Commercial Truck Insurance California: Local Coverage for California Carriers

California trucking operations face insurance requirements that go far beyond what federal law demands. State regulators impose stricter liability limits, and the roads themselves present distinct hazards that standard policies often miss.

At Saberlines Insurance Services, we’ve helped California carriers navigate commercial truck insurance requirements that protect both their operations and their bottom line. Getting this right isn’t optional-it’s the foundation of running a sustainable trucking business in the state.

Why California Carriers Face Different Insurance Rules

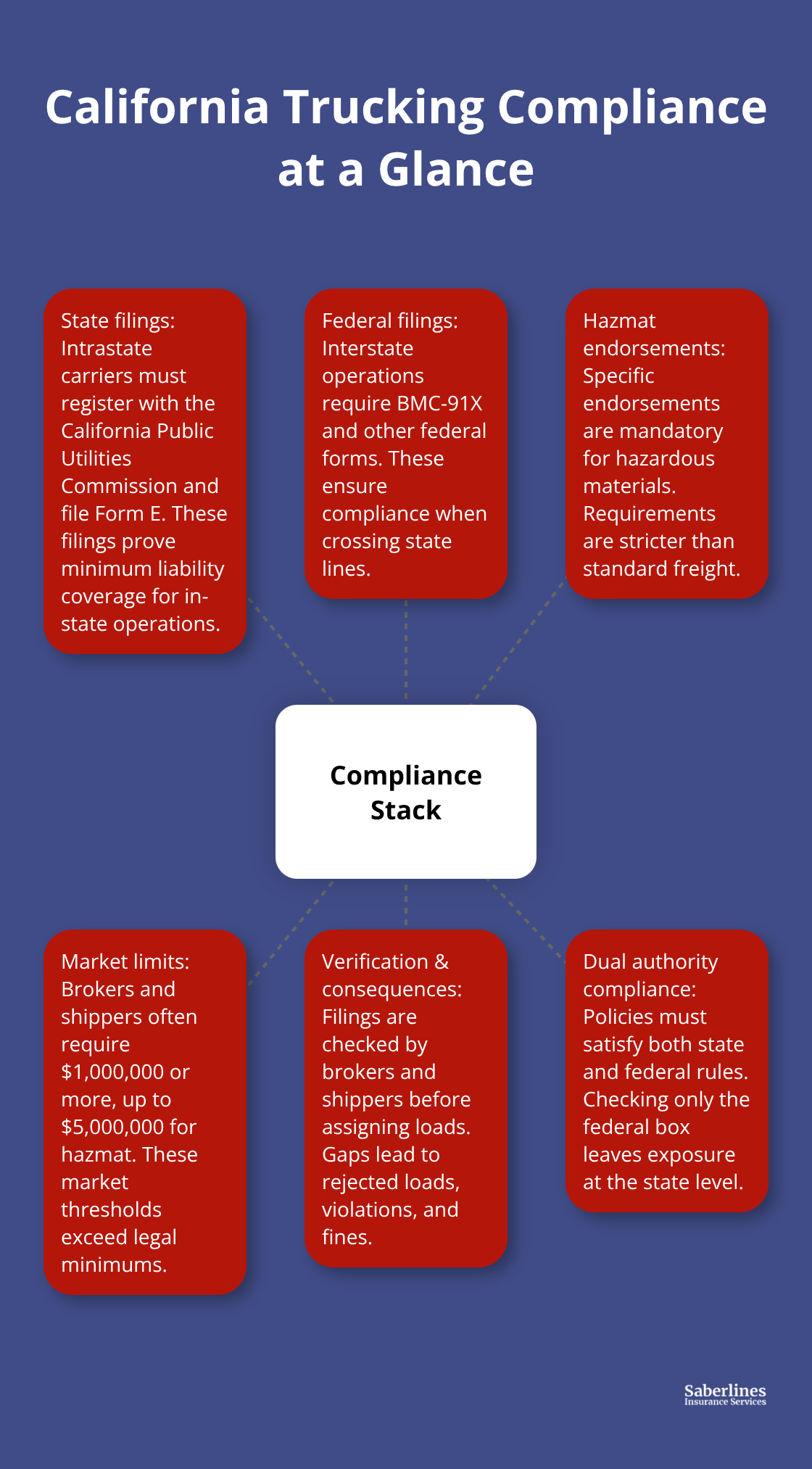

California’s regulatory framework treats commercial trucking differently than the rest of the country, and carriers who ignore this distinction face serious compliance problems and coverage gaps. The state does not simply adopt federal minimums-it imposes its own liability thresholds that sit significantly higher than what the Federal Motor Carrier Safety Administration requires. For intrastate operations within California, you must register with the state’s Public Utilities Commission and file Form E to prove minimum liability coverage. Interstate operations crossing state lines demand even more rigorous filings, including BMC-91X forms and specific endorsements for hazmat shipments. This layered regulatory structure means your insurance must satisfy both state and federal authorities simultaneously, and a policy that checks the federal box alone leaves you exposed to state-level violations and fines.

Many brokers and shippers operating in California also mandate liability limits that exceed state minimums-commonly $1,000,000 even when state law permits lower coverage for certain freight types. This market reality means that carriers treat California like any other state only to discover their policies fall short of what shippers actually require, leading to rejected loads and lost revenue.

State Registration and Filing Requirements

California requires intrastate carriers to register with the Public Utilities Commission and file Form E to demonstrate minimum liability coverage. Interstate operations face additional complexity, as they must complete BMC-91X forms and obtain specific endorsements for hazmat shipments. These filings are not administrative formalities-they directly affect your ability to operate legally and accept loads from major brokers and shippers. A single filing error or missing endorsement can delay your authority activation or result in rejected loads. The Motor Carrier ID rule change (effective in 2025) requires exact matching of your state-issued Motor Carrier ID in insurance filings; filings that use only a DOT number produce a “No Hit” error and prevent authority activation. This precision matters because brokers and shippers verify your filings before assigning freight to your operation.

Market-Driven Liability Limits Exceed State Minimums

State law permits lower liability limits for certain intrastate freight types, but the market operates under different rules. Brokers and shippers commonly mandate $1,000,000 liability limits even when California law allows lower coverage for lighter freight. Hazmat shipments demand liability limits ranging from $1,000,000 to $5,000,000 and require Form E filings that specify your hazmat authority. This gap between legal minimums and market requirements catches many carriers off guard-a policy that satisfies state law may not satisfy the shippers who control your load assignments. You cannot compete for premium freight without matching the coverage limits that major shippers require, regardless of what the state technically permits.

Rising Premiums and Tightening Underwriting

California’s commercial insurance costs have climbed steadily due to higher claim payouts from litigation, increased construction costs, and more frequent natural disasters. Even carriers with clean claims records see premium increases year over year, making cost control through risk management essential rather than optional. Underwriting has become increasingly selective across California, with insurers demanding detailed applications, comprehensive safety protocols, and operational data before issuing policies. Construction, manufacturing, transportation, and hospitality sectors face the tightest scrutiny and the highest potential for coverage reductions. Some coverages once considered standard-like certain cargo exclusions or physical damage provisions-are now being reduced or removed entirely from policies. You cannot afford to accept whatever a quote presents; instead, work with an agent who identifies gaps and discusses alternatives tailored to your specific operations. Proactive risk management through documented safety procedures, driver training programs, and regular operational audits improves underwriter confidence and can offset rising costs without sacrificing protection.

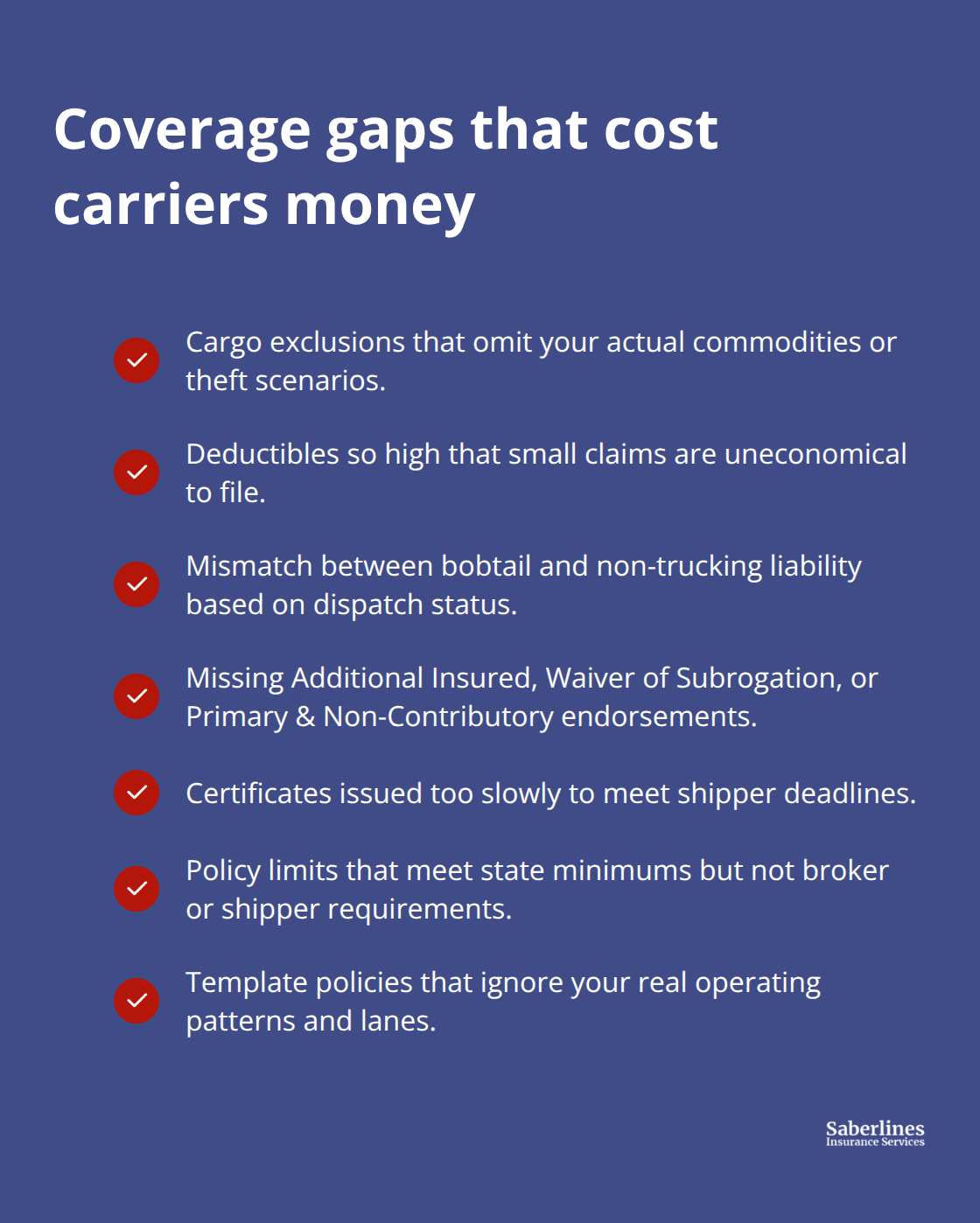

Coverage Gaps That Cost Carriers Money

Many carriers purchase policies that technically comply with state law but fail to cover the scenarios that actually occur on California roads. Cargo policies often exclude specific commodities or theft scenarios that match your typical freight. Physical damage coverage may carry high deductibles that make small claims uneconomical to file. Bobtail versus Non-Trucking Liability coverage depends on your dispatch status, and a mismatch between your actual usage and your policy language results in denied claims when accidents happen. Brokers and shippers require endorsements like Additional Insured, Waiver of Subrogation, and Primary & Non-Contributory-and if your policy lacks these, shippers reject your certificates of insurance and assign loads to competitors instead. The cost of these coverage gaps (missed loads, denied claims, compliance fines) far exceeds the premium savings from purchasing a bare-bones policy. Understanding what your specific operation actually needs-not what a template policy offers-determines whether your insurance protects your income or leaves you exposed when problems arise.

Essential Coverage Types for California Trucking Operations

Liability and Physical Damage: The Foundation

Commercial auto liability and physical damage form the foundation of any trucking operation in California, but they function differently than most carriers assume. Liability coverage pays for injuries or property damage you cause to third parties, while physical damage protects your truck from collision, theft, or weather events. California shippers and brokers demand primary liability limits of $1,000,000 for standard freight and $1,000,000 to $5,000,000 for hazmat operations, regardless of what state minimums technically allow. Physical damage carries deductibles that directly impact your out-of-pocket costs after an accident-a $2,500 deductible means you absorb that loss before insurance kicks in, making deductible selection a real financial decision tied to your cash flow.

Many carriers purchase the lowest available deductible to feel protected, only to discover they cannot afford to file small claims because the administrative hassle exceeds the payout. Instead, select a deductible you can actually absorb without disrupting operations, then invest the premium savings into bobtail coverage or cargo protection that fills genuine gaps in your operation.

Cargo Insurance and Specialized Coverage

Cargo insurance protects the freight you haul, but standard policies exclude specific commodities and scenarios that match exactly what you transport. A general freight policy may exclude electronics, perishables, or high-value items, leaving you liable for losses your shipper assumes you cover. Refrigeration breakdown coverage specifically protects temperature-controlled loads if your reefer unit fails-critical coverage if you haul produce or pharmaceuticals, yet many carriers overlook it until they face a $50,000 spoilage claim.

Non-trucking liability and bobtail insurance address the gap between dispatched work and personal use. If you drive your power unit without a trailer for personal errands or between loads, non-trucking liability covers accidents during those periods when commercial liability does not apply.

Workers’ Compensation and General Liability

Workers’ compensation and general liability round out a complete program. Workers’ comp covers employee injuries regardless of fault, while general liability protects against bodily injury or property damage claims arising from non-vehicle operations like cargo loading or yard accidents. Most carriers treat these coverages as afterthoughts rather than as integral parts of a cohesive program, a mistake that leaves operations exposed to significant financial risk.

Endorsements That Shippers Require

Brokers and shippers require endorsements like additional insured status and waiver of subrogation on your certificates of insurance. If your policy lacks these endorsements, shippers reject your certificates and assign loads elsewhere, making endorsement compliance as important as coverage limits themselves. Fast certificate issuance becomes critical when shippers demand proof of coverage before assigning freight-delays in obtaining certificates cost you loads and revenue. The right insurance partner processes certificates immediately and understands which endorsements your specific freight lanes require, preventing the coverage gaps that result in rejected loads.

How to Choose the Right Insurance Partner for California Trucking

Finding the right insurance provider matters far more than most carriers realize, because your agent either prevents costly coverage gaps or leaves you scrambling after problems arise. California’s regulatory complexity and market-driven coverage requirements demand an agent who speaks trucking fluently, not someone who treats your account as a generic commercial policy. The difference shows up in how quickly your certificates of insurance arrive when shippers demand them, whether your endorsements match what brokers actually require, and whether your cargo coverage actually covers the freight you haul.

What Specialized Trucking Knowledge Looks Like

An agent with deep trucking experience immediately recognizes that your bobtail usage pattern creates a gap, or that hazmat shipments demand specific liability limits and Form E filings that standard policies miss entirely. Agents without trucking specialization treat these requirements as exceptions rather than standard operating procedures, which means they discover problems after you’ve already suffered the consequences. When you evaluate potential providers, ask how many trucking accounts they service and whether they personally understand the difference between intrastate Form E filings and interstate BMC-91X requirements. If an agent struggles to explain why market-driven liability limits exceed state minimums, or cannot articulate how bobtail coverage fills a specific gap in your operation, they lack the specialized knowledge that prevents expensive mistakes.

Comparing Quotes Without Falling for Low Prices

Comparing quotes requires discipline because the cheapest premium almost always reflects reduced coverage or higher deductibles that cost more after an accident. A quote that undercuts competitors by 20 percent likely omits cargo protection, carries a $5,000 deductible instead of $2,500, or excludes specific commodities you regularly haul.

Request detailed breakdowns showing what each quote covers and what it excludes, then map those details against your actual operations. If you haul refrigerated freight but a quote lacks refrigeration breakdown coverage, that savings evaporates the moment your reefer unit fails and you face a $50,000 spoilage claim.

How Underwriting Standards Affect Your Application

Underwriting standards have tightened significantly across California, with carriers now expecting detailed safety protocols, driver training documentation, and operational procedures before policies issue. Agents who invest time understanding your specific operation can present your application in ways that satisfy underwriter requirements and secure better rates than generic submissions receive. Local market relationships matter because some underwriters specialize in particular freight lanes or fleet sizes, and an agent with established connections can access carriers that online quote tools never show. GEICO Commercial Truck Insurance and other national carriers offer broad coverage across vehicle types, but California-focused agencies often secure better rates for specific niches because they work directly with underwriters who understand local conditions and accept the operational nuances that national carriers sometimes flag for additional scrutiny.

Speed of Certificate Issuance and Administrative Support

The fastest certificate issuance happens when your agent maintains systems that produce certificates immediately rather than routing requests through multiple departments. Delays of even 24 hours cost you loads when shippers impose tight deadlines, making speed a practical advantage that directly impacts your revenue. Ask prospective agents how many hours it takes to issue certificates and whether they handle endorsement requests without requiring your approval on every change. The right partner processes these administrative tasks as routine rather than as exceptions, because they understand that load assignments depend on documentation speed. Saberlines Insurance Services processes certificates and endorsement requests immediately, recognizing that shippers impose tight deadlines and delays directly reduce your ability to accept freight.

Final Thoughts

Commercial truck insurance in California demands more than compliance checkboxes-it requires alignment between your coverage and how your operation actually functions. State minimums and market requirements operate on different tracks, which means brokers and shippers set the real standards through their load assignments and endorsement demands. Selecting an insurance partner with genuine trucking expertise prevents the costly mistakes that generic commercial agents make, because specialized knowledge shows up in certificate speed, accurate endorsements, and cargo protection that matches your freight.

We at Saberlines Insurance Services understand the difference between intrastate Form E filings and interstate BMC-91X requirements, recognize how bobtail usage patterns create coverage gaps, and process certificates immediately when shippers impose tight deadlines. Our team secures coverage for operations that online quote tools reject, and we market for preferred and hard-to-place risks across California’s diverse trucking sectors. Contact us to discuss how your current coverage aligns with your actual operations and where gaps might be costing you loads and revenue.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.