General Liability Premium Estimates: How Much Will Your Policy Cost?

General liability premium estimates vary wildly depending on your business type, size, and track record. A construction company might pay $500 annually while a retail operation pays $1,200 for similar coverage.

At Saberlines Insurance Services, we’ve seen businesses overpay by thousands simply because they didn’t understand what drives their costs. This guide breaks down exactly what insurers look at and how you can reduce what you pay.

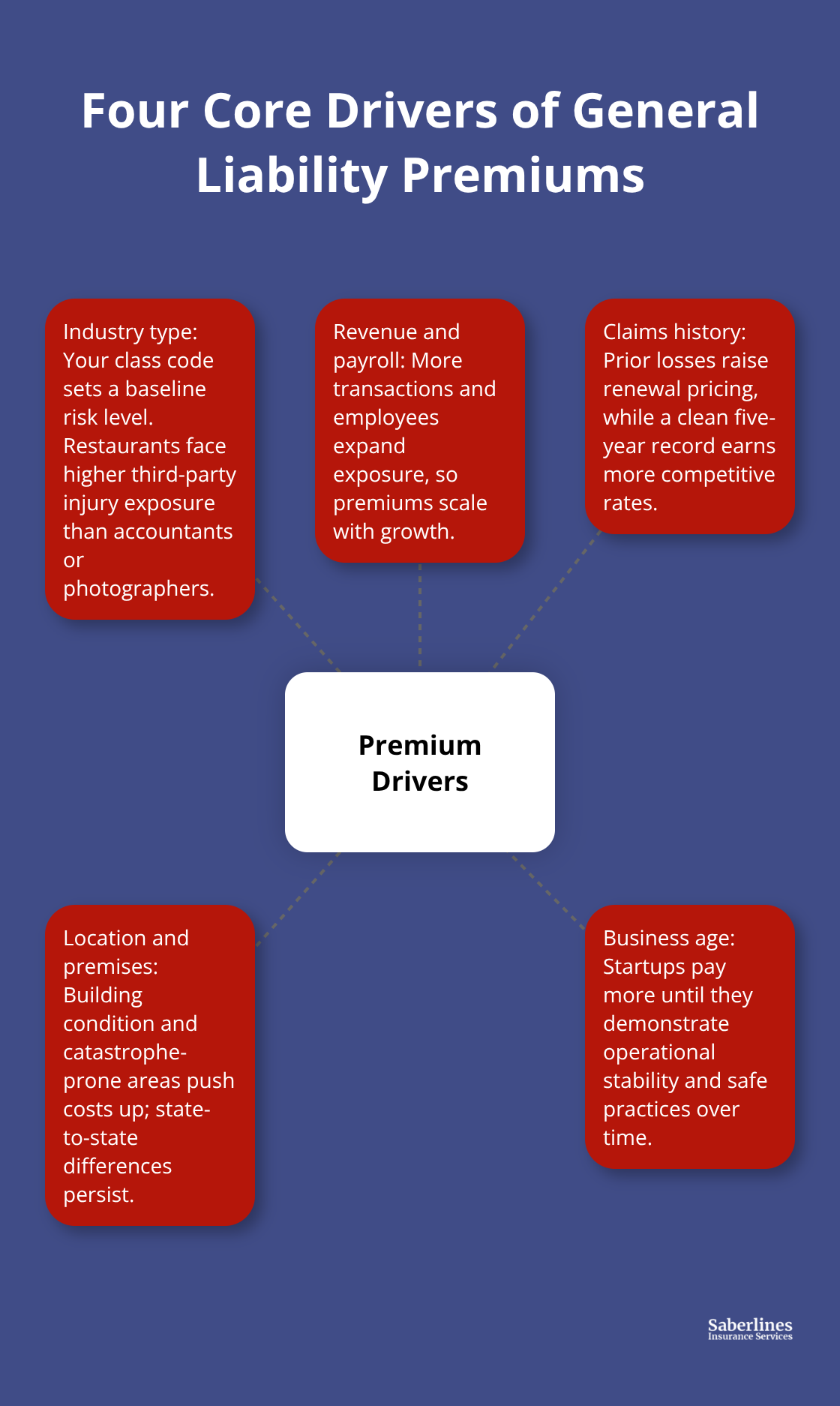

What Actually Drives Your Premiums

Industry Type Sets Your Baseline Cost

Your industry determines your baseline risk in ways most business owners don’t fully grasp. A restaurant operator pays roughly $1,352 annually according to The Hartford data, while an accountant in the same region pays $604. The difference isn’t arbitrary-it reflects the actual probability that someone gets hurt or property gets damaged in that business type. Restaurants have equipment, food safety risks, and customer foot traffic that create injury exposure. Accountants work in offices with minimal third-party contact. The Hartford’s data shows photographers at $421 annually and engineers at $500, demonstrating how dramatically risk classification shifts your cost. Your business class code is what insurers use to categorize you into these risk brackets, and challenging an incorrect code can sometimes save hundreds.

Revenue and Payroll Expand Your Exposure

Higher revenue typically means more customer interactions, more transactions, and more opportunities for something to go wrong. A construction company with $2 million in annual revenue will pay more than one with $500,000 because the volume of work creates proportionally higher exposure. The Hartford reports that payroll size matters particularly for workers’ compensation within general liability bundled policies, and employee count affects your overall risk profile. If you scale your business, expect your general liability premium to increase with that growth-not as punishment, but as a mathematical reflection of your expanded exposure.

Claims History Acts as Your Financial Report Card

Your past claims are the single most predictive factor insurers use to price your policy. One serious claim can raise your premium by 20-40% on renewal, and multiple claims within a few years can make coverage expensive or hard to find. Insurers treat your loss history like a credit score-they bet on your future behavior based on your track record. A clean five-year history signals you manage risk well and deserve competitive rates. If you had a claim three years ago, that still affects your pricing, though its impact diminishes over time.

Location and Premises Condition Matter More Than You Think

Your premises condition and operations shape your premium significantly. Whether you rent versus own, whether your building is old or new, whether you maintain safety equipment-these operational realities change your premium. Catastrophe-prone locations like high-hazard flood or wildfire zones push costs up significantly because the underlying risk is genuinely higher. A retail store in California pays roughly $42 per month while one in Florida pays $55 monthly for similar coverage, according to Insureon data. This geographic premium variance reflects both natural disaster risk and local claims patterns.

Business Age Influences Underwriting Decisions

Your business’s years in operation also factor in-startup businesses typically face higher premiums because they lack a loss history to prove competence, while established operations with clean records negotiate better terms. Insurers view newer businesses as higher risk until they demonstrate operational stability and safe practices over time. Understanding these four factors-industry type, revenue, claims history, and location-positions you to anticipate what your quote will look like and identify where you can improve your risk profile before you apply for coverage.

General Liability Premium Ranges by Industry

Construction and Trades Command the Highest Costs

Construction and trades businesses face the steepest general liability premiums because the work itself creates constant injury and property damage risk. A construction company pays roughly $500 annually according to industry data, but that represents the floor-general contractors who manage multiple crews and subcontractors often pay $1,000 to $3,000 annually depending on revenue and claims history. The Hartford reports that manufacturers pay $617 annually on average, reflecting similar exposure from equipment, materials handling, and worker proximity to hazards. Engineering firms sit lower at $500 annually because the risk concentrates on design liability rather than physical site work. Your premium in trades reflects not just what could happen, but what statistically does happen in your industry-and those statistics justify higher costs.

Retail and Food Service Split Into Two Tiers

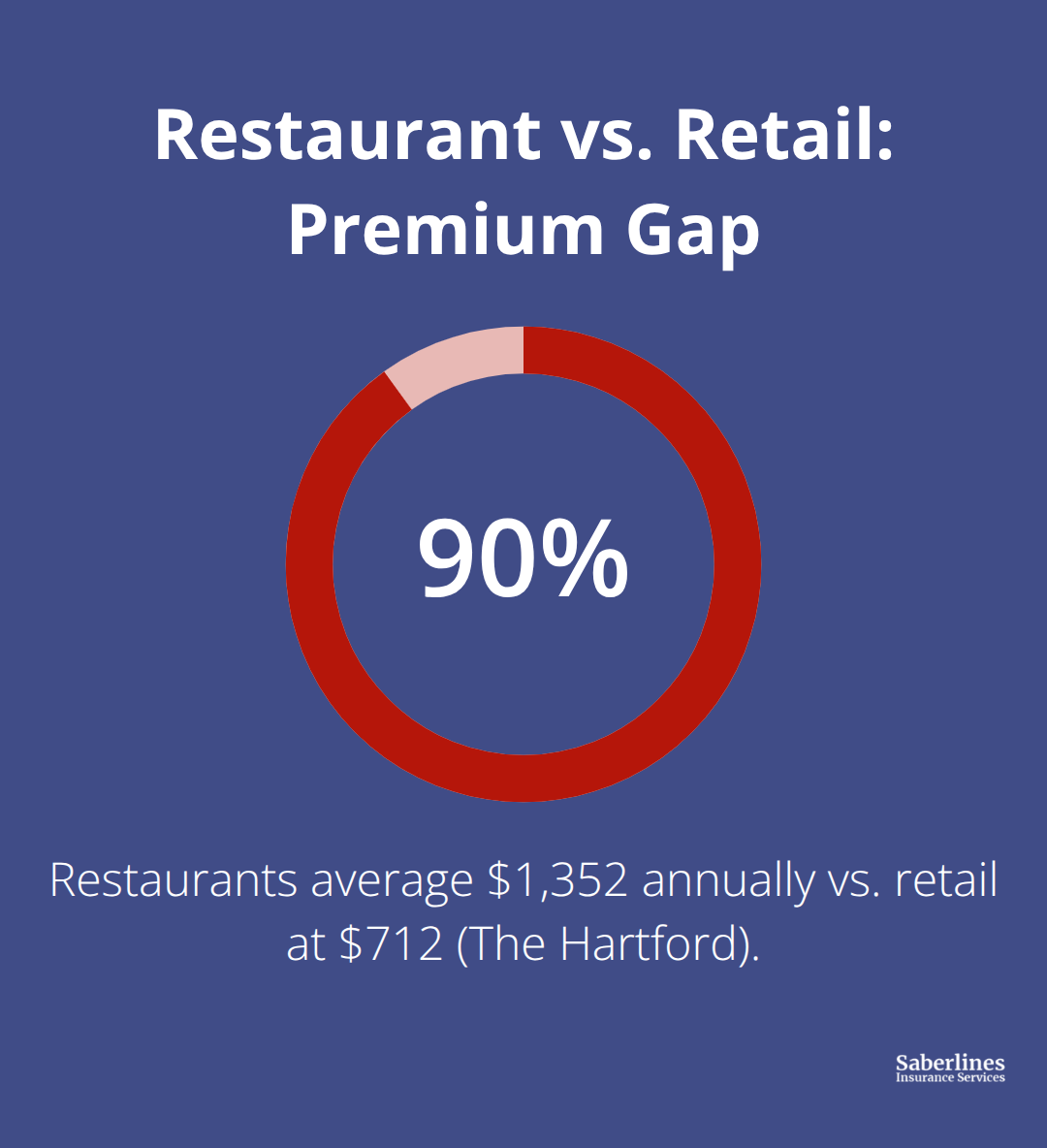

Retail and food service operations occupy the middle ground, but restaurants significantly outpace general retail. The Hartford data shows restaurants at $1,352 annually while retail stores average $712, a 90% difference driven by equipment risk, food safety exposure, and customer volume.

A coffee shop might pay around $47 monthly according to Insureon data, while a full-service restaurant with kitchen equipment and higher traffic easily exceeds $100 monthly. Location amplifies these costs dramatically-a restaurant in Florida pays roughly $55 monthly compared to $42 in California for the same coverage, reflecting regional claims patterns and catastrophe exposure.

Professional Services Operate at the Lowest End

Professional services like accounting, consulting, and photography operate at the lowest end of the spectrum. Accountants pay $604 annually, consultants $720, and photographers just $421 according to The Hartford, because their exposure comes primarily from professional liability rather than physical premises risk. An IT consultant working from home might pay only $32 monthly because the business operates with minimal customer contact and no equipment hazards. Your premium in professional services reflects genuinely lower risk-you should expect quotes in the $300 to $900 annual range unless your specific services create unusual exposure.

Geographic Variation Persists Across All Industries

Geographic differences matter significantly across all industries. Texas businesses pay roughly $43 monthly while Colorado businesses pay $54 for similar coverage, and these differences persist whether you operate in construction, retail, or professional services. State-specific claims data, regulatory environments, and natural disaster exposure drive this variance rather than random pricing. Understanding your industry baseline and geographic premium helps you anticipate your actual costs and identify where you can strengthen your risk profile before requesting quotes.

How to Lower Your General Liability Insurance Premiums

Document Your Safety Practices to Prove Risk Management

Safety documentation changes what insurers will pay for your coverage more directly than almost any other factor. Insurers now expect baseline evidence of risk management before they offer competitive rates, and businesses that submit maintenance schedules, safety training records, and incident tracking systems negotiate better terms consistently. The Hartford data shows that robust risk controls improve underwriting posture, meaning insurers view your business as lower-risk and price accordingly.

If you operate in construction or manufacturing, document every safety inspection, equipment maintenance log, and employee training session. Photograph your premises regularly to show upkeep and hazard removal. When you request a quote, include this documentation unprompted-it signals you take risk seriously and deserve better pricing. Restaurants that maintain daily equipment inspection logs and food safety certifications pay less than those without documentation. The difference between a business that can prove its safety practices and one that cannot often runs 15-25% on renewal quotes.

Build Your Documentation Before You Shop for Coverage

Start building your safety documentation now regardless of when your policy renews. Waiting until you shop for new coverage puts you at a disadvantage because you’ll lack the track record insurers want to see. Maintenance logs, training certificates, and incident reports accumulated over months demonstrate genuine commitment to risk reduction. Insurers reward this evidence with better pricing and terms because it predicts lower future claims.

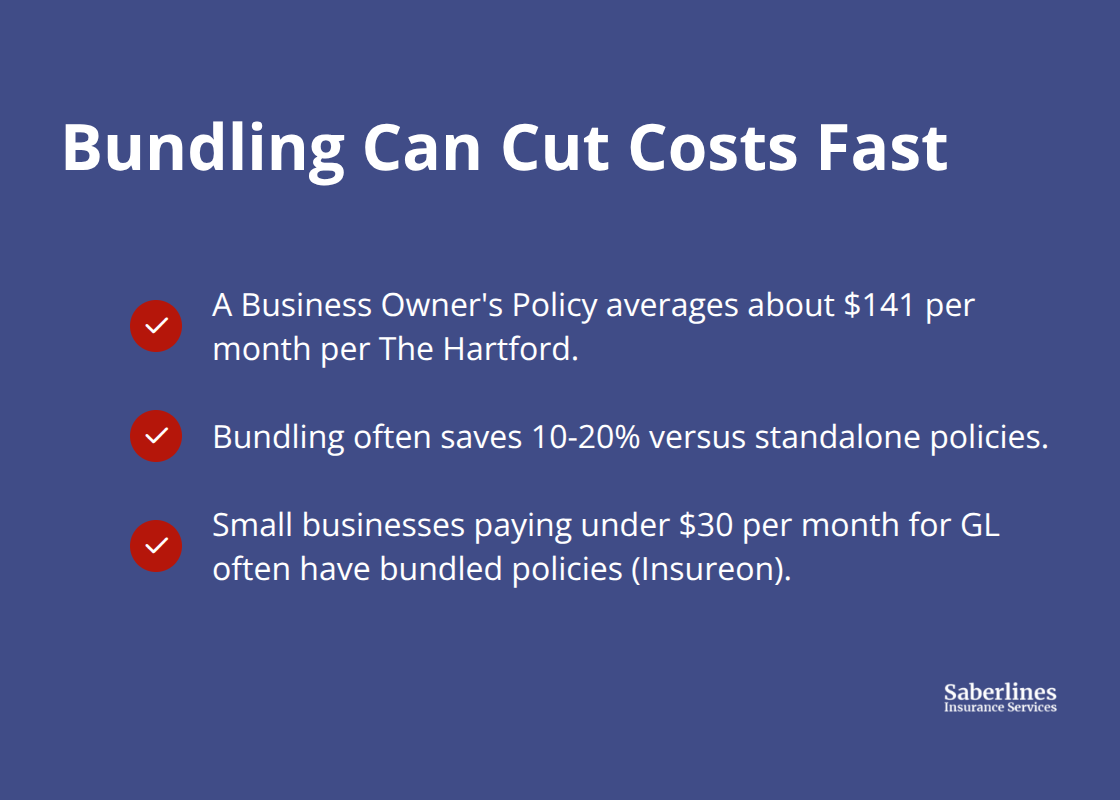

Bundle Policies to Unlock Immediate Savings

Policy bundling delivers the most straightforward premium reduction available. The Hartford reports that a Business Owner’s Policy combining general liability, commercial property, and business income costs about $141 monthly, while purchasing those same coverages separately would cost substantially more. Bundling typically saves 10-20% compared to standalone policies, and the savings compound when you add additional lines like workers’ compensation or commercial auto.

If you operate vehicles for business, commercial auto bundled with your general liability costs less than either policy alone. Insureon data shows that small businesses paying under $30 monthly for general liability often have bundled policies rather than standalone coverage. When you request quotes, always ask carriers for bundled pricing on every combination of coverage your business needs-don’t accept quotes on individual policies without comparing bundle options.

Leverage Your Claims History to Negotiate Better Terms

Your claims history determines whether you qualify for the best bundled rates, but even businesses with one or two prior claims find better terms through bundling than through standalone policies. The 2026 market shows that insurers reward bundled customers with better terms because multi-line relationships reduce their administrative costs and improve risk visibility across your entire operation. A clean loss history combined with bundled coverage positions you for the most competitive pricing available in the current market.

Final Thoughts

Your general liability premium estimates hinge on four core factors: industry type, revenue volume, claims history, and location. Understanding these drivers allows you to anticipate your costs and identify where you can strengthen your risk profile before requesting quotes. Start building safety records, maintenance logs, and training certificates now rather than waiting until your policy renews, since insurers reward businesses that demonstrate genuine risk management with better pricing and terms.

Always request bundled quotes that combine general liability with commercial property, workers’ compensation, or other coverages your business needs, as bundling typically saves 10-20% compared to purchasing policies separately. Submit complete information about your operations when you request quotes, including your current safety programs, maintenance schedules, and loss history, since the more detail you provide, the more precise your quote becomes. Shop with multiple carriers before accepting any quote, as pricing varies significantly based on how different insurers assess your specific risk profile.

We at Saberlines Insurance Services help business owners across California find competitive general liability coverage tailored to their operations and risk profiles. Contact us to request quotes and discuss your coverage needs with specialists who understand your industry’s specific exposures.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.