General Liability Policy Basics: A Simple Start to Coverage

General liability insurance protects your business from the financial fallout of accidents, injuries, and damage claims. Most business owners don’t fully understand what their policy covers-or what it doesn’t.

At Saberlines Insurance Services, we’ve seen too many companies operate with gaps in their coverage. This guide walks you through general liability policy basics so you can make informed decisions about protecting your business.

What General Liability Actually Protects

The Three Core Coverage Areas

General liability insurance covers three major categories of claims that can drain your business finances. The first is bodily injury, which means if someone gets hurt because of your business operations, your policy pays their medical bills, lost wages, and legal costs if they sue. A customer slipping on your floor, an object falling from your equipment, or someone injured during a service you provide all fall under this umbrella. According to the SBA, this coverage includes medical expenses and the costs of defending lawsuits or settlements.

The second category is property damage liability, which covers damage you cause to someone else’s property while conducting business. If your equipment damages a client’s building, your vehicle hits their fence, or your work causes structural harm, general liability pays for repairs up to your policy limits. The third category is personal and advertising injury, covering claims like libel, slander, false advertising, or copyright infringement in your marketing materials.

This protection matters more than most business owners realize because one lawsuit can cost tens of thousands in legal fees alone.

Products and Completed Operations Coverage

General liability also covers products and completed operations, meaning injuries or damages caused by products you sell or work you finish remain covered even after the customer leaves your premises. This extension protects you from liability that surfaces weeks or months after you complete a job or deliver a product. Many business owners overlook this benefit, yet it provides substantial protection for long-term exposure.

What General Liability Costs

The Hartford reports that average general liability costs around $810 per year for small businesses, though Progressive data from 2025 shows a median monthly cost of $55 with an average of $79 per month depending on your industry and risk profile. Your specific premium depends on your business type, number of employees, location, coverage limits, and claims history. A typical starting point is $1 million per occurrence and $2 million aggregate limits, which provides solid protection for most small operations.

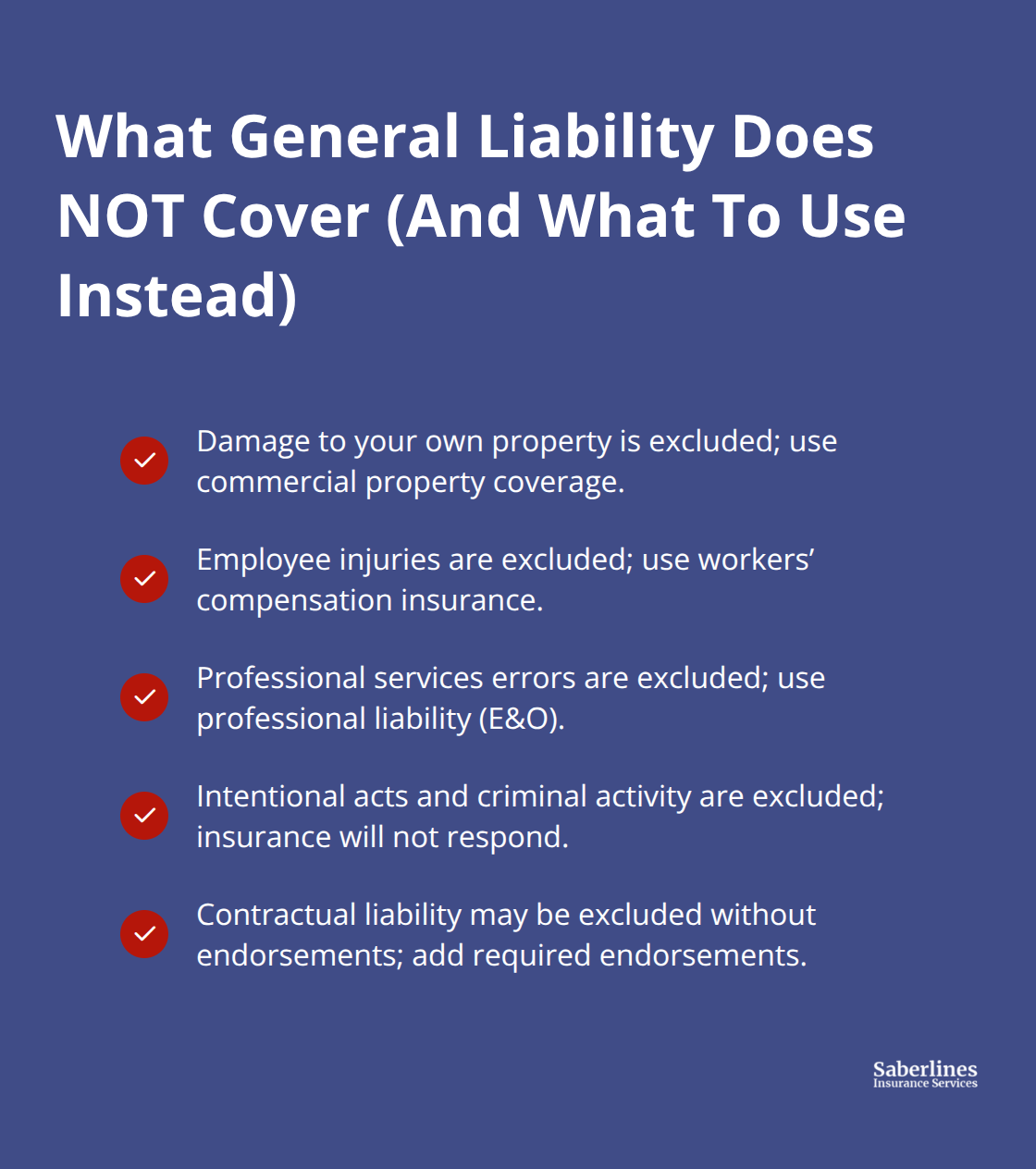

Critical Coverage Gaps to Know

General liability does not cover your own property damage, employee injuries (workers compensation handles that), professional services errors, or intentional acts. Understanding this distinction matters because many business owners mistakenly think one policy covers everything. These exclusions create gaps that other policies must fill-which is why assessing your full risk picture becomes essential before you finalize your coverage limits.

Common Exclusions and Limitations

Professional Services Errors Require Separate Coverage

General liability insurance has hard boundaries, and stepping outside those lines leaves you exposed. The most dangerous gap for many business owners is professional services errors. If you provide advice, design work, accounting services, or any specialized expertise, general liability simply does not cover mistakes in that work. A bookkeeper who miscalculates payroll taxes, a consultant who provides faulty recommendations, or a designer who misinterprets client specifications will find their general liability policy useless when a client sues for financial losses.

According to the SBA, professional liability insurance is the separate coverage that handles these errors and omissions. This distinction matters enormously because the cost of defending a professional negligence claim can easily exceed $50,000 in legal fees alone, even if the claim gets dismissed. If your business involves any professional judgment or specialized knowledge, you need to ask yourself whether general liability is sufficient or whether professional liability insurance fills a critical gap. Many service-based businesses operate for years without this protection, gambling that mistakes will not happen.

Intentional Acts and Criminal Activity Fall Outside Coverage

Intentional acts and criminal activity also fall completely outside general liability coverage. If an employee assaults someone, your business commits fraud, or you deliberately damage property, your policy will not pay. This exclusion exists because insurance cannot cover illegal behavior or willful misconduct.

Your insurer will deny any claim that stems from actions you took on purpose or that violate the law.

Contractual Liability Assumptions Need Endorsements

General liability does not automatically cover contractual liability or assumptions you make in client agreements. If a contract requires you to carry specific insurance coverage or accept liability beyond what your policy normally covers, that contractual obligation may not be covered unless you add contractual liability endorsements to your policy. Many contractors discover this problem when a property owner demands additional insured status or when a client contract requires you to defend them in lawsuits.

Without these endorsements in place, you could find yourself responsible for legal defense costs that your policy refuses to pay because the contract imposed an obligation your base policy did not assume. Reading your client contracts before quoting coverage prevents expensive surprises later. The Hartford notes that some clients require blanket additional insured endorsements before work begins, which means you must address these requirements upfront rather than after a dispute arises.

How to Choose the Right Coverage Limits

Start with What You Cannot Afford to Lose

Choosing coverage limits feels abstract until you face a real claim. The SBA’s practical rule of thumb is straightforward: insure against risks you cannot pay out of pocket if an incident occurs. This means your first step is brutal honesty about what would happen if someone sued your business tomorrow. A $1 million per occurrence and $2 million aggregate policy sounds standard, but standard does not mean right for your situation.

Match Your Industry Risk to Your Limits

If your business operates in a high-density urban area where property values are steep and foot traffic is heavy, you face different exposure than a landscaping crew in a rural region. Progressive data from 2025 shows that median general liability costs sit around $55 per month, but this baseline changes dramatically based on your industry classification, the number of employees you carry on payroll, and your location. Higher-risk professions like landscaping, construction, or food service consistently pay more because the probability of injury claims and property damage is genuinely higher.

A business that manufactures and installs equipment faces more exposure than one that only delivers it, so your premium reflects that reality.

Align Coverage Limits with Your Assets and Revenue

Your assets and revenue matter more than industry generalizations. If you own a small salon with $150,000 in annual revenue and minimal property on-site, a $1 million per occurrence limit may provide adequate breathing room. But if you operate a contracting business with crews on multiple job sites, vehicles, and equipment worth hundreds of thousands of dollars, that same limit leaves you dangerously exposed.

Review Client Contracts Before You Quote Coverage

Many contractors face contractual requirements from property owners or clients who demand you carry specific coverage limits before work begins. Progressive notes that blanket additional insured endorsements often get required, which means you must verify your client contracts upfront rather than discovering gaps after a dispute. Pull three to five recent client contracts and identify what coverage limits they actually demand, then build your policy around those real requirements rather than guessing. If your contracts consistently ask for $2 million aggregate coverage, paying slightly more for that protection beats losing clients or facing uninsured contractual liability exposure.

Account for Location and Business Age

Location matters significantly because densely populated areas with higher past claims activity typically drive up premiums, which means your coverage limits should reflect local risk patterns. Newer businesses sometimes pay higher premiums than established ones with proven safety records, so if you are still building your track record, slightly higher limits may compensate for that uncertainty and protect you while you establish operational consistency.

Final Thoughts

General liability policy basics come down to three essential truths: understand what your policy covers, identify the gaps that other insurance must fill, and match your coverage limits to your actual business exposure. Too many business owners treat general liability as a checkbox item rather than a strategic decision, accepting whatever limits their agent suggests or whatever their competitors carry, then discovering during a claim that their coverage falls short. The real work happens before you buy a policy-pull your client contracts, assess your location and industry risk honestly, and calculate what you could not afford to pay out of pocket if someone sued tomorrow.

An agent who takes time to ask questions about your business model, your client base, and your growth plans identifies coverage gaps you would miss on your own and explains which endorsements matter for your situation. Generic quotes from online tools miss critical details about your operations, your contractual obligations, and your risk exposure. A conversation with someone who understands your specific business removes the guesswork from coverage decisions.

We at Saberlines Insurance Services specialize in helping transportation businesses and owner-operators secure the coverage they actually need. We understand that general liability sits alongside other policies like commercial auto and workers compensation to create a complete protection strategy. Get a customized quote today and discover how the right coverage gives you confidence that your business is genuinely protected.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.