General Liability Insurance Quotes: Comparing Rates Without Surprises

General liability insurance quotes vary wildly depending on your business. Without understanding what drives these differences, you might overpay or worse, discover coverage gaps when you need protection most.

At Saberlines Insurance Services, we’ve helped hundreds of business owners cut through the confusion. This guide shows you exactly what to compare and which hidden costs to watch for.

What Drives Your General Liability Quote

Industry Risk Sets Your Baseline Premium

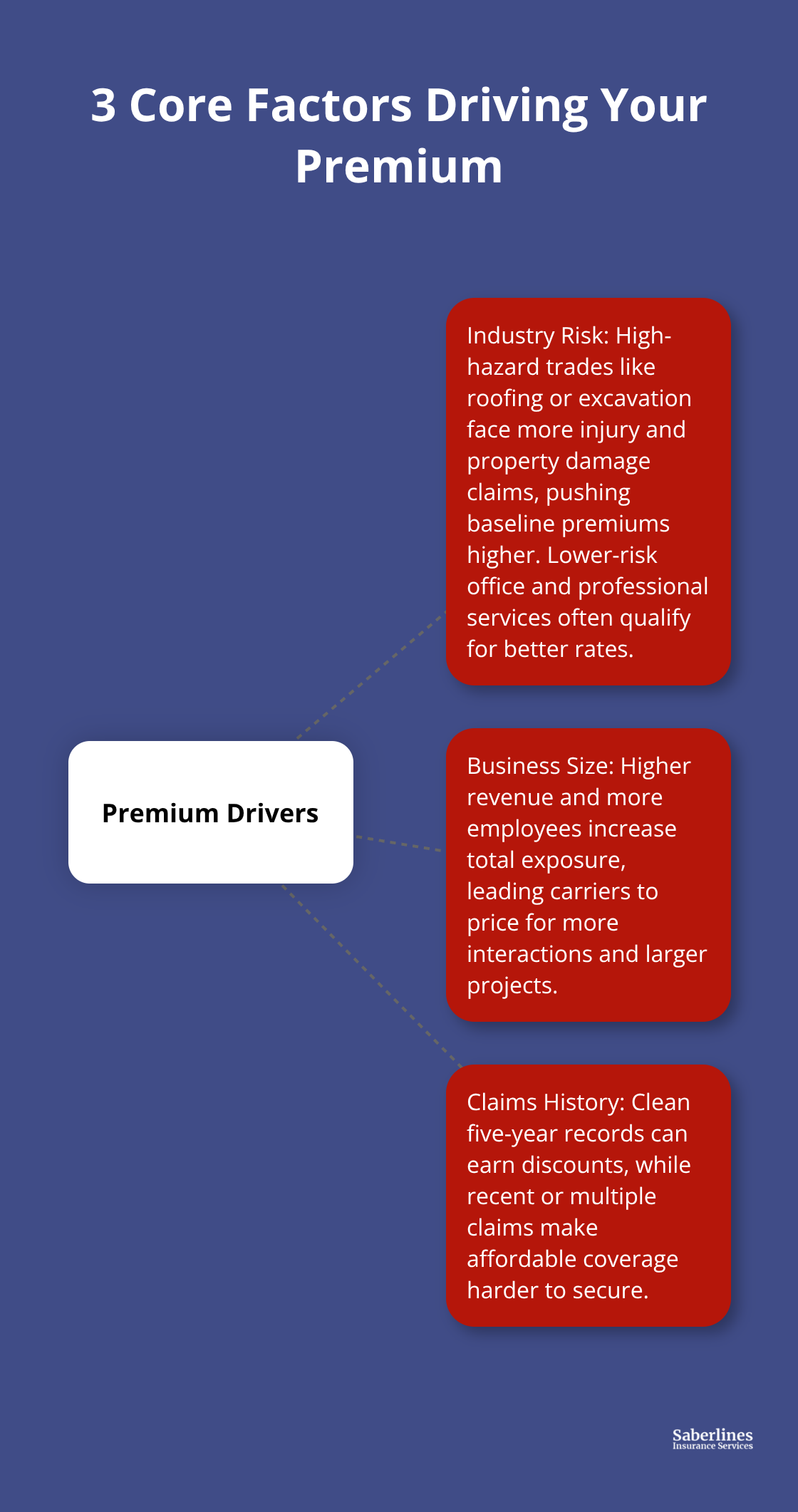

Your industry determines your baseline risk the moment you submit a quote. Construction companies pay roughly double what retail businesses pay because they face more bodily injury and property damage claims. A plumbing contractor operating in a major city might see quotes around $150–200 per month, while a consulting firm in the same area quotes closer to $50–75. The Hartford reports that office-based and professional service businesses typically qualify for better rates than hands-on trades, which means your work type alone can swing your premium by hundreds of dollars annually.

High-risk sectors like excavation, roofing, or HVAC command the steepest premiums because insurance companies have decades of claims data showing these industries generate more incidents. If you operate in a lower-risk category, you have leverage to negotiate better terms. If you’re in construction or similar fields, accepting higher premiums reflects the cost of doing business-what matters is not overpaying within your risk bracket.

Revenue and Employee Count Expand Your Exposure

Your revenue and employee count matter far more than most business owners realize. A one-person operation with $100,000 annual revenue faces completely different underwriting than a five-person team doing $500,000 in work, even if they’re in the same industry. Insurers use revenue as a proxy for total exposure; more money typically means more client interactions, larger projects, and greater liability potential.

ERGO NEXT dominates the very small business segment (0–4 employees) because their pricing reflects this lower-exposure reality, averaging about $107 per month-roughly 13% below the national benchmark. Adding a second or third employee usually increases your quote noticeably because each person represents another potential source of claims. Your staffing decisions directly impact what insurers charge you.

Claims History Determines Your Long-Term Costs

Your claims history is the final major lever on your premium. A clean five-year record with zero claims can reduce your quote by 10–20% compared to a business with one significant claim, according to industry standards. A single claim from two years ago stays on your record and directly raises your premium; two claims within five years makes finding affordable coverage substantially harder.

If you’ve had claims, your only path forward involves demonstrating genuine risk improvements-better safety protocols, updated equipment, formal training programs. Request a premium review after 12–24 months of clean history to show insurers that your business has changed. The insurers you approach next will scrutinize your loss record carefully, which is why understanding what they see on your report matters before you start requesting quotes.

Comparing Quotes Side by Side Without Getting Misled

Request Quotes from Multiple Insurers Using Identical Terms

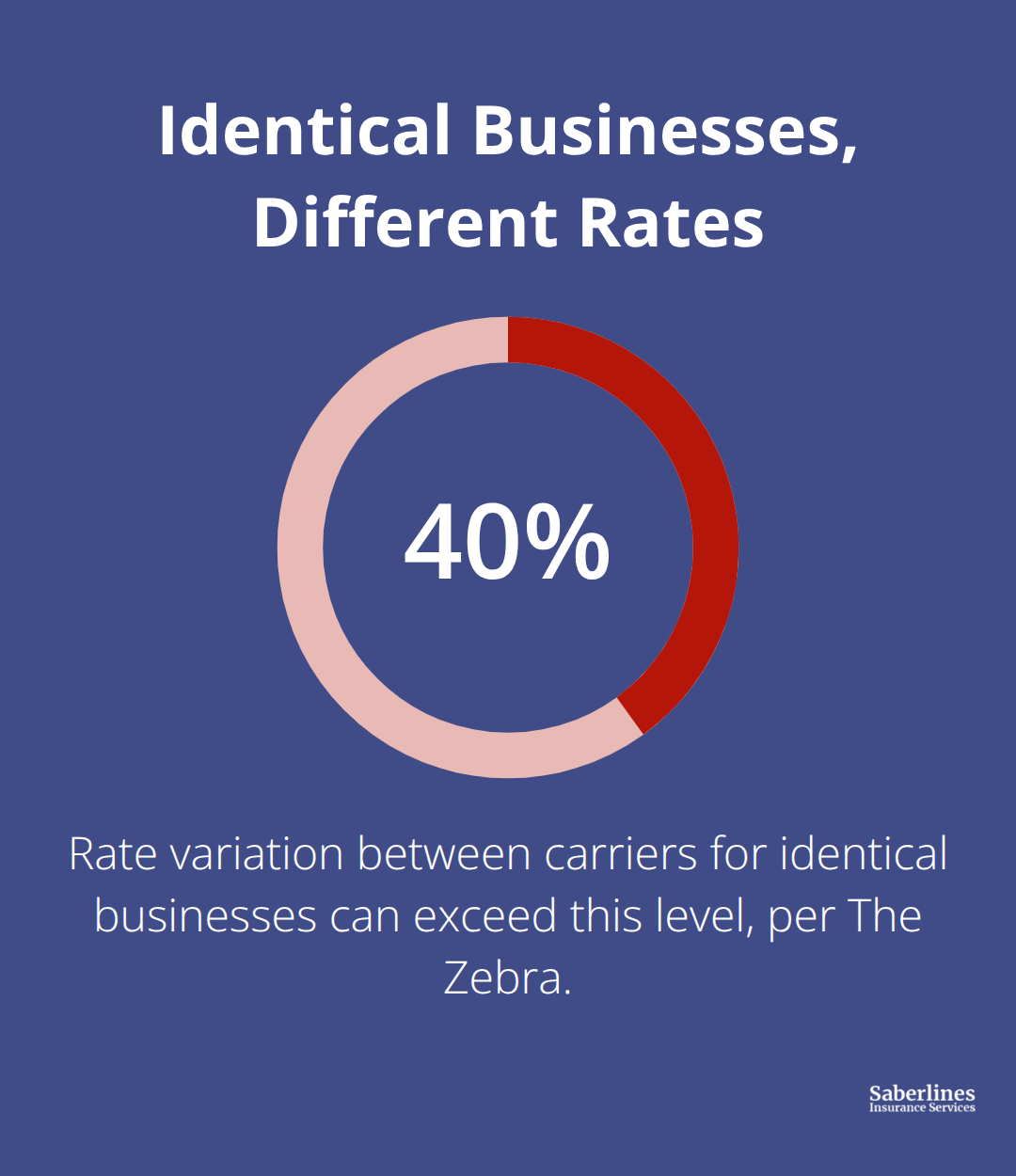

You must obtain quotes from three to five insurers if you want accurate pricing. Most business owners stop after one or two quotes and assume they’ve seen the market, which costs them money. The Zebra’s comparison methodology evaluated over 400 industries across all 50 states and found that rate variations for identical businesses can exceed 40% between carriers.

Simply Business exists specifically because no single insurer dominates every risk profile, which means the cheapest quote for a roofing contractor might come from a completely different carrier than the cheapest quote for an accounting firm.

Request quotes with identical coverage limits and deductibles across all providers so you actually compare apples to apples. If you ask one insurer for $1 million per occurrence and another for $2 million, the price difference tells you nothing about their competitiveness. Fill out each questionnaire thoroughly and truthfully because underwriting adjustments after submission can swing your final premium significantly.

Understand How Carrier Pricing Favors Different Business Sizes

ERGO NEXT and The Hartford both excel at online quoting, but they price differently based on your business structure. The Hartford’s rates average about 17% below the national average for office-based businesses with 5–49 employees, while ERGO NEXT dominates the 0–4 employee segment at roughly 13% below benchmark. Your business size determines which carrier’s pricing structure favors you most, so don’t assume the lowest initial quote will remain lowest after underwriting reviews your complete risk profile.

Balance Coverage Limits Against Your Actual Liability Exposure

Coverage limits and deductible choices create the second major comparison trap. A $300,000 per-occurrence limit from biBERK costs dramatically less than a $1 million limit from the same carrier, but the cheaper option leaves you exposed if a single incident causes $500,000 in damages. Your deductible choice works the opposite direction: raising your deductible from $500 to $2,500 typically reduces your premium by 15–25%, but you’ll absorb that $2,000 difference out of pocket if you file a claim.

The Hartford offers up to $2 million per occurrence and $4 million aggregate without umbrella insurance, giving office professionals genuine protection for complex claims, while biBERK’s $300,000 minimum suits lower-risk sole proprietors perfectly. Review your actual liability exposure before selecting limits based purely on price. If you regularly work on client premises, handle valuable equipment, or interact with the public extensively, skimping on limits to save $30 monthly creates catastrophic risk.

Identify Policy Exclusions and Required Endorsements

Policy exclusions matter equally because what’s not covered often matters more than what is. Standard CGL policies exclude employee injuries, intentional acts, pollution cleanup, and contractual liabilities, which means if you’ve promised a client to maintain their property or indemnify them in your contract, your standard general liability won’t cover that obligation.

Request quotes for additional endorsements like additional insured status, waiver of subrogation, and primary and noncontributory coverage if your clients require them, because adding these later costs more than including them upfront. Simply Business specializes in contract-related endorsements available online, making it efficient for comparing how different carriers price these essential add-ons. Your contract obligations determine which endorsements you actually need, so review your client agreements before you finalize any quote comparison.

What Costs Hide Inside Your General Liability Quote

Most business owners encounter hidden costs only after they’ve already purchased a policy, which is far too late. Your initial quote price is rarely your final cost because insurers layer in additional fees, exclusions create coverage gaps that force out-of-pocket spending, and claims history triggers premium increases that catch you off guard. Understanding where these costs originate gives you the leverage to negotiate better terms before you sign anything.

Additional Fees Add Up Fast

Additional fees exist in nearly every general liability policy, though most quote systems bury them in fine print or mention them only after you’ve committed to a carrier. Processing fees, policy issuance fees, and administrative surcharges can add $50–150 annually to your quoted premium, which means a $600 annual quote actually costs $700–750 once you account for these charges. Some carriers charge specific surcharges for high-risk industries; a construction company might see a 5–10% risk surcharge added after underwriting reviews their actual job sites and safety protocols.

Request the complete fee schedule from every carrier before you compare final costs, not just the base premium they advertise. Several carriers also charge endorsement fees when you add required coverage like additional insured status or waiver of subrogation, with costs ranging from $25–75 per endorsement depending on the carrier and complexity. When selecting the right policy, compare how different carriers price endorsements, since the carrier offering the lowest base premium might cost more once you add the endorsements your clients actually require.

Coverage Gaps Leave You Exposed

Coverage gaps represent the more dangerous hidden cost because they leave you exposed to claims your policy won’t cover. Standard CGL policies exclude employee injuries, meaning workers compensation is a separate purchase, but many sole proprietors mistakenly believe their general liability covers anyone working on their behalf. If you hire a subcontractor and they suffer injury on a job, your general liability provides zero coverage, leaving you personally liable for medical costs and lost wages.

Similarly, contractual liability exclusions mean if your client contract requires you to indemnify them or maintain their property, your standard policy won’t cover that obligation unless you’ve added the endorsement specifically. These gaps force you to absorb costs that proper coverage would have handled, which often exceeds the premium savings you thought you achieved by selecting a cheaper policy.

Claims History Triggers Long-Term Premium Increases

Premium increases after claims hit differently than initial quotes because they compound over time. A single claim typically raises your premium 10–20% for the following three years, and multiple claims within five years can increase your rate 30–50% or force non-renewal entirely. This means one significant incident doesn’t just cost you the claim amount-it costs you thousands in elevated premiums across years.

Short-term on-demand coverage averaging around $115 monthly works well for gig workers avoiding long-term premium damage from occasional claims, but most traditional carriers lock you into multi-year rate increases once you file. The solution involves reviewing your actual risk exposure before you need coverage and selecting limits that reflect your real liability potential rather than choosing the cheapest option available.

Final Thoughts

Accurate general liability insurance quotes demand that you compare multiple carriers using identical coverage terms and deductible levels. The three core factors-industry risk, business size, and claims history-shape your premium at every insurer, but each carrier prices these factors differently based on their underwriting appetite and target market. A quote that appears cheap initially often hides additional fees, coverage gaps, or endorsement costs that inflate your actual expense significantly.

An insurance agent transforms this process from overwhelming to manageable by accessing carrier networks independently, identifying which insurers price favorably for your specific business type, and catching coverage gaps before you purchase. Agents negotiate fee schedules directly, bundle endorsements efficiently, and match your limits to your actual liability exposure rather than leaving you either overinsured or dangerously exposed. At Saberlines Insurance Services, we help transportation businesses and owner-operators navigate complex coverage needs with precision, marketing your risk across preferred carriers to deliver fast, affordable quotes without surprises-visit us today to discuss your specific requirements.

Your next step is straightforward: gather your business information, request general liability insurance quotes from three to five carriers using identical terms, and have an agent review the complete fee structure before you commit. This approach takes a few hours now and saves you thousands across your policy period.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.