Small Contractor Insurance Package: Bundle Coverage for Efficiency

Most contractors juggle multiple insurance policies without realizing they’re overpaying and creating unnecessary headaches. A small contractor insurance package bundles your essential coverage into one streamlined solution that saves money and simplifies administration.

At Saberlines Insurance Services, we’ve seen firsthand how the right package protects your business while cutting through the complexity. Read on to discover what belongs in your coverage and where most contractors leave themselves exposed.

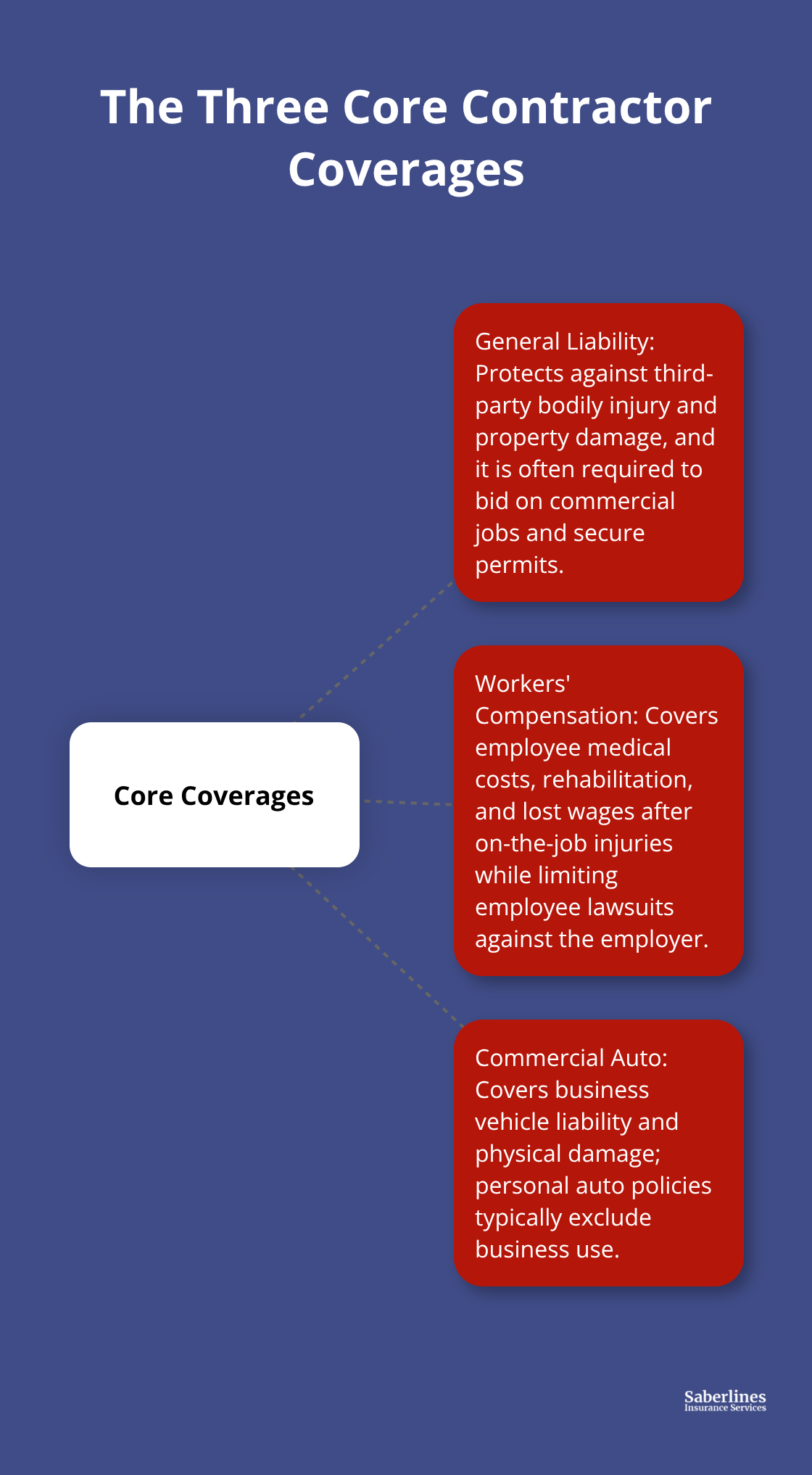

The Three Coverages Every Contractor Needs

General liability coverage forms the foundation of any contractor’s insurance program, protecting you when your work injures someone or damages their property. This coverage pays for medical bills, legal defense, and settlements if a client or third party sues you. General liability typically costs between $500 and $3,000 annually for small contractors, though premiums vary based on your trade, project size, and location. The coverage applies to bodily injury and property damage claims that arise from your operations, but it explicitly excludes employee injuries-which is where workers’ compensation becomes essential.

Without general liability, you cannot bid on most commercial projects, secure permits, or satisfy client contracts that require proof of insurance.

Workers’ Compensation Protects Your Team and Your Business

Workers’ compensation is legally required in most states the moment you hire your first employee, and it covers medical costs, rehabilitation, and lost wages when an employee gets injured on the job. This coverage also protects you from direct lawsuits by employees since they typically cannot sue their employer for work-related injuries when workers’ comp is in place. Premiums are calculated based on your payroll and job classification-a carpenter pays more than an office administrator because the risk profile differs. Many contractors underestimate this cost during the quoting phase, but skipping it exposes you to catastrophic liability and state penalties. The investment in workers’ comp directly reduces your exposure to expensive employee litigation and demonstrates professional responsibility to clients and lenders.

Commercial Auto Insurance Covers Vehicles Used for Business

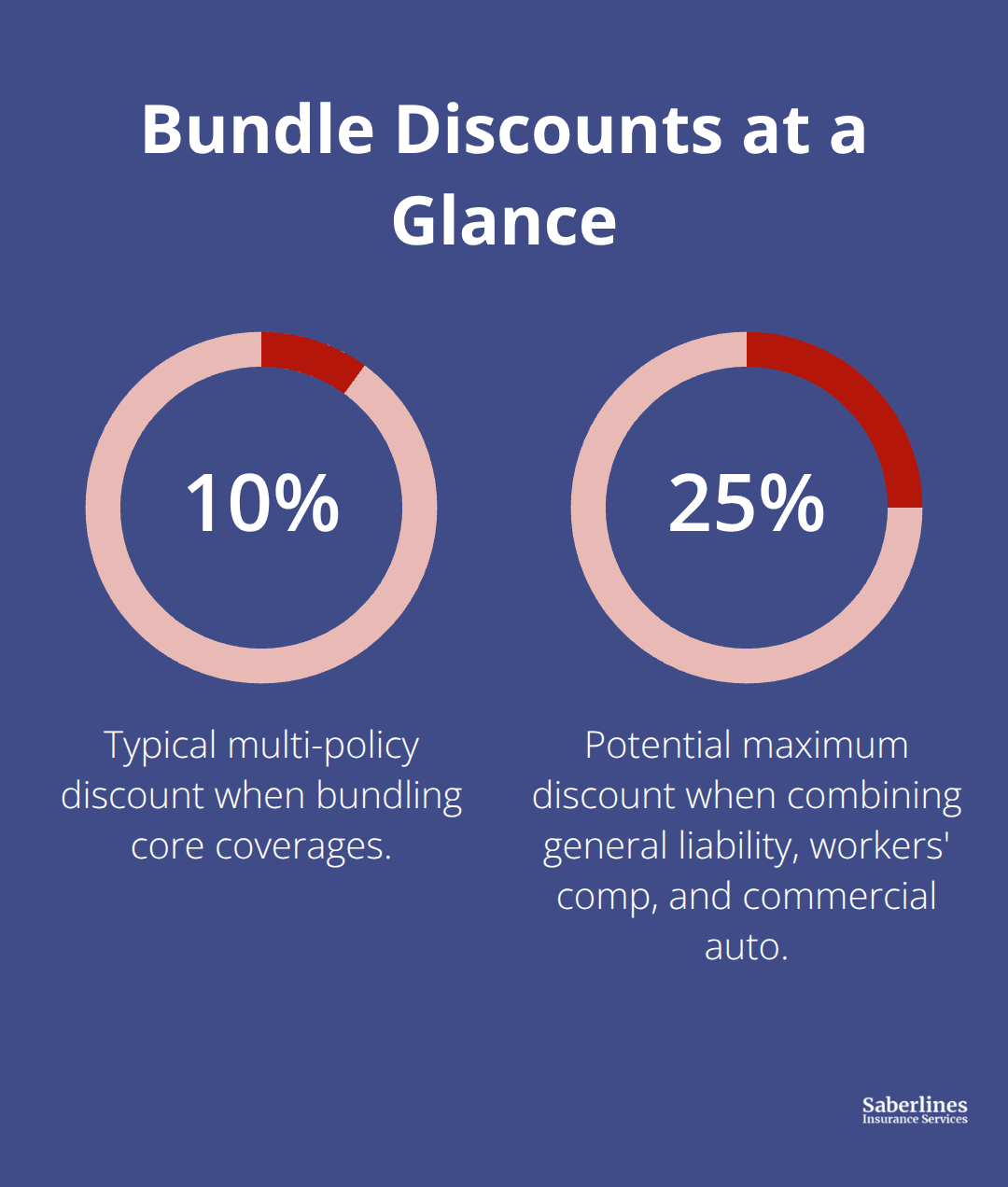

Commercial auto insurance protects your business vehicles and drivers when they operate for work-related purposes. Standard personal auto policies exclude business use, leaving you completely exposed if a company vehicle causes an accident while traveling to a job site or hauling materials. Commercial auto covers liability for injuries and property damage you cause, plus physical damage to your own vehicles from collision, theft, or weather. For contractors with multiple vehicles, bundling commercial auto with general liability and workers’ compensation typically yields discounts ranging from 10 to 25 percent compared to purchasing policies separately.

Why a Single Carrier Simplifies Everything

A single carrier managing all three coverages means one renewal date, one billing statement, and one point of contact when claims arise-this operational simplicity frees your time to focus on growing the business rather than managing insurance paperwork. You avoid the confusion that comes with multiple insurers, each with different coverage terms and claim procedures. When one company handles your entire package, the claims process moves faster because all your coverage information sits in one place, and the carrier understands your full risk profile. This alignment also reduces the risk that coverage gaps slip through the cracks between separate policies.

How Bundling Cuts Costs and Simplifies Operations

Discounts That Add Up Fast

Bundling contractor insurance policies under a single carrier typically yields discounts ranging from 10 to 25 percent compared to purchasing general liability, workers’ compensation, and commercial auto separately. Travelers’ internal retention analysis from May 2022 showed that multiline policyholders stay up to two years longer than single-policy customers, suggesting the financial and operational benefits are real enough to influence loyalty.

The discount mechanism works because insurers reduce their administrative overhead when managing one bundled account instead of three separate ones, and they pass a portion of those savings to you. For a contractor paying $1,500 annually for individual policies, a 15 percent bundle discount translates to $225 in immediate annual savings.

Eliminate Overlapping Coverage

Bundling prevents you from paying twice for the same protection. Equipment protection, for example, can be embedded within a general liability bundle rather than purchased as a standalone policy. This consolidation removes redundant coverage that wastes money and leaves your protection cleaner and more efficient.

Streamline Your Billing and Renewals

Consolidating your policies transforms how you manage billing and claims. A single renewal date instead of three means you spend less time tracking expiration dates and less risk of accidentally letting coverage lapse between different policy anniversaries. One billing statement replaces three separate invoices, cutting the administrative clutter that distracts you from actual work.

Speed Up Claims Resolution

When a claim occurs, a single carrier understands your complete risk profile across all three coverage areas, so the investigation moves faster and decisions are made with full context rather than a carrier reviewing just one isolated policy. You work with one contact person who knows your business inside and out instead of juggling multiple claims departments. This operational simplicity directly impacts your bottom line by reducing the hours spent on insurance management that could otherwise go toward bidding jobs or completing projects.

What Coverage Gaps Actually Cost You

Most contractors don’t realize that general liability, workers’ compensation, and commercial auto leave significant exposures unprotected. Equipment sitting on job sites, hired vehicles, and trade-specific risks like pollution liability fall outside these three core coverages-and that’s where many contractors discover expensive gaps when claims happen.

Common Coverage Gaps Contractors Miss

Your three core policies cover the obvious exposures, but contractors routinely face claims outside general liability, workers’ compensation, and commercial auto. Tools vanish from job sites, vehicles you rent for specific projects, and trade-specific environmental risks represent genuine financial threats that standard bundled packages don’t address.

A contractor using a rented excavator on a demolition project has zero protection if that equipment sustains damage unless hired equipment coverage exists in the policy. Similarly, a landscaper applying herbicides or a concrete contractor working near water sources faces pollution liability claims that general liability explicitly excludes. These gaps aren’t theoretical-they’re the exact scenarios that force contractors into out-of-pocket settlements.

Tools and Equipment Need Separate Protection

Portable tools and equipment sitting on job sites vanish regularly. A carpenter’s $8,000 air compressor, a plumber’s diagnostic equipment, or a mason’s power tools left overnight attract theft and weather damage that standard property policies won’t cover because those policies exclude mobile equipment. Inland marine coverage, sometimes called tools and equipment insurance, protects your portable inventory during transit and at job sites from theft, fire, storms, and accidental damage. For contractors with equipment valued above $5,000, this coverage typically costs $300 to $800 annually depending on your trade and security practices. The math is straightforward: if you lose a single expensive tool or piece of equipment, you’ve paid for years of inland marine coverage. Document your equipment inventory with photos and serial numbers to make claims faster and help you qualify for better rates.

Rented and Borrowed Equipment Creates Hidden Exposure

When you hire equipment for a specific project-a crane, excavator, or scaffolding-your general liability policy doesn’t protect you if that rented equipment sustains damage. The equipment owner will pursue you for repair or replacement costs, which can easily reach $5,000 to $15,000 for heavy machinery. Hired equipment coverage extends your protection to rented and borrowed tools so you’re not personally liable for damage that occurs during normal operations. This endorsement costs minimal additional premium, often $100 to $300 annually, but it eliminates a major financial exposure that catches contractors off guard. When you quote a project that requires rented equipment, verify this coverage exists before you sign the rental agreement.

Pollution Liability Protects Specific Trades

Environmental claims destroy contractors who don’t anticipate them. Landscapers applying pesticides or fertilizers, concrete contractors working near streams, remediation crews, and anyone handling hazardous materials face pollution liability exposure that general liability explicitly excludes. A single spill into groundwater or a chemical runoff claim can cost $50,000 to $250,000 in cleanup and third-party liability. Pollution liability insurance is trade-specific and not standard in bundled packages, so you must request it during quoting if your work involves chemicals, fuel, or proximity to water or soil. Contractors in California doing environmental work or hazardous material remediation should prioritize this coverage because state regulations are strict and penalties for environmental violations are substantial.

Final Thoughts

A small contractor insurance package that bundles general liability, workers’ compensation, and commercial auto delivers immediate financial and operational wins. You save 10 to 25 percent through multiline discounts, consolidate billing into one statement, and eliminate the administrative chaos of managing three separate policies with different renewal dates. A single carrier means faster claims resolution because one contact person understands your complete risk profile instead of juggling multiple departments.

The real protection comes from recognizing where standard bundles fall short. Equipment theft, hired machinery damage, and pollution liability represent genuine financial threats that catch unprepared contractors off guard. Before you finalize coverage, audit your actual operations: What equipment sits on job sites? Do you rent machinery regularly? Does your trade involve chemicals or environmental exposure?

Getting a quote is straightforward. We at Saberlines Insurance Services specialize in commercial insurance and can help you build a small contractor insurance package tailored to your specific trade and project mix. Reach out with details about your operations, equipment value, and the types of projects you typically handle.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.