Workers Compensation Coverage Options: What Small Fleets Need

Small fleet operators face a critical decision: which workers compensation coverage options actually protect their business and employees. The costs of inadequate coverage can be devastating, from medical bills to legal liability that threatens your operation.

At Saberlines Insurance Services, we’ve helped countless small fleets navigate these choices and find affordable protection. This guide breaks down the coverage types you need, how to manage costs, and why the right policy matters for your bottom line.

What Workers Compensation Actually Covers

Workers compensation covers medical expenses, lost wages, rehabilitation costs, and death benefits for employees injured or sickened on the job. According to Travelers, this coverage also protects employers from certain lawsuits related to work injuries. For small fleet operators, this means medical bills for driver injuries are handled by the insurance carrier rather than your business, and injured workers receive a portion of their lost income during recovery. The specifics vary by state, but the core protection remains consistent: if a driver gets hurt while working, workers compensation pays for their care and replaces lost earnings. Nearly all states legally require this coverage, which means operating without it exposes you to penalties, fines, and personal liability that can shut down your operation.

Why State Requirements Vary and What That Means for You

Most states mandate workers compensation for any business with employees, but a handful operate differently. In monopolistic states like Wyoming, Nevada, Ohio, and North Dakota, you must either buy coverage from a state-run fund or self-insure through a third-party administrator. This limits your options but often reduces costs since there’s no competition driving premiums up. Conversely, competitive states give you the freedom to shop between carriers, which is where small fleets gain real leverage on pricing. Some states like Utah allow certain business structures to opt out entirely-sole proprietors with no employees, partnerships with no employees, and LLCs treated as partnerships can elect not to carry coverage by obtaining a Workers Compensation Coverage Waiver through the Utah Labor Commission. However, this exemption requires meeting specific documentation requirements and only applies to the owner or partners, not to any hired drivers. For small fleets with employees, this option is irrelevant because you must carry coverage regardless of state.

Why Robust Claims Support Matters More Than You Think

Travelers data shows 70 percent of injured employees return to work within 30 days when they receive proper support and early intervention. This statistic matters because it proves that strong claims support and coordinated care reduce time away from work and lower your total costs. Carriers that invest in nurse case managers, telehealth options, and 24/7 support lines keep drivers productive faster than insurers that simply pay bills and disappear. Without this level of service, a simple back injury can linger for months, costing you far more in lost productivity than the insurance premium itself. Additionally, workers compensation includes employer’s liability protection, which shields you from lawsuits by injured workers in most situations.

How Inadequate Coverage Exposes Your Fleet to Financial Risk

Skipping workers compensation or choosing a bare-bones policy leaves your business exposed to exactly the kind of financial catastrophe that forces small fleets to close. Medical bills for a serious injury can reach tens of thousands of dollars, and without proper coverage, your business absorbs those costs directly. Legal liability from an injured worker’s lawsuit can exceed your annual revenue, especially if your policy lacks adequate employer’s liability limits. The right coverage protects both your drivers and your bottom line, which is why selecting the appropriate policy type matters far more than simply finding the cheapest option available.

Understanding what workers compensation covers is only half the battle. The real question is which coverage options actually fit your fleet’s specific risks and budget-and that’s where most small operators make costly mistakes.

Coverage Options That Protect Your Fleet

Small fleet operators must layer three distinct coverage types within workers compensation to achieve adequate protection. Each layer addresses different risks, and selecting the right combination determines whether your operation stays financially secure or faces catastrophic exposure.

Medical and Disability Benefits Form Your Foundation

The first layer covers medical expenses and lost wages-this is the foundation that most states mandate. When a driver suffers a work-related injury, medical benefits pay for emergency care, ongoing treatment, rehabilitation, and medications without caps in most states. Disability benefits replace a portion of lost wages, typically 60 to 66 percent of the employee’s average weekly earnings, for the duration of their recovery.

Travelers data shows 70 percent of injured employees return to work within 30 days when they receive coordinated care and early intervention. This statistic proves that carriers offering nurse case managers, telehealth services, and 24/7 support lines directly reduce your downtime costs. Medical bill review programs save roughly 70 percent of every medical dollar billed, making this a significant cost-containment lever that separates quality carriers from budget options. Using preferred medical providers cuts costs by up to 20 percent, offering meaningful savings for small fleets with modest safety records.

This first layer is non-negotiable-every state requires it, and skipping it exposes you to penalties and personal liability that can exceed your annual revenue.

Occupational Disease Coverage Protects Against Long-Term Exposure

The second layer addresses occupational diseases, which are illnesses contracted through work exposure rather than acute injuries. Drivers exposed to diesel fumes, extreme temperatures, or repetitive stress conditions qualify for coverage if they develop related health conditions. Many small fleet operators overlook this coverage because it seems less urgent than accident injuries, but occupational disease claims in transportation can be expensive and lengthy.

This protection matters because occupational illnesses often develop slowly and require extended medical treatment. Without this layer, your fleet absorbs the cost of treating conditions that workers developed while performing their jobs.

Employer’s Liability Protection Shields Your Assets

The third layer, employer’s liability protection, shields you from lawsuits by injured workers in situations where traditional workers compensation might not apply or where damages exceed standard benefit limits. This coverage protects your business assets and personal finances when an injured employee claims negligence or sues for additional damages beyond what workers compensation provides.

Treat employer’s liability as essential, not optional-the cost difference is minimal, but the protection is substantial. Most carriers bundle these three layers into a single policy, so your decision isn’t about selecting individual components but rather choosing a carrier that delivers strong claims support, cost management tools, and state-specific expertise.

Policy Structures That Match Your Fleet’s Financial Position

Guaranteed cost policies work well for small to medium fleets with stable operations and predictable payrolls. Large deductible plans suit financially stable operations willing to retain more risk in exchange for lower premiums. The structure you select depends on your fleet’s cash flow, loss history, and risk tolerance.

Your next step involves understanding which factors actually drive your premium costs and how to control them without sacrificing the protection your drivers and business need.

What Actually Drives Your Workers Compensation Premium

Your premium isn’t some mystery number pulled from thin air. Location, payroll size, job duties, and claims history determine roughly 80 percent of what you’ll pay. A driver in California pays substantially more than one in Texas due to state benefit structures and cost-of-living adjustments that vary wildly. Your total payroll matters because carriers calculate exposure based on how many drivers you employ and their average wages. A fleet with five drivers earning $50,000 annually versus five drivers earning $70,000 will see measurably different premiums. Your claims history is the single most controllable factor. A fleet with zero claims over three years qualifies for experience modification rates that cut premiums by 10 to 25 percent, while a fleet with frequent claims pays surcharges that compound annually. The type of work your drivers perform also shifts costs significantly. Long-haul interstate drivers face different risk profiles than local delivery drivers, and some carriers charge premiums based on whether your fleet operates primarily on highways or in urban areas.

Location and Payroll Structure Set Your Baseline Costs

State regulations and benefit structures create the foundation of your premium calculation. California’s generous benefit caps and cost-of-living adjustments produce substantially higher premiums than Texas, where benefit structures remain more conservative. Your payroll directly influences exposure calculations-a fleet with ten drivers earning $60,000 annually carries different risk than one with five drivers earning $80,000. Carriers assess total payroll exposure and adjust premiums accordingly. Understanding these baseline factors means you can anticipate cost differences before requesting quotes, rather than treating premium variations as random or unfair.

Claims History and Experience Modification Rates Control Your Destiny

Your claims history is the single most controllable premium factor. A fleet with zero claims over three years qualifies for experience modification rates that cut premiums by 10 to 25 percent, while a fleet with frequent claims pays surcharges that compound annually. This reality means that investing in safety and injury prevention directly reduces your insurance costs over time. Each claim you avoid improves your modification rate and strengthens your negotiating position with carriers at renewal time. Fleets that treat claims prevention as a business priority, not just a safety concern, see measurable premium reductions within two to three years.

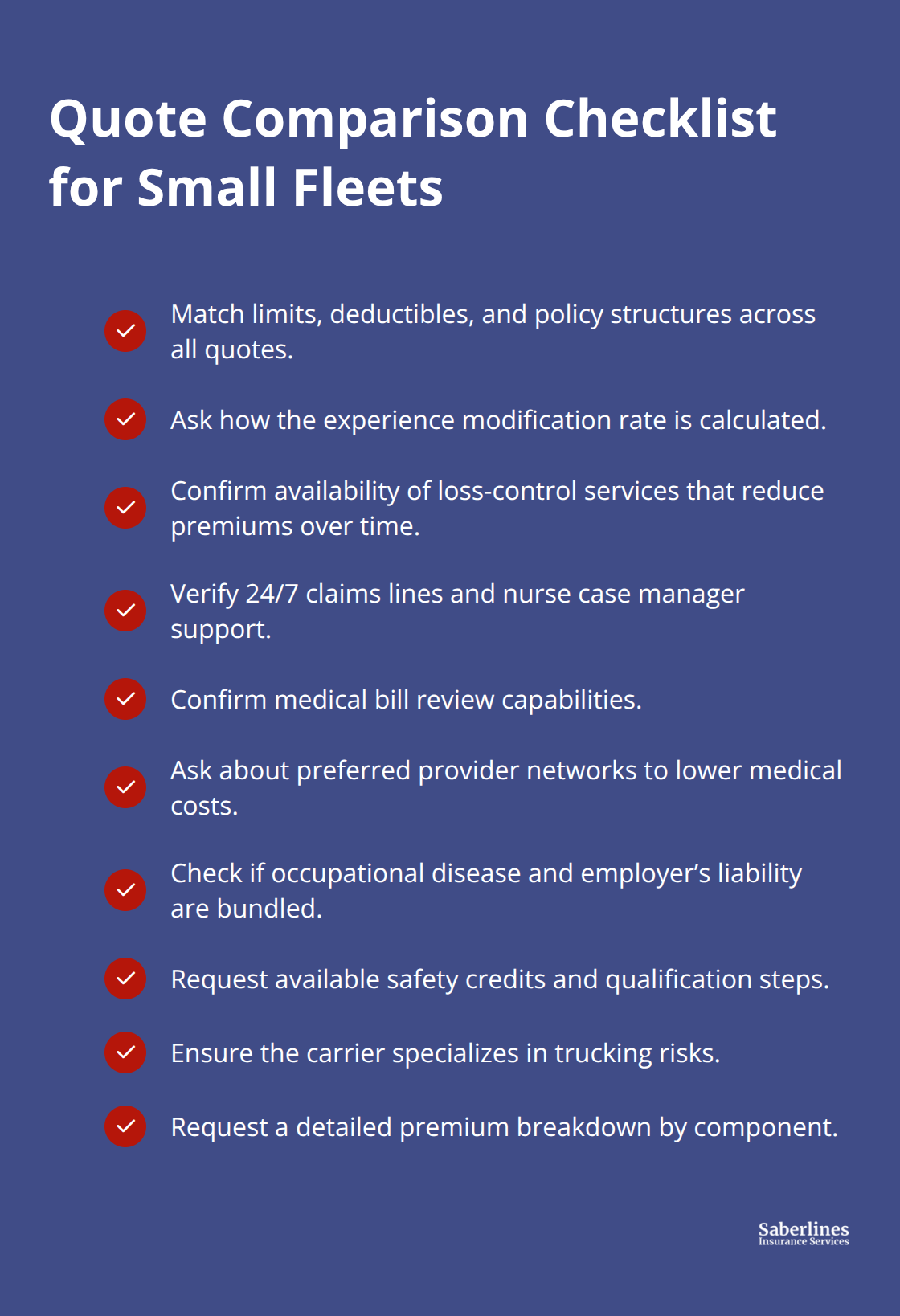

Comparing Quotes Requires Asking the Right Questions

Most small fleet operators request three quotes, compare the premium numbers, and select the lowest price. This approach guarantees you’ll overpay for coverage that doesn’t fit your operation. Instead, request quotes that include identical coverage limits, deductibles, and policy structures so you’re actually comparing apples to apples. Ask each carrier about their experience modification calculation and whether they offer loss-control services that reduce your premium over time.

Request details about their claims handling process, specifically whether they staff 24/7 claims lines and assign nurse case managers to serious injuries. Inquire about medical bill review capabilities and whether they use preferred provider networks that reduce costs. Some carriers bundle occupational disease coverage and employer’s liability at no additional charge, while others charge separately. A quote that appears $200 monthly cheaper might exclude occupational disease coverage entirely, making the actual comparison misleading. Ask about safety credits available in your state. Some carriers offer 5 to 10 percent discounts for completing specific training programs or maintaining certified safety records. Verify whether the carrier serves trucking operations specifically or treats transportation as a secondary line of business. Carriers focused on trucking typically understand industry-specific risks better and offer more tailored solutions than generalist insurers. Request a detailed breakdown showing what each component of the premium covers, not just a single lump sum. This transparency reveals where each carrier’s priorities lie and whether their pricing structure matches your fleet’s actual risk profile.

Safety Programs Transform Premium Costs and Claim Outcomes

Travelers data shows that medical bill review alone saves roughly 70 percent of every medical dollar billed, but this savings only occurs if your carrier actively manages claims rather than passively paying invoices. Fleets that invest in driver training programs specifically focused on injury prevention see measurable premium reductions because carriers track safety metrics and reward low-loss operations with better rates. The Truckers’ Injury Prevention System (TIPS) provides industry-specific resources that address the exact hazards your drivers face daily, from proper lifting techniques to vehicle maintenance protocols that prevent accidents. Implementing a formal safety program demonstrates to carriers that your operation takes risk management seriously, which directly influences your renewal rates and experience modification calculations. Fleets report injuries promptly and document incident details thoroughly to reduce claim severity because early intervention prevents minor issues from becoming expensive medical situations. A driver with back pain who receives immediate telehealth evaluation and ergonomic training costs far less than one who waits two weeks before seeking care, at which point the condition has worsened. Carriers offering 24/7 nurse lines enable your drivers to receive immediate guidance on work-related health concerns, preventing unnecessary emergency room visits and reducing claim costs. Wellbeing support programs addressing psychosocial challenges reduce time away from work by up to 20 percent according to Travelers, meaning mental health resources aren’t luxuries but cost-reduction tools that directly impact your bottom line.

Final Thoughts

Your workers compensation coverage options determine whether your small fleet operates with confidence or carries constant financial risk. The three-layer protection model-medical and disability benefits, occupational disease coverage, and employer’s liability-addresses the full spectrum of work-related injuries your drivers face. Skipping any layer exposes your business to costs that exceed your annual revenue, so selecting the right carrier matters far more than negotiating the lowest premium.

A generalist insurer treating transportation as a secondary business won’t understand the specific hazards your drivers face or offer industry-tailored solutions that reduce your total cost of risk. Carriers focused on trucking operations provide access to resources like the Truckers’ Injury Prevention System, nurse case managers who coordinate care immediately after injuries, and preferred provider networks that cut medical costs by up to 20 percent. Request quotes with identical coverage structures so you compare protection levels rather than premium numbers alone, and ask each carrier about their claims handling capabilities, medical bill review programs, and 24/7 support availability.

Your claims history is the single most controllable factor affecting your premium, which means investing in driver safety training and injury prevention directly reduces what you’ll pay over time. Contact Saberlines Insurance Services to discuss which workers compensation coverage options fit your fleet’s specific situation and budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.