requires and how to keep costs reasonable. This guide breaks down the requirements, explains what drives your premiums, and shows you concrete ways to save money.

California’s Mandatory Truck Insurance Requirements

Liability Coverage Minimums by Vehicle Weight

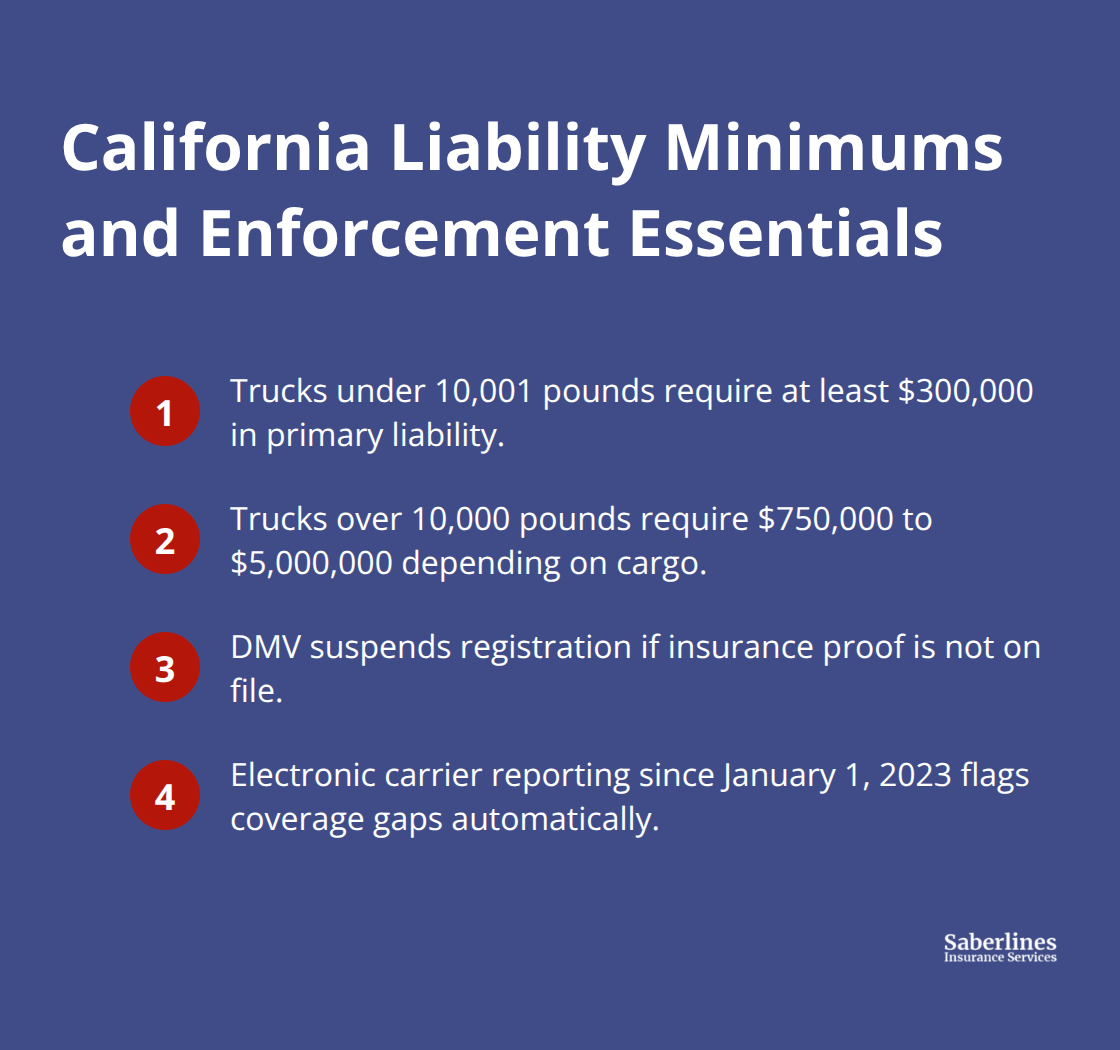

California sets hard minimums for commercial vehicle liability that vary significantly based on vehicle weight and cargo type. For trucks under 10,001 pounds transporting household goods, the state requires at least $300,000 in primary liability coverage. Trucks over 10,000 pounds face steeper requirements ranging from $750,000 to $5,000,000 depending on the cargo transported. The California Department of Motor Vehicles suspends registration if proof of insurance isn’t on file, and you cannot legally operate or park your vehicle on public roads without it.

The state electronically reports insurance information from carriers to the DMV starting January 1, 2023, so gaps in coverage get flagged automatically.

Passenger Carrier Requirements

If you transport passengers, the requirements jump significantly higher based on seating capacity. Carriers with 7 or fewer seats need $750,000 in liability coverage. Those with 8 to 15 seats must carry $1,500,000. Carriers with 16 or more seats must carry $5,000,000. These thresholds reflect the increased risk exposure that comes with transporting people rather than freight.

Understanding Cargo Classification Complexity

Many truckers underestimate their actual cargo liability exposure because California’s definition of cargo extends beyond obvious freight. You might think you’re covered at the minimum, only to discover your specific cargo type triggers higher limits. Truck cargo liability insurance covers damage to third-party owned cargo, while physical damage insurance protects your vehicle itself. State rules can be deceptively complex, and misclassifying your cargo creates serious compliance gaps.

Workers’ Compensation and Federal Compliance

Workers’ compensation is mandatory in California if you have any employees, even one part-time driver. The state requires you to maintain coverage through either a state-approved insurer or a state fund program. If you operate as a sole proprietor with no employees, you can elect coverage or waive it, but hiring someone later makes coverage non-negotiable.

Federal motor carrier regulations often demand additional protection beyond state minimums. If you operate under USDOT authority as an for-hire carrier, federal law typically requires a combined single limit of $750,000 to $1,000,000 depending on cargo type, which exceeds many state minimums and directly increases your costs. You’ll also need to file specific compliance forms with California and federal agencies: the ICC MCS-90, TL672, TL676, and TL1000 forms document your insurance to regulatory bodies.

Beyond Minimum Coverage

Physical damage coverage becomes essential if you lease your truck from another carrier-most lease agreements require it, and skipping it leaves you personally liable for vehicle repairs. Motor truck cargo insurance protects you if cargo suffers damage, theft, or loss during transit, a critical add-on if you haul valuable goods. Meeting minimum state requirements alone isn’t enough for most trucking operations-federal requirements and contract obligations typically demand broader coverage that costs more but protects your business from catastrophic losses. Understanding what actually applies to your operation requires looking at your specific vehicle weight, cargo type, seating capacity, and whether you operate under your own authority or lease to another carrier.

What Drives Your California Truck Insurance Costs

Your truck insurance premium reflects your operational risk profile. Progressive’s 2024 analysis of new for-hire truck policies found national average monthly costs of around $746 for specialty truckers and $954 for transport truckers, but California rates vary significantly based on your specific situation.

Authority Status and Liability Risk

USDOT authority status creates the largest cost difference most truckers face. Operating under your own authority costs substantially more than leasing to a carrier because you assume primary liability risk. When you lease to another carrier, that carrier carries the main liability exposure, which lowers your premiums considerably. This single factor can shift your annual costs by thousands of dollars, making it one of the most important decisions you make about your business structure.

Vehicle Weight and Type

Vehicle weight and type create hard cost differences because heavier trucks and tractor-trailers require higher liability limits by law, directly increasing your base premium. A box truck under 10,001 pounds costs less to insure than a semi-truck over that threshold, but the gap widens dramatically depending on your cargo classification. The relationship between vehicle weight and insurance cost is straightforward: more weight means higher legal liability limits, which means higher premiums.

Driving History and Safety Record

Your driving history determines whether you pay standard rates or face significant surcharges. A clean record with zero accidents and violations qualifies you for the best available pricing. A single speeding ticket or minor accident can increase your annual costs by hundreds or even thousands of dollars, making your driving record far more impactful than most business expenses. This reality means that safe driving practices directly protect your bottom line.

Cargo Type and Operating Radius

Cargo type influences cost in ways that surprise many operators: hauling household goods, agricultural products, or general freight carries different risk profiles than transporting hazardous materials or high-value equipment. Riskier cargo types trigger higher liability rates and often require additional motor truck cargo insurance coverage. Operating radius affects premiums because interstate or cross-state trucking involves greater exposure and route variability than local California-only operations. A driver running regional hauls across state lines pays more than someone making short delivery runs within a single city.

Vehicle Age and Safety Features

Age of your vehicle matters significantly: newer trucks with advanced safety features reduce accident and theft risk, which insurers reward with lower premiums, while older vehicles without modern safety technology cost more to insure. These cost drivers (authority status, vehicle weight, driving record, cargo type, operating radius, and vehicle age) interact with each other, meaning your actual premium reflects a combination of factors rather than any single element. Understanding which factors you can control and which ones are fixed helps you make smarter decisions about where to invest in risk reduction. Your next step involves identifying which cost drivers apply to your operation and exploring strategies that actually lower your premiums without sacrificing the coverage you need.

How to Actually Lower Your Truck Insurance Costs

The cost drivers we outlined earlier aren’t all equal when it comes to what you can actually control. Your driving record and how you structure your authority status create the biggest opportunities for real savings, while vehicle age and cargo type offer secondary levers. Most truckers waste time chasing minor discounts while ignoring the major factors that cut hundreds or thousands from their annual premiums.

Your Driving Record Protects Your Profit Margin

Your driving record directly impacts your bottom line in ways most business owners underestimate. A single accident or violation doesn’t just add a surcharge-it can increase your annual costs by $500 to $2,000 or more depending on severity. This means defensive driving isn’t just about safety; it’s about protecting your profit margin.

If you currently carry violations or accidents on your record, the math is simple: one year of clean driving qualifies you for better rates at renewal, making safe practices your highest-return investment. Progressive’s analysis of 2024 truck policies showed that clean driving records unlock access to the best available pricing tiers, while drivers with violations face substantially higher premiums across all vehicle types.

Authority Structure Creates Enormous Cost Differences

Operating under your own USDOT authority costs substantially more than leasing to a carrier because you carry primary liability exposure. When you lease to another carrier, that carrier carries the main liability exposure, which lowers your premiums considerably. If you currently operate independently but could transition to leasing arrangements with established carriers, that single structural change could reduce your annual insurance costs by thousands.

This isn’t about abandoning independence-it’s about understanding that your authority structure has direct financial consequences. Many owner-operators discover too late that they could have saved significant money by operating under a carrier’s authority while maintaining operational control.

Vehicle Choice and Maintenance Reduce Insurance Costs

Newer trucks with electronic stability control, collision avoidance systems, and advanced braking technology consistently receive lower premiums than older vehicles without these features. If you’re considering a truck purchase or upgrade, the insurance cost difference should factor into your decision alongside fuel efficiency and maintenance expenses.

A five-year-old truck with modern safety systems costs less to insure than a ten-year-old truck without them, and that gap compounds over years of operation. The relationship between vehicle age and insurance cost is straightforward: newer equipment with safety technology reduces risk, which means lower premiums.

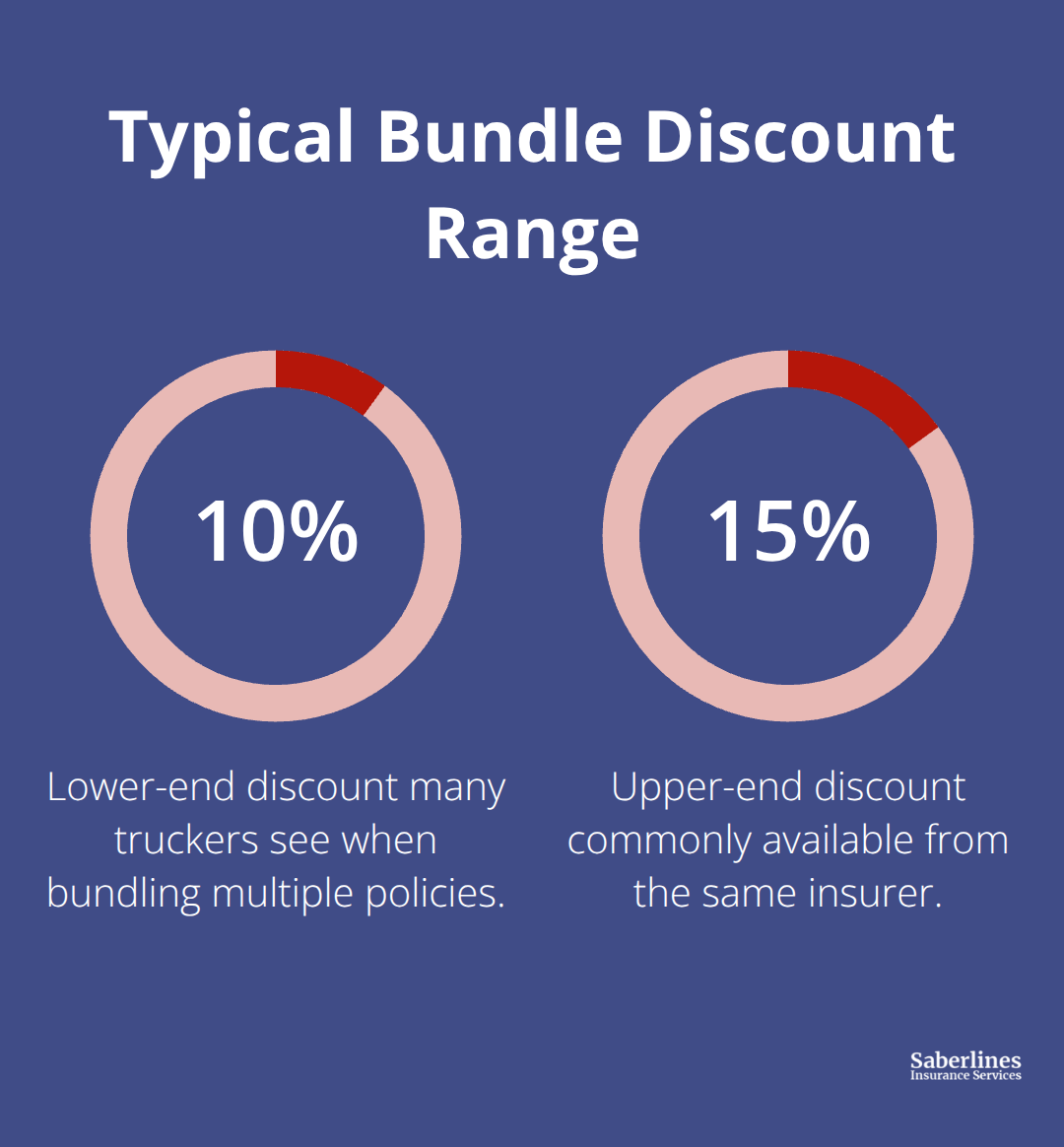

Bundling Coverages Generates Measurable Savings

Adding general liability, workers’ compensation, or property coverage to your commercial auto policy through the same insurer typically generates bundle discounts ranging from 10 to 15 percent. Many independent operators miss these savings by paying for these coverages separately through multiple insurers.

Consolidating your insurance portfolio with one agency doesn’t just reduce your premium-it simplifies compliance and claims handling when you need support. This approach (combining multiple policies with a single provider) creates both financial and operational advantages that compound over time.

Cargo Type and Operating Radius Shape Your Strategy

If you haul household goods or general freight, your rates are lower than hazardous materials operators, but you can still reduce costs by limiting your operating radius to California intrastate routes when possible. Interstate trucking triggers higher premiums due to increased exposure and route variability.

Some operators find that focusing their business on regional California work generates enough volume while keeping insurance costs significantly lower than cross-country operations. Your cargo type influences cost in ways that surprise many operators: hauling household goods, agricultural products, or general freight carries different risk profiles than transporting hazardous materials or high-value equipment. Riskier cargo types trigger higher liability rates and often require additional motor truck cargo insurance coverage.

Final Thoughts

California trucking insurance requirements protect you, your cargo, your passengers, and the public-and getting coverage right means understanding that state minimums vary dramatically based on vehicle weight, cargo type, and seating capacity. Your actual costs depend on factors you control and factors you don’t, but your driving record, authority structure, and vehicle choice create the biggest opportunities for savings. A clean driving history reduces your annual premiums by hundreds or thousands of dollars, operating under a carrier’s authority instead of your own USDOT authority cuts costs substantially because you avoid primary liability exposure, and newer trucks with safety technology cost less to insure than older vehicles without modern features.

Bundling multiple coverages with one insurer generates measurable savings while simplifying your compliance obligations, and limiting your operating radius to California intrastate routes instead of interstate work reduces your premiums because your exposure stays lower and more predictable. Choosing cargo types with lower risk profiles costs less than hauling hazardous materials or high-value equipment, and these secondary strategies compound over time when combined with the major cost drivers. The path forward starts with understanding your specific situation: your vehicle weight, cargo classification, authority status, and current driving record.

We at Saberlines Insurance Services help owner-operators and fleets navigate California trucking insurance by combining deep industry expertise with fast quotes and access to preferred carriers. Contact us at saberlinesins.com to get a quote tailored to your operation and discover what your California trucking insurance actually costs.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.