Physical Damage Trucking Insurance: Protect Your Assets on the Road

Your truck is your livelihood, and one accident can wipe out months of profits. Physical damage trucking insurance protects your vehicle from collisions, weather, theft, and other events that could sideline your business.

At Saberlines Insurance Services, we help owner-operators understand what coverage actually matters and how to avoid paying for protection you don’t need. This guide walks you through the essentials so you can make informed decisions about your assets.

What Your Physical Damage Policy Actually Covers

Collision coverage handles the most straightforward scenario: your truck hits something, or something hits your truck. This includes overturns, jackknifes, and impacts with other vehicles or stationary objects. The insurer pays for repairs or replacement based on the actual cash value of your truck at the time of loss, not what you paid for it years ago. If your truck is worth $45,000 and repair costs run $12,000, you pay your deductible and the policy covers the rest.

The Federal Motor Carrier Safety Administration reports that the average cost of a non-injury large truck crash reaches approximately $47,000, which means even one significant collision can exceed your truck’s value. Collision is non-negotiable if you financed or leased your equipment, and lenders will require it in your policy.

What Comprehensive Actually Protects

Comprehensive coverage handles losses that don’t involve a collision: theft, vandalism, fire, hail, weather damage, and other non-accident perils. This matters more than many owner-operators realize. If someone steals your catalytic converter or your truck burns in a garage fire, collision won’t help you. Comprehensive also covers glass damage, fallen trees, and water damage from flooding.

You need both collision and comprehensive unless you own an older truck with minimal value, which is rare advice you’ll hear. Most fleets should carry both because downtime from a weather event or theft costs just as much as downtime from a wreck. The actual cash value approach means your payout reflects depreciation, so a 2015 truck worth $35,000 gets valued at $35,000, not the $60,000 you paid originally. This is why you should reassess your truck’s value annually, especially if you upgrade components or maintain exceptional condition.

The Cargo Question

Cargo coverage is separate from physical damage insurance and protects the freight you carry, not your truck. Physical damage covers your tractor and trailer only. If you haul someone else’s goods and they get damaged in a crash, your cargo policy pays the shipper, not your physical damage policy. This distinction confuses owner-operators frequently.

You need cargo coverage if you haul freight under a broker or shipper arrangement, but it’s a different policy line entirely. Many owner-operators overlook this and assume physical damage handles everything. It doesn’t. Talk to your agent about what you actually haul and whether cargo coverage applies to your operation. Some owner-operators under permanent leases receive cargo coverage through their motor carrier, so you should verify your existing protection before you buy duplicate coverage.

Actual Cash Value vs. Replacement Cost

Your physical damage payout reflects actual cash value, which accounts for depreciation and the truck’s condition at the time of loss. This means a newer truck with lower mileage and well-maintained systems receives a higher valuation than an older unit with the same make and model. You won’t recover what you originally paid, but you will recover what the truck is worth on the market today.

Lenders and lessors typically require physical damage coverage at actual cash value to protect their interest in the equipment. If you own your truck outright, you still benefit from accurate valuation because it determines how much the insurer pays when a loss occurs. Undervaluing your truck leaves you short when repairs or replacement becomes necessary.

Moving Forward With Coverage Decisions

Understanding what physical damage covers sets the foundation for choosing limits and deductibles that match your operation. The next step involves assessing your specific truck’s value, your financial situation, and the deductible levels that make sense for your business model.

Why Physical Damage Coverage Protects Your Bottom Line

Repair Costs Have Skyrocketed

Repair costs in trucking have climbed dramatically. Parts inflation, labor shortages, and supply chain disruptions mean a collision that cost $15,000 to fix five years ago now runs $22,000 or higher. Your truck sitting idle while repairs happen doesn’t just cost you money-it costs you income. An owner-operator earning $0.70 per mile loses roughly $1,680 in gross revenue for every 2,400 miles missed during a two-week repair cycle. If your truck stays down for a month, you’re looking at $3,360 in lost income before accounting for fuel, maintenance, and other operating costs.

Speed Matters When Your Truck Goes Down

Physical damage coverage gets you back on the road faster because insurers with strong repair networks can schedule work immediately rather than forcing you to hunt for a shop and wait weeks for availability. The difference between a carrier that processes claims in three days versus three weeks directly impacts your ability to accept loads and keep cash flowing. Without physical damage coverage, a $35,000 repair bill comes straight from your pocket, which forces many owner-operators to take out loans at high interest rates or sit idle longer while they save. That downtime compounds-every week you’re not running is a week you can’t pay yourself, cover truck payments, or build emergency reserves.

Lenders and Lessors Require It

Lenders and lessors won’t negotiate on this requirement. If you financed your truck through a bank or leasing company, your loan agreement mandates physical damage coverage at actual cash value until the debt is paid off. The lender’s name appears on your policy as a loss payee, meaning they receive payment first if a total loss occurs. Owner-operators who skip physical damage coverage violate their financing agreements and risk loan acceleration or repossession.

One Accident Can End Your Business

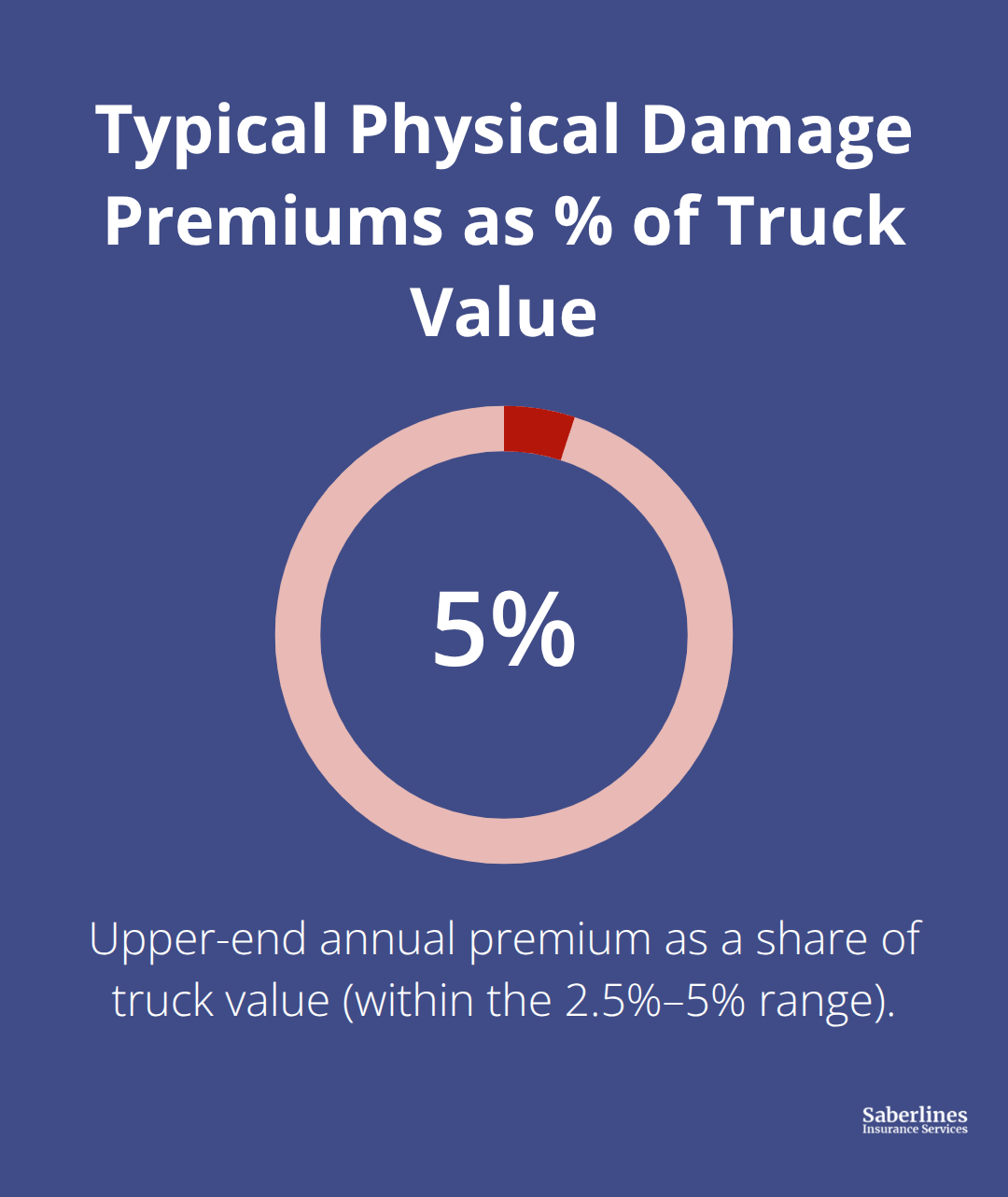

Beyond legal obligations, physical damage is simply the difference between staying in business and losing everything. The Federal Motor Carrier Safety Administration reports that average non-injury truck crashes cost approximately $47,000-enough to total many used trucks outright. A single major accident without coverage could force you to exit the industry entirely. The coverage is affordable relative to the risk; typical physical damage premiums run between $1,000 and $3,000 annually depending on your truck’s value, age, and driving history. That’s roughly 2.5 to 5 percent of your truck’s value for protection against catastrophic financial loss.

What Happens Next

Owner-operators who treat physical damage as optional rather than essential are gambling with their livelihoods on every mile driven. The next step involves understanding exactly what coverage limits and deductible options work for your specific situation-and how to avoid overpaying for protection you don’t need while ensuring you have enough when disaster strikes.

Picking the Right Coverage for Your Truck

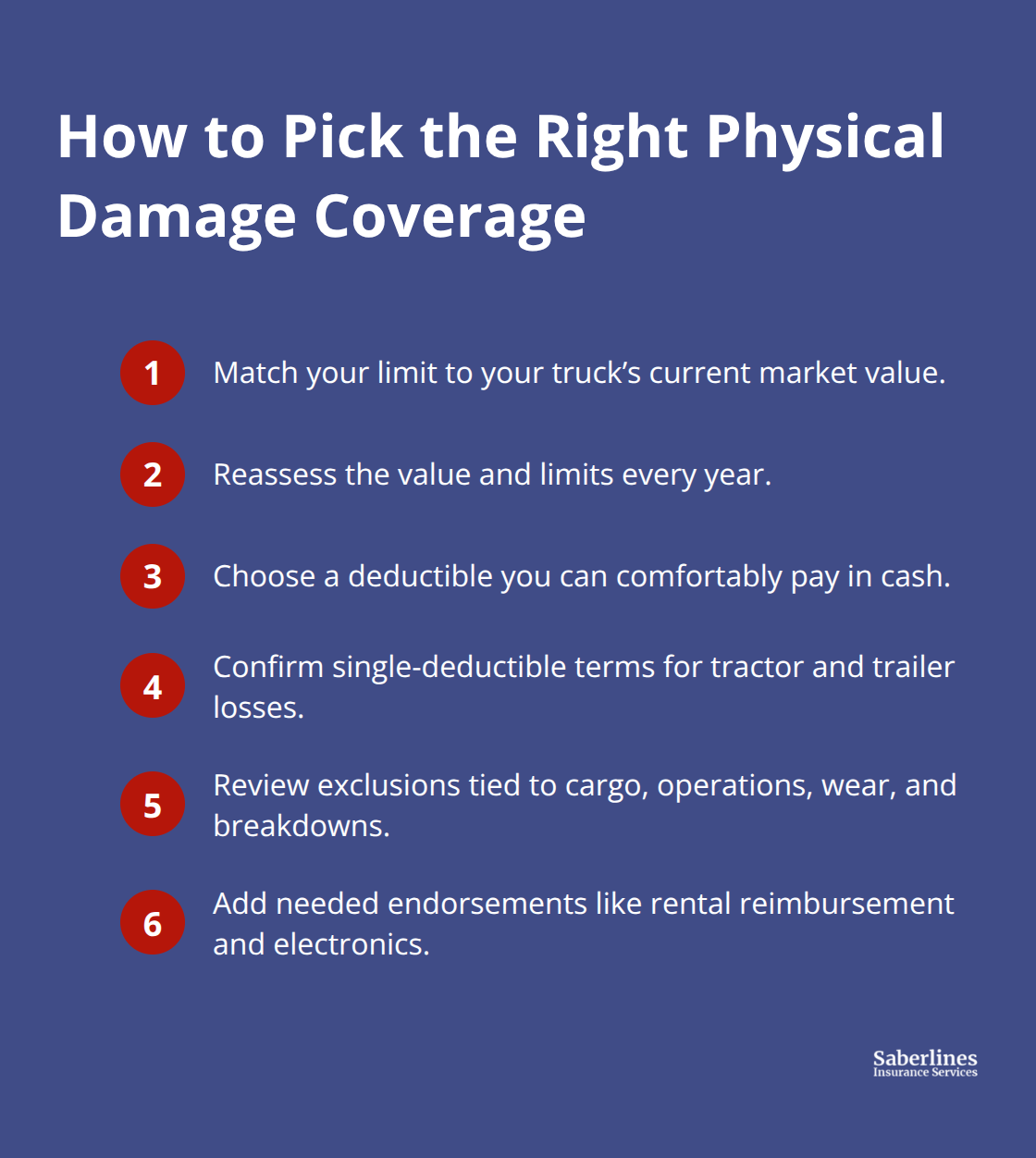

Match Your Coverage Limit to Your Truck’s Actual Value

Start with your truck’s actual market value, not the price you paid or what you think it’s worth. Pull recent sales data for your specific year, make, model, and mileage on sites like Truck Paper or NADA Guides to see what similar trucks sell for in your region. A 2018 Peterbilt 579 with 450,000 miles trades differently than one with 250,000 miles, and regional demand matters too-trucks sell for more in high-freight areas than in depressed markets. Once you have that number, that’s your coverage limit.

Setting your limit below market value leaves you short after a total loss; setting it above market value wastes premium dollars on coverage you’ll never collect. If your truck is worth $38,000, your physical damage coverage limit should be $38,000. Reassess this annually because your truck’s value drops predictably each year. A truck worth $38,000 today might be worth $34,000 in twelve months, so your coverage should track that depreciation.

Choose a Deductible You Can Actually Afford

Deductibles directly control your premium, and owner-operators often choose wrong by picking the lowest deductible available. A $500 deductible costs significantly more than a $2,500 deductible, but most owner-operators can’t absorb a $500 claim without financial strain every time they have an accident. The smarter move is choosing a deductible you can actually pay out of pocket without borrowing money or sitting idle.

If you have $3,000 in emergency reserves, a $2,500 deductible makes sense because you can pay it immediately and keep working. If you have $8,000 in reserves, a $5,000 deductible saves you hundreds in annual premium while remaining manageable. Some carriers offer deductible buyback endorsements where a small monthly fee covers your deductible at claim time, which works well if you want a low deductible without the premium hit, but read the fine print because some plans exclude certain claim types.

Your policy should also address what happens when you have multiple losses in one incident-if your tractor and trailer both suffer damage, do you pay two deductibles or one? The single deductible endorsement means you pay just your highest deductible across all vehicles in one loss, which protects you from catastrophic out-of-pocket costs when multiple units suffer damage simultaneously.

Identify Coverage Gaps and Exclusions

Policy exclusions are where coverage gaps hide, and most owner-operators never read them. Standard physical damage covers collision and comprehensive perils, but it excludes wear and tear, mechanical breakdown, and damage from illegal activities. Some policies exclude certain high-risk cargo types or specific operations like heavy haul or specialized transport.

Verify that your operation-whether you run general freight, expedited loads, or specific commodity types-falls within the policy’s defined coverage. Ask your agent directly whether your primary business activity is covered without restrictions. If you occasionally haul specialized cargo that sits outside the standard definition, that gap becomes a claim denial when you need it most.

Also confirm whether optional endorsements like electronic equipment coverage or rental reimbursement are included or cost extra, because repair shops now charge $150 to $300 per day for loaner trucks during repairs, and that cost multiplies quickly during a two-week repair cycle. Your operation changes over time-you might add trailers, shift to different cargo, or expand your service area-and your coverage should match your current reality, not last year’s business.

Final Thoughts

Physical damage trucking insurance protects your livelihood when accidents happen, and one collision costs $47,000 or more in repairs alone. Without coverage, that bill comes straight from your pocket and forces you to borrow money, sit idle, or exit the industry entirely. With coverage, you pay your deductible and return to the road within days instead of weeks.

The three decisions that matter most are matching your coverage limit to your truck’s actual market value, selecting a deductible you can afford without financial strain, and identifying gaps or exclusions that could leave you exposed. Your truck’s value drops predictably each year, so you should reassess your coverage annually to track that depreciation. Read your policy exclusions carefully because mechanical breakdowns, wear and tear, and certain cargo types won’t be covered, and if your operation has changed since you bought your policy, your coverage needs to change too.

We at Saberlines Insurance Services help owner-operators and fleets secure physical damage trucking insurance that protects assets without wasting premium dollars on unnecessary add-ons. Contact Saberlines Insurance Services to get a fast, affordable quote and discuss your coverage needs with someone who understands trucking operations.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.