Truck Insurance for Owner-Operators: Affordable Coverage for Solo Operators

Running your own truck operation means managing costs on every front. Truck insurance for owner-operators is one expense you can’t skip, but finding affordable coverage that actually protects your business takes strategy.

We at Saberlines Insurance Services help solo operators cut through the confusion and find policies that fit their budget and their needs. This guide walks you through what coverage matters, how to compare quotes, and the mistakes that cost owner-operators money.

What Coverage Actually Protects Your Operation

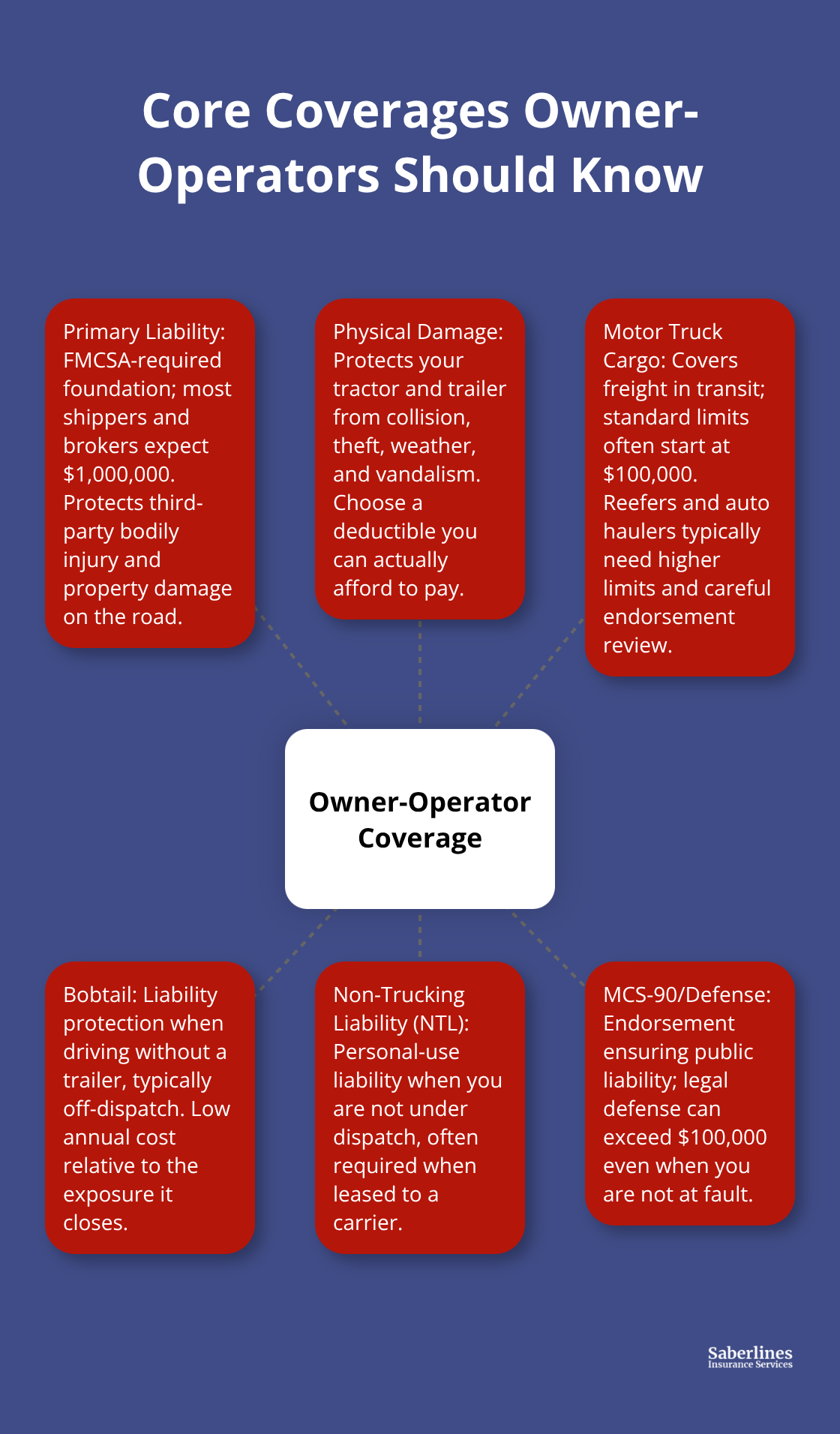

Primary liability forms the foundation of any owner-operator policy and you cannot skip it. The Federal Motor Carrier Safety Administration requires a minimum of $750,000 in liability coverage, but that floor misleads most operators-shippers and brokers won’t dispatch loads unless you carry $1,000,000. In 2024, the FMCSA recorded over 152,000 truck accidents, with average injury costs around $148,279. A single accident without adequate liability coverage wipes out years of profit. Typical annual rates for $1,000,000 in primary liability run $8,000 to $15,000, and new authorities often pay more because underwriters view inexperience as higher risk.

Every primary liability policy includes an MCS-90 endorsement, which guarantees public liability coverage and covers legal defense costs that can exceed $100,000 even if you’re not at fault. That defense protection alone justifies the premium.

Physical Damage Protects Your Biggest Asset

Most owner-operators have $150,000 to $250,000 tied up in equipment, and physical damage coverage protects that investment from collision, theft, weather, and vandalism. While federal law doesn’t mandate it, lenders do-financed equipment requires it. Motor truck cargo insurance proves equally critical. Standard cargo coverage starts at $100,000 and costs roughly $500 to $1,800 annually, but higher-value loads demand more. Auto haulers typically need $250,000 in cargo limits, running $2,500 to $3,500 yearly, while refrigerated freight costs $2,500 to $3,500 for standard coverage. Cargo theft exceeds $30 billion annually according to industry data, and 2024–2025 policies often exclude theft unless you purchase it as a specific endorsement-that gap can cost you entire loads. Physical damage deductibles range from $500 to $5,000; higher deductibles lower premiums but only if you can actually cash-flow a repair bill when it hits.

Bobtail and Non-Trucking Liability Fill Critical Gaps

Bobtail insurance covers liability when you operate without a trailer, typically costing $240 to $720 annually. Non-trucking liability (NTL) covers personal use of the truck when you’re off-dispatch, also running $240 to $720 per year. If you’re leased to a carrier, the carrier’s primary policy covers dispatch work, but the moment you use that truck for personal errands or between loads, you face exposure. One accident during personal use without NTL leaves you personally liable for injuries and property damage. These two coverages cost little relative to the exposure they plug, yet many owner-operators skip them because law doesn’t mandate them. That’s a costly mistake-a single claim without proper coverage can exceed the premium you’d pay over five years. A claim without bobtail or NTL coverage can also trigger coverage denial, which means you pay the full cost of injuries, property damage, and legal defense out of pocket.

Understanding what each coverage type protects helps you build a policy that matches your actual operation, not just regulatory minimums. The next section shows you how to compare quotes from multiple providers and identify which discounts actually save you money without sacrificing protection.

How to Find Affordable Truck Insurance Quotes

Compare Quotes Across Specialized Carriers

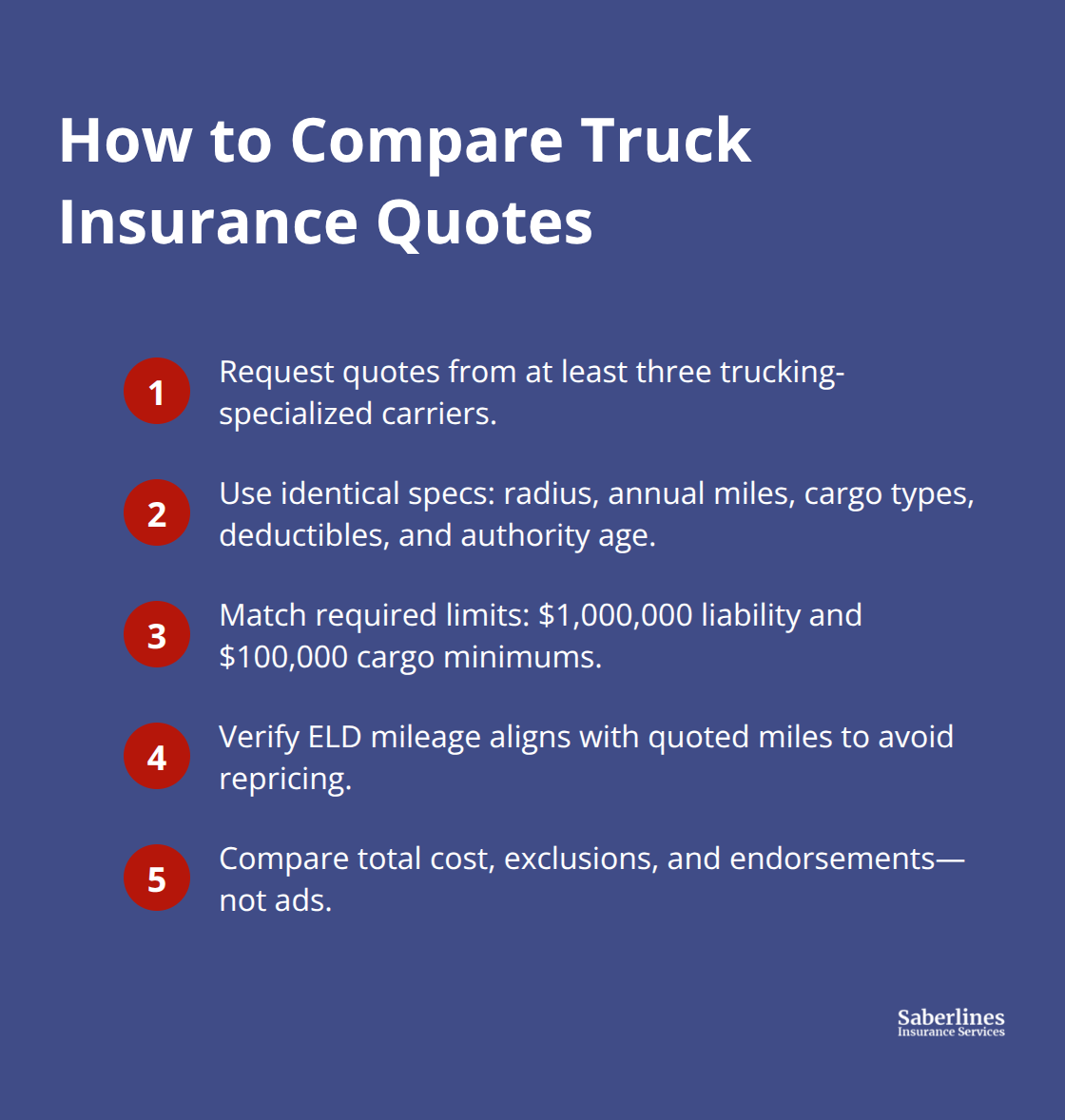

Shopping for truck insurance quotes requires discipline, not just price chasing. Most owner-operators grab the first three quotes and pick the cheapest one, then wonder why claims get denied or certificates of insurance don’t match what they quoted. That approach costs money. Instead, contact at least three trucking-specialized carriers and request quotes based on identical specifications: same radius, same estimated annual miles, same cargo types, same deductibles, same authority age. Mileage discrepancies alone sink quotes-if your ELDs show 110,000 miles but you quote at 60,000, underwriters price you as higher risk and your approved rate jumps significantly at binding. Accuracy in your initial submission matters more than shopping speed.

When you receive quotes, verify that each one reflects the same $1,000,000 liability and $100,000 cargo minimums that shippers and brokers expect. State-minimum pricing looks attractive in advertisements but won’t move freight in the real world. Try apples-to-apples comparisons rather than chasing the lowest advertised price.

Control the Pricing Levers You Can Influence

The biggest pricing levers you control are mileage and radius, cargo type, new-venture status, your motor vehicle record and PSP scores, and deductible amounts. A clean driving record cuts premiums substantially; Federal Motor Carrier Safety Administration data show that drivers with preventable violations face premium increases or carrier rejections regardless of experience length. A single preventable violation, especially an out-of-service issue, can raise premiums or limit carrier options.

Install dual-facing dash cameras to reduce premiums by five to fifteen percent and provide defense against false claims, making them worthwhile even if you absorb the upfront cost. Bundle multiple coverages with one provider to save roughly ten to fifteen percent on total premiums compared to splitting coverage across carriers. Shop renewals sixty to ninety days before expiration to access more markets and ensure you’re comparing actual rates, not just advertised figures. Last-minute quote scrambles force you into narrow options and weaker negotiating position.

Manage Deductibles and Payment Strategy

Deductible strategy directly impacts what you pay monthly and what you can afford to repair. Higher deductibles lower premiums, but only increase them if your emergency fund can absorb a $2,500 to $5,000 repair bill without stalling operations. Premium financing offers fifteen to twenty-five percent down with eight to ten monthly installments, which spreads cost but adds finance charges. Pay in full when possible to reduce overall annual cost by avoiding those finance charges.

Telematics and safe-driving programs unlock substantial discounts as insurers reward technology-driven safety practices. A full-service agency connects you with carriers that value your driving history and compliance documentation rather than just running automated quotes. Avoid last-minute certificate of insurance changes that cause load rejections and payment delays; scrambling for COIs complicates claims and signals disorganization to underwriters.

Your goal is to present yourself as a compliant operator with preventive maintenance logs, documented tire and brake care, solid safety practices, and no distracted-driving violations. That consistency keeps renewal pricing stable and opens access to more competitive markets year over year. The next section addresses the mistakes that undermine this strategy and cost owner-operators thousands in denied claims and coverage gaps.

Common Mistakes Owner-Operators Make With Insurance

Most owner-operators build their insurance around the cheapest quote, then assume coverage gaps won’t matter until a claim lands on their desk. That assumption costs thousands. The real damage happens in three places: carrying limits that look acceptable on paper but fail under actual loss conditions, ignoring exclusions that void claims when you need them most, and treating insurance as a set-it-and-forget-it expense rather than a business tool that needs annual review. In 2026, underwriters tighten risk models and enforcement rises, which means gaps that went unnoticed five years ago now trigger claim denials and premium spikes at renewal.

Cargo Limits and Specialty Loads Create Silent Exposure

Cargo insurance exclusions burn most owner-operators. Standard $100,000 cargo coverage costs $500 to $1,800 annually, but refrigerated freight or auto transport demands higher limits. Refrigerated loads require $2,500 to $3,500 annually for adequate coverage because a breakdown or spoilage claim can exceed $50,000 in minutes. Auto haulers need $250,000 in cargo limits, running $2,500 to $3,500 yearly, yet many operators quote at $100,000 to save premium, then lose entire loads to uncovered claims. Cargo theft exclusions create another silent killer. Industry data show cargo theft exceeds $30 billion annually, and 2024–2025 policies typically exclude theft unless you purchase it as a separate endorsement costing $200 to $500 extra. Load one high-theft commodity without that endorsement and a single theft wipes out months of premium savings. The mistake isn’t carrying cargo insurance-it’s carrying the wrong limit or exclusions for the loads you actually run.

Policy Review Gaps and Authority Changes

Failing to review your policy annually creates cascading problems. Your operation changes (you add a second truck, shift to different cargo types, expand your radius, or adjust your annual mileage estimates), but your insurance stays static. Underwriters base premiums on the information you provided at binding, so mismatches between your actual operation and your policy details trigger claim complications and underwriting reviews at renewal. If your ELDs show 120,000 miles but your policy was quoted at 80,000, you’re technically misrepresented, which gives insurers grounds to adjust claims or raise renewal rates aggressively. More critically, regulatory compliance changes every year. In 2025–2026, the FMCSA focuses heavily on driver qualification files, medical certification accuracy, and domicile status verification. A driver qualification file gap or a missed medical recertification can cause your carrier to deny coverage or cancel outright, even if the gap exists for only 30 days. Owner-operators who don’t review their compliance documentation annually discover problems when a load is rejected or a claim is denied.

Timing and Documentation Mistakes

Authority age matters significantly. New authorities face higher premiums and stricter underwriting, so if you operate under your own authority within your first three years, expect fewer options and tighter documentation requirements. That means gaps in your application or misstatements in your initial filing carry long-term consequences. Many operators wait until 30 days before expiration to shop for renewal quotes, which compresses your negotiating window and forces acceptance of whatever quote comes through first. A full policy review 60 to 90 days before renewal catches mismatches, updates your operation details, and opens access to competitive markets. Last-minute scrambles for certificates of insurance cause load rejections and payment delays, which complicate claims and signal disorganization to underwriters.

Avoid these timing traps by scheduling your annual review well in advance and maintaining accurate, current documentation throughout the year.

Final Thoughts

Truck insurance for owner-operators succeeds when coverage matches your actual operation, not regulatory minimums. A clean driving record, accurate mileage reporting, dual-facing dash cameras, and bundled coverages lower premiums without sacrificing protection. Shopping 60 to 90 days before renewal opens competitive markets and prevents last-minute scrambles that force weak negotiating positions.

The three mistakes outlined above-underestimating cargo limits, ignoring policy exclusions, and skipping annual reviews-cost operators thousands in denied claims and coverage gaps. Higher deductibles work only if your emergency fund can absorb them; otherwise, they create cash-flow problems when repairs hit. Working with a specialized agency matters because trucking insurance differs fundamentally from standard commercial auto, and carriers that understand owner-operator operations price risk more fairly and catch compliance gaps before they trigger claim denials.

Contact Saberlines Insurance Services to discuss your operation, your cargo types, your authority age, and your budget. We’ll build quotes that reflect your actual risk, not just advertised minimums, and show you where you can cut costs without creating exposure. Getting a quote takes minutes, but the conversation that follows determines whether your coverage actually protects your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.