Truck Cargo Insurance: Safeguarding Goods From Dock to Destination

Every year, trucking companies lose millions to cargo theft, damage, and accidents. The right truck cargo insurance protects your shipments and your business from these costly risks.

At Saberlines Insurance Services, we’ve seen firsthand how the wrong coverage-or no coverage at all-can devastate a fleet’s finances. This guide walks you through what cargo insurance actually covers, why it matters, and how to pick a policy that fits your operation.

What Cargo Insurance Actually Protects

Theft and Loss Coverage

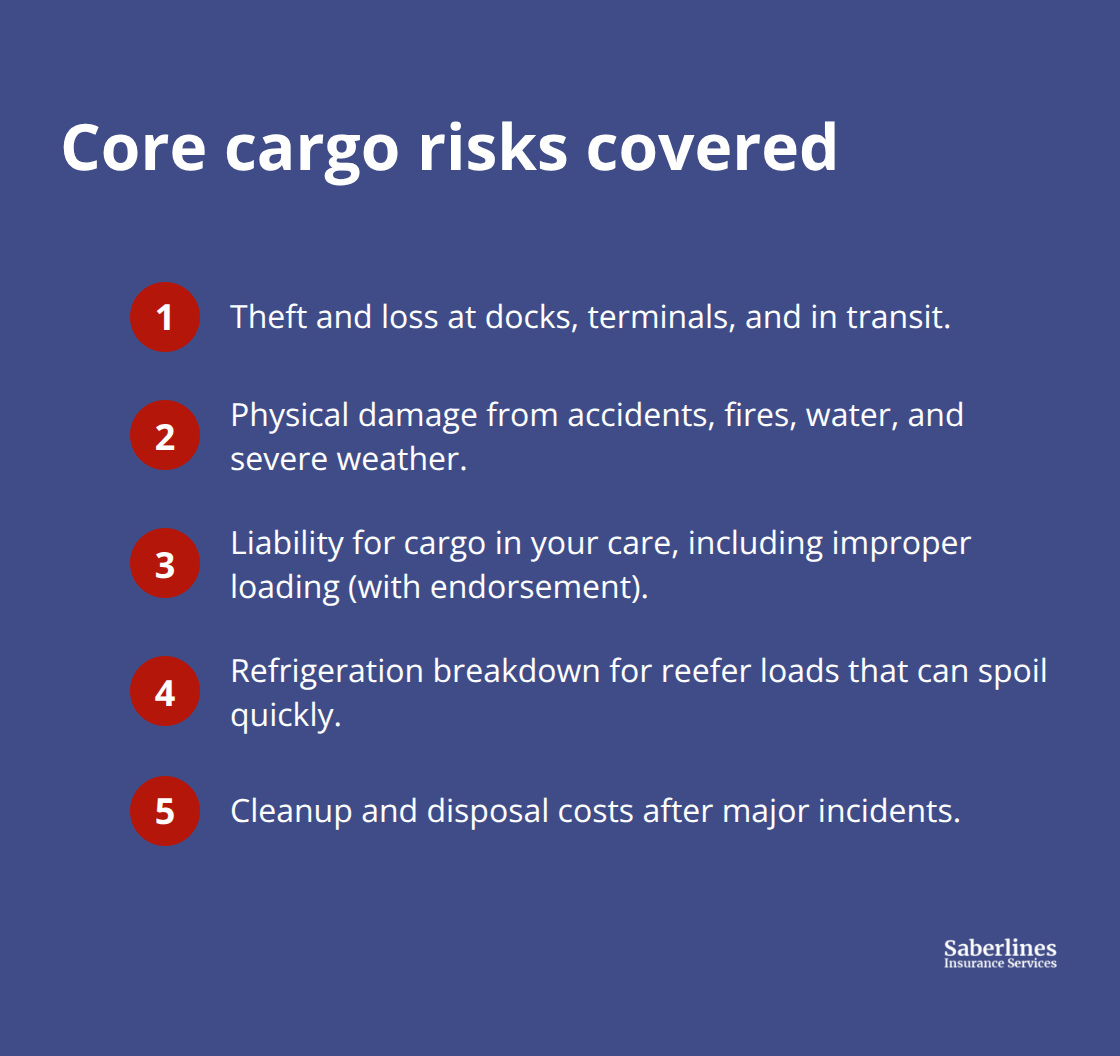

Cargo insurance protects against theft and loss while goods sit at docks, terminals, or travel across state lines. Theft remains a serious problem in trucking-cargo theft costs the industry hundreds of millions annually, with thieves targeting high-value electronics, refrigerated products, and retail freight parked in unsecured areas overnight. This coverage activates the moment you take possession of the shipment and stays active until you hand it off to the next party in the supply chain. Without it, you absorb the full financial hit when cargo vanishes from a loading dock or a parked trailer.

Physical Damage During Transport

Cargo insurance covers physical damage from accidents, equipment failure, fire, water damage, and severe weather during transport. If a trailer rolls, a reefer unit fails mid-journey, or a collision damages the shipment, this coverage pays for the loss. Refrigeration breakdown coverage is often included automatically in certain package options, which is essential for reefer loads that can spoil within hours if equipment fails. Cleanup and disposal costs after a major incident are typically covered too, preventing surprise expenses when damaged freight must be removed from the trailer.

Liability Protection for Cargo in Your Care

The policy protects you from liability claims when cargo damage occurs under your care, reducing the financial exposure that basic carrier liability alone cannot handle. Standard liability covers injuries or property damage you cause to others, not the cargo itself. If a shipper loads merchandise improperly and it shifts during transit, causing damage, you face a claim. Cargo insurance covers that loss if your policy includes improper loading as an endorsement-a detail many carriers overlook at quote time. Many brokers require a minimum cargo coverage of $100,000, with higher-value loads demanding $250,000 or more depending on freight type and contract terms.

Why Coverage Details Matter for Your Operation

The right coverage protects your reputation with shippers and brokers who evaluate carriers on reliability and professionalism. A major claim without cargo insurance can financially devastate a small fleet or owner-operator, making this coverage a vital safety net that keeps contracts active and operations solvent. Shippers evaluate carriers on reliability, safety, and professionalism, with robust coverage signaling seriousness about freight protection. Understanding what your policy covers-and what it excludes-prevents costly gaps when you need the protection most. The next step involves assessing your specific cargo types and values to determine the right limits for your operation.

Why Your Fleet Needs Cargo Insurance Now

Cargo insurance isn’t optional for professional trucking operations-it’s a financial necessity that separates solvent fleets from those facing bankruptcy after a single major loss. Many carriers mistakenly believe their standard liability policy covers cargo damage, but it doesn’t. Standard liability covers injuries or property damage you cause to third parties, not the goods you’re transporting. When a $50,000 shipment of electronics gets stolen from your trailer or damaged in a collision, your basic liability won’t pay a cent. That gap between what you think you’re covered for and what you actually are covered for is where fleets go under.

The Real Cost of Operating Without Cargo Coverage

The financial reality hits hard: brokers require a minimum of $100,000 in cargo coverage, with higher-value loads demanding $250,000 or more. If you operate without this coverage and lose a load, you’re personally liable for the full value-no insurance company stepping in, no claim to file, just you writing a check to an angry shipper or broker. That single incident wipes out months of profit. A refrigerated load of perishable goods worth $75,000 spoils because your reefer unit fails mid-route, or thieves back up to your trailer at a rest stop and take $120,000 in retail freight. Without cargo coverage, you absorb those losses completely. Many carriers don’t survive their first major claim without insurance protection.

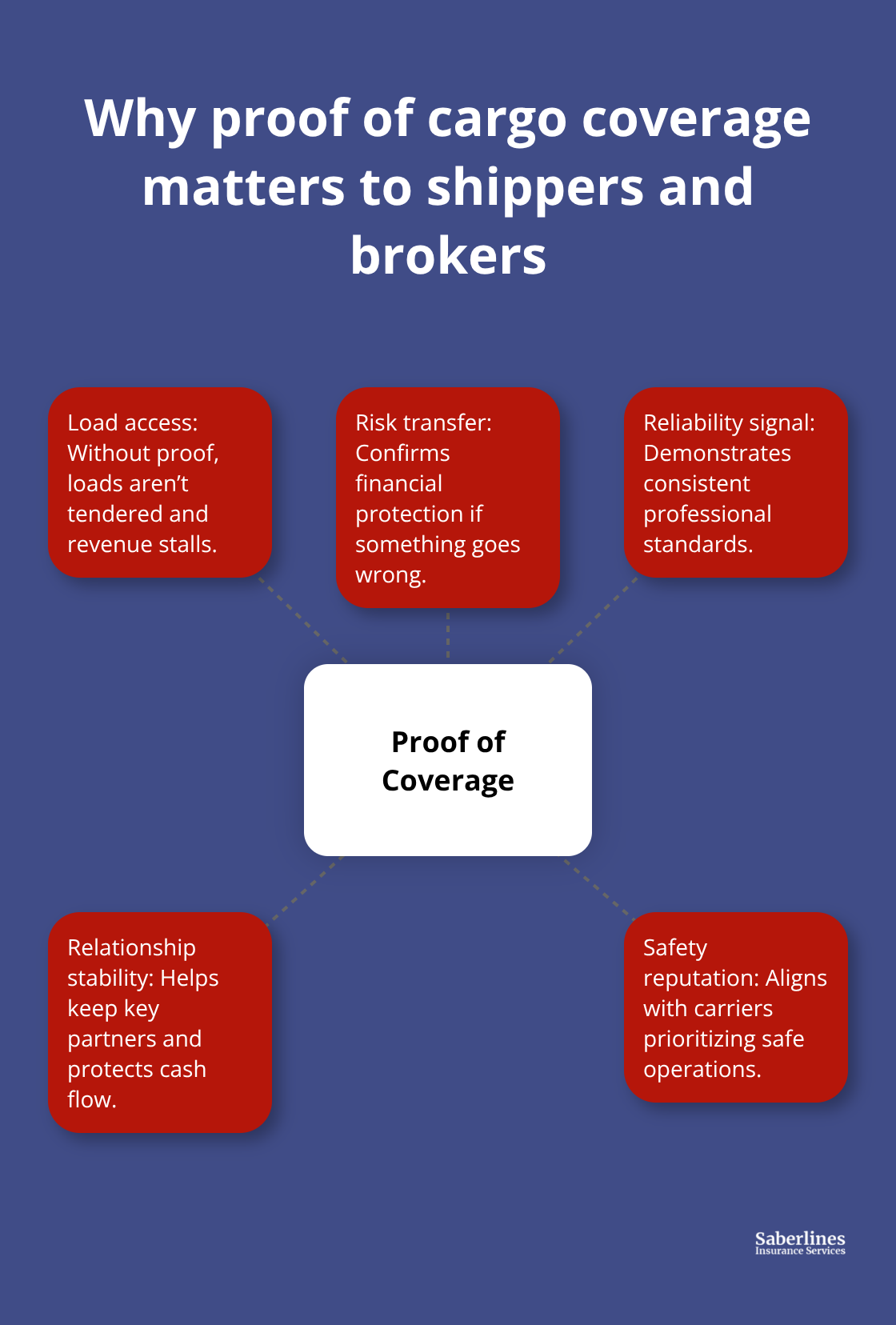

Why Shippers and Brokers Demand Proof of Coverage

Shippers and brokers know the stakes. They won’t load your truck without proof of active cargo coverage because they understand the risk. No coverage means no loads, which means no revenue. Losing a single major shipper or broker relationship devastates cash flow for owner-operators and small fleets. Shippers evaluate carriers on three things: reliability, safety, and professionalism.

Carrying robust cargo coverage signals that you take your responsibilities seriously and won’t disappear when something goes wrong.

Cargo Coverage as a Contract Requirement

Many freight brokers include cargo coverage as a contractual requirement-some won’t even quote you if you can’t provide a Certificate of Insurance showing active coverage. That means cargo insurance isn’t just protection; it’s a business requirement that determines which loads you can legally haul. Without it, entire contract opportunities close. The investment in cargo coverage pays for itself the moment you secure a contract that requires it, because that contract wouldn’t exist otherwise. Carriers with verified cargo coverage maintain stronger relationships with shippers and brokers, leading to more consistent load opportunities and better rates over time.

Moving Forward With the Right Protection

Your next step involves assessing your specific cargo types and values to determine the right limits for your operation. Understanding what your policy covers-and what it excludes-prevents costly gaps when you need the protection most.

How to Choose the Right Cargo Insurance Policy

Start With Your Actual Cargo Values

Picking cargo coverage means starting with a brutally honest inventory of what you haul. Electronics, refrigerated goods, retail freight, and machinery require different protection levels because they carry different risk profiles and values. A carrier hauling $30,000 loads of canned goods faces a completely different exposure than one moving $150,000 in semiconductor components. Your policy limits must reflect the actual value of shipments you handle regularly, not some theoretical number that sounds reasonable.

Brokers typically demand $100,000 minimum, but if your average load sits at $200,000, that minimum leaves a $100,000 gap that destroys you financially if something goes wrong. Talk to your largest shipper or broker partner and ask directly: what cargo values do you typically move? What do your contracts specify? That conversation takes fifteen minutes and prevents months of regret later. Higher-value loads demand $250,000 or more in coverage depending on freight type and contract language.

Verify Refrigeration and Deductible Details

Refrigerated loads add another consideration entirely. Reefer coverage is often included automatically in certain package options, so verify this detail before you quote because it changes your premium significantly. The deductible matters equally. A $1,000 deductible costs less monthly but hits harder when you file a claim; a $5,000 deductible spreads the pain across more months but protects you better when loss happens.

Most fleets find a $2,500 deductible strikes the right balance between manageable monthly cost and reasonable claim exposure.

Reject Price-Only Shopping

The second step involves rejecting the temptation to shop purely on price. Insurance companies price cargo coverage based on cargo type, operating radius, equipment age, and driver history-meaning the cheapest quote often comes from a carrier that doesn’t understand your specific risks or excludes coverage you actually need. A carrier that excludes improper loading might quote $200 monthly cheaper, but that exclusion leaves you exposed on the exact scenario that happens most often in real operations.

Work With Transportation Specialists

Work with specialists who ask detailed questions about your freight mix, your routes, your equipment condition, and your driver experience level. An agent who has handled dozens of cargo claims knows which exclusions matter and which ones you can safely live with. They know that theft coverage becomes critical if you park overnight in unsecured areas, or that water damage coverage matters more for cross-country routes than regional ones.

Ask any potential insurer about their claims process specifically-how fast do they respond, do they have in-house adjusters, and what documentation do they actually require? A carrier promising two-day claims processing saves you money when you’re sitting idle waiting for authorization to move forward. Request references from other carriers they insure and call them directly. That five-minute conversation reveals whether the insurer actually pays claims without fighting or whether they nickel-and-dime every loss.

Evaluate Coverage Exclusions Carefully

The right specialist costs the same or less than a cheap quote but delivers actual protection when you need it. Transportation specialists understand that improper loading exclusions, theft gaps, and water damage limitations create real exposure in your daily operations. They match coverage to your specific freight mix rather than selling a one-size-fits-all policy. Saberlines Insurance Services specializes in transportation risks and understands these details in ways that generic commercial agencies do not. When you work with a firm that focuses on trucking, you get agents who speak your language and know your industry’s actual hazards.

Final Thoughts

Truck cargo insurance protects your bottom line by eliminating the financial devastation that follows a single major loss. Without it, a stolen load, equipment failure, or accident wipes out months of profit and potentially closes your business. With it, you transfer that risk to an insurer and keep operating.

Choosing the right policy requires more than finding the lowest price-it demands working with specialists who understand transportation risks and ask the right questions about your freight mix, routes, and equipment. Generic commercial agencies miss critical details that matter in trucking (improper loading exclusions, refrigeration breakdown coverage, claims processing speed). They don’t understand why a two-day claims process saves you money when you’re sitting idle waiting for authorization.

Contact Saberlines Insurance Services to discuss your cargo coverage needs and get a quote tailored to your operation. Your next major loss is coming, and we help you prepare for it with protection that actually works when you need it most.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.